The consolidated government – treasury and central bank

In yesterday’s blog – If only the citizens knew what was going on! – I noted that it makes very little sense from a flow of funds perspective to consider the central bank not to be part of a consolidated government sector along with the treasury. The notion of a consolidated government sector is a basic Modern Monetary Theory starting point and allows us to demonstrate the essential relationship between the government and non-government sectors whereby net financial assets enter and exit the economy without complicating the analysis unduly. This simplicity leads to many insights all of which remain valid as operational options when we add more detail to the model. However, it still seems that readers are confused by this and somehow think that the consolidation is misleading. So for today’s blog I aim to explain in more detail what this consolidation is about. It should disabuse you of the notion that the mainstream macroeconomics obsession with central bank independence is nothing more than an ideological attack on the capacity of government to produce full employment which also undermines our democratic rights.

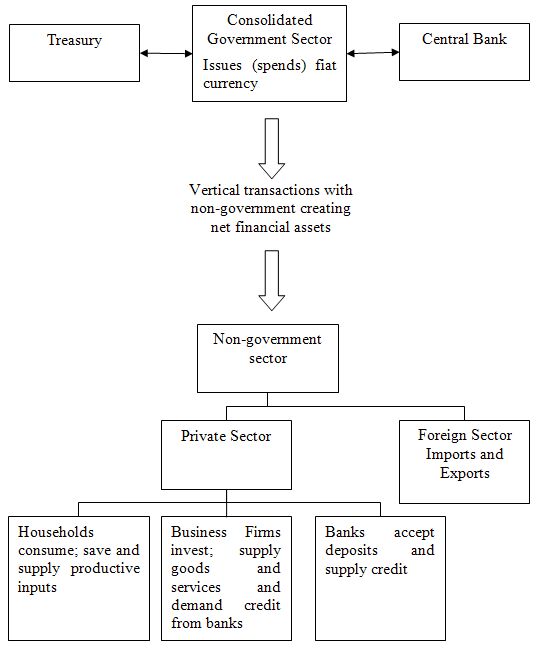

Regular readers will have seen this diagram which appeared along with discussion in the blog – Deficits 101 Part 3 – but was originally presented in my book Full Employment Abandoned: Shifting sands and policy failures which was published in 2008.

You should also read the blog – Deficits 101 Part 1 – to refresh your memory of the vertical relationship between the government and non-government sectors whereby net financial assets enter and exit the economy.

The diagram sought to elaborate on the vertical transactions between the government and non-government sectors and to explain the importance of them for understanding how the economy works? It was intended as a vehicle to help people connect the pieces of the monetary system in an orderly fashion and to re-educate those who have been poisoned by mainstream macroeconomics textbooks.

You will see that this diagram adds more detail to the diagram presented in Deficits 101 Part 1 – which showed the essential relationship between the government and non-government sectors arranged in a vertical fashion.

Focusing on the vertical train first, you will see that the tax liability lies at the bottom of the vertical, exogenous, component of the currency. The consolidated government sector (the treasury and central bank) is at the top of the vertical chain because it is the sole issuer of currency and the transactions that the treasury and the central bank make with the non-government are able to alter the net system balance (which I will explain presently).

The middle section of the graph is occupied by the private (non-government) sector. It exchanges goods and services for the currency units of the state, pays taxes, and accumulates the residual (which is in an accounting sense the federal deficit spending) in the form of cash in circulation, reserves (bank balances held by the commercial banks at the central bank) or government (Treasury) bonds or securities (deposits; offered by the central bank).

The currency units used for the payment of taxes are consumed (destroyed) in the process of payment. Given the national government can issue paper currency units or accounting information at the central bank at will, tax payments do not provide the state with any additional capacity (reflux) to spend.

The reason we take a consolidated approach to government in the first instance is because the two arms of government (treasury and central bank) have an impact on the stock of accumulated financial assets in the non-government sector and the composition of the assets.

The government deficit (treasury operation) determines the cumulative stock of financial assets in the private sector. Central bank decisions then determine the composition of this stock in terms of notes and coins (cash), bank reserves (clearing balances) and government bonds with one exception (foreign exchange transactions).

The diagram also shows how the cumulative stock is held in what we term the non-government Tin Shed which stores fiat currency stocks, bank reserves and government bonds.

I invented this Tin Shed analogy to disabuse the Australian public of the notion that somewhere down in Canberra (our national capital) there was a storage area where the national government was putting all those surpluses away for later use. This is a constant misperception that pervades the policy debate. Even the mainstream macroeconomics textbooks call budget surpluses “national saving”.

The reality is that there is no storage because when a surplus is run, the purchasing power embodied in the net outflow of financial assets from the non-government sector to the government sector is destroyed forever. However, the non-government sector certainly does have a Tin Shed within the banking system and elsewhere.

Any payment flows from the government sector to the non-government sector that do not finance the taxation liabilities remain in the non-government sector as cash, reserves or bonds. So we can understand any storage of financial assets in the Tin Shed as being the reflection of the cumulative budget deficits.

Taxes are at the bottom of the exogenous vertical chain and go to rubbish, which emphasises that they do not finance anything. While taxes reduce balances in private sector bank accounts, the government doesn’t actually get anything – the reductions are accounted for but go nowhere.

Thus the concept of a fiat-issuing Government saving in its own currency has no meaning. Governments may use its net spending to purchase stored assets (spending the surpluses for instance on gold or in sovereign funds) but that is not the same as saying when governments run surpluses (taxes in excess of spending) the funds are stored and can be spent in the future. This concept is erroneous. Please read my blog – The Futures Fund scandal – for more discussion on this point.

Finally, payments for bond sales are also accounted for as a drain on liquidity but then also scrapped.

What are the implications of all this?

You will have heard of the term the monetary base which appears in most macroecoomics text-books as the precursor to outlining the erroneous concept of the money multiplier. Please read my blogs – Money multiplier and other myths and Money multiplier – missing feared dead – for more discussion about why there is no money multiplier.

The concept of the monetary base is a very narrow concept of what economists misleadingly call money. We will use the term net financial assets because it is less problematic.

The monetary base is comprised of:

- The currency (notes and coins) held by the public and issued by the government);

- The deposits that the commercial banks have with the central bank – the so-called reserves;

- The liabilities the central bank has to the non-bank financial intermediaries.

The term “base” is loaded (excuse pun) because it is seen by the mainstream as the base on which banks lend from. Of-course bank lending is not reserve constrained so the term lacks meaning in this context. Please read the following blogs – Building bank reserves will not expand credit and Building bank reserves is not inflationary – for further discussion on this point.

The following table captures the relationship between the monetary aggregates but in no way supports a money multiplier interpretation of the linkages.![]()

The Table helps to sort the vertical transactions (1 to 4) from the horizontal (6 and 8).

National government budget impacts

In isolation, a national government budget deficit, which results from the government spending more (via crediting bank accounts and/or posting cheques) than it drains via taxation revenue from the non-government sector, results in an overall injection of net financial assets to the monetary system. This boosts the monetary base.

Conversely a national government budget surplus, which results from the government spending less than it drains via taxation revenue from the non-government sector, results in an overall withdrawal of net financial assets from the monetary system. This reduces the monetary base.

However, if the government also issues debt $-for-$ to match its deficit then the impact on the monetary base is neutralised. Mainstream textbooks think this is a “funding” operation, whereas from a MMT perspective it is a bank reserve operation which allows the central bank to effective conduct its liquidity management tasks.

Please read my blog – Understanding central bank operations – for more discussion on this point.

Foreign exchange transactions

The external position of a nation impacts on the monetary base if there is official central bank foreign exchange transactions.

A nation’s currency is demanded in foreign exchange markets to facilitate the purchase of its exports by foreigners; to pay interest, profits and dividends to residents who have foreign investments; and to faciliate foreign direct investment in local companies.

Conversely, a nation’s currency is supplied to foreign exchange markets to facilitate the purchase of imports from other countries; to pay interest, profits and dividends to foreign investors; and to faciliate lending to foreign companies.

Ordinarily, where there is a balance of payments deficit the demand for a nation’s currency in foreign exchange markets will be less than the supply of that currency and there will be downward pressure on the exchange parities.

When there is a balance of payments surplus the demand for a nation’s currency in foreign exchange markets will be greater than the supply of that currency and there will be updward pressure on the exchange parities.

So exchange rate movements can arise from the real sector and the financial sectors with the latter increasingly dominating in the era of financialisation. That situation is one thing that needs to be changed if we are to restore stable growth with full employment but that is the topic of another blog.

A floating exchange rate system allows these supply and demand imbalances in currencies to resolve themselves via exchange rate movements with no impact on the monetary base.

However, under a fixed exchange rate system, a country with an external deficit (supply of currency greater than demand) would face downward pressure on its parity and the central bank was committed to easing that quantity imbalance by conducting official foreign exchange transactions. So in this case it would buy its own currency in the foreign exchange markets by selling foreign currencies until the demand and supply of the local currency was equal and consistent with the fixed exchange rate being targetted.

These transactions would drain the local currency from the economy (the foreign exchange market is considered part of the monetary system) and so the monetary base would shrink.

If the nation had an external surplus (supply of currency less than demand) it would face upward pressure on its parity and the central bank had to sell its own currency in the foreign exchange markets by buying foreign currencies until the demand and supply of the local currency was equal and consistent with the fixed exchange rate being targetted.

These transactions would inject the local currency from the economy (the foreign exchange market is considered part of the monetary system) and so the monetary base would increase.

In a pure floating regime with no official central bank intervention, there is no change in the volume of a nation’s currency as a result of the foreign exchange transactions. As an example, assume an exporting firm in Australia earns $USDs and seeks to convert them into $AUDs. It will sell them to a foreign exchange dealer who brokers a deal with a counterparty who desires to hold $USDs and already has $AUDs (perhaps an importing firm).

The exporting firm’s holdings of $AUDs rises as the counterparty’s holds fall. There is no change in the volume of AUDs on issue.

Clearly, things are different in a pure fixed exchange rate system as noted above. A floating exchange rate system thus does no hamper monetary or fiscal policy in the same way that monetary policy is forced to defend the parity in a fixed exchange rate system.

In reality, the central bank still conducts official foreign exchange transactions even if the currency mostly floats. So when the currency is weak (and the central bank fears an inflationary spike coming via increased import prices), it may intervene and buy foreign currency and vice versa when the currency is strong (and there is a fear that the competitiveness of the trading sector is compromised).

The following graphs show the scale of that intervention in Australia since 1973. The data is available from the Reserve Bank of Australia. The left-panel shows the total official FX transactions in $A millions (which include gold and foreign exchange less net overseas borrowing of the national government), the middle panel shows the change in reserve assets due to valuation in $A millions, while the right-panel shows the total change in reserve assets.

You can see the scale of the transactions has increased over time and there are huge swings in short periods of time.

I plan to write some more about the capacity of foreign exchange markets to wreak havoc on a nation, a point that some commentators seem to have become stuck on recently. I would note that Australia is an extremely open economy with litle industrial base. Our export sector is largely based on primary commodities and agriculture.

We have huge swings in our exchange rate. For example in September 2001, the $AUD was selling for 0.4923 $USD and all my US mates were laughing about how we were now the half-price country. By March 2007, it was back over 80 cents. In 1987, we lost about 10 per cent of our nominal GDP in valuation effects due to currency depreciation and terms of trade swings in two quarters! These are huge swings. Our standard of living was barely impacted.

![]()

Government bond sales

The impact of national budget outcomes and central bank official intervention on the monetary base can be offset by government bond sales/purchases. Why would the government desire this offset?

The fundamental principles that arise in a fiat monetary system are as follows.

- The central bank sets the short-term interest rate based on its policy aspirations.

- Government spending is independent of borrowing which the latter best thought of as coming after spending.

- Government spending provides the net financial assets (bank reserves) which ultimately represent the funds used by the non-government agents to purchase the debt.

- Budget deficits (and official foreign intervention which adds to the monetary base) put downward pressure on interest rates contrary to the myths that appear in macroeconomic textbooks about ‘crowding out’.

- The “penalty for not borrowing” is that the interest rate will fall to the bottom of the “corridor” prevailing in the country which may be zero if the central bank does not offer a return on reserves.

- Government debt-issuance is thus a “monetary policy” operation rather than being intrinsic to fiscal policy, although in a modern monetary paradigm the distinctions between monetary and fiscal policy as traditionally defined are moot.

To understand these points we need to understand the concept of a system balance which relates to the daily liquidity in the banking system. The system balance is another term for the monetary base. It is important to understand it because it impacts on the ability of the central bank to maintain its desired monetary policy stance – which involves setting a particular overnight interest rate.

Every day, official transactions are occurring (Items 1 to 3 in the Table above) and they impact on the system balance or the money market cash position.

Governmments spend and tax continuously and the central bank regularly conducts official foreign exchange transactions. Further public debt matures regularly and the central bank may conduct repos and rediscount treasury notes before their maturity date is reached.

When the flow of funds that accompany the vertical transactions is in favour of the government sector, we say the system balance is in deficit (or the system is “undersquare”) and vice versa (surplus or oversquare).

You can thus appreciate the particular transactions and balances that will deliver a system surplus or a system deficit.

A budget deficit, for example, will result in a system surplus or oversquare position. There will be excess reserves in the accounts held by the banks with the central bank.

If there is no support rate paid by the central bank on these excess reserves then the commercial banks will try to lend then on the interbank market. The possible borrowers will be other banks who lack reserves at the end of the day. But these horizontal transactions are incapable of clearing the overall system overall. All they do is shuffle which banks are carrying the excess.

In trying to chase a return on the excess reserves, the competition in the interbank market drives the overnight rate down to whatever support rate is in place (which might be zero). Effectively, if there was no central bank reaction, the official policy rate being maintained by the central bank would become irrelevant as the interbank rate fell.

The central bank can drain the excess reserves simply by selling government debt. Accordingly, debt is issued as an interest-maintenance strategy by the central bank. It has no correspondence with any need to fund government spending.

The analysis should be easily understood in the case of the impacts of budget surpluses and the impact of official foreign exchange transactions that add reserves and those that drain reserves.

Further, the idea that governments would simply get the central bank to “monetise” treasury debt (which is seen orthodox economists as the alternative “financing” method for government spending) is highly misleading. Debt monetisation is usually referred to as a process whereby the central bank buys government bonds directly from the treasury.

In other words, the federal government borrows money from the central bank rather than the public. Debt monetisation is the process usually implied when a government is said to be printing money. Debt monetisation, all else equal, is said to increase the money supply and can lead to severe inflation.

However, as long as the central bank has a mandate to maintain a target short-term interest rate and does not pay a support rate on excess reserves, the size of its purchases and sales of government debt are not discretionary. Once the central bank sets a short-term interest rate target, its portfolio of government securities changes only because of the transactions that are required to support the target interest rate.

The central bank’s lack of control over the quantity of reserves underscores the impossibility of debt monetisation. The central bank is unable to monetise the federal debt by purchasing government securities at will because to do so would cause the short-term target rate to fall to zero or to the support rate. If the central bank purchased securities directly from the treasury and the treasury then spent the money, its expenditures would be excess reserves in the banking system. The central bank would be forced to sell an equal amount of securities to support the target interest rate.

The central bank would act only as an intermediary. The central bank would be buying securities from the treasury and selling them to the public. No monetisation would occur.

However, the central bank may agree to pay the short-term interest rate to banks who hold excess overnight reserves. This would eliminate the need by the commercial banks to access the interbank market to get rid of any excess reserves and would allow the central bank to maintain its target interest rate without issuing debt.

From a MMT perspective it is far preferable to eliminate the debt-issuance machinery altogether and pay a support rate on reserves if the central bank wants to target a non-zero short-term interest rate. But even more preferable is to allow the short-term interest rate to drop to zero by not issuing public debt or paying a support rate on excess reserves. Then the interbank market will compete the rate down to zero each day and fiscal policy would become the principle counter-stabilisation tool and the most effective means of disciplining price pressures in specific asset classes.

Please read the following blogs – Operational design arising from modern monetary theory – Asset bubbles and the conduct of banks and The natural rate of interest is zero! for further discussion of the preferred MMT position.

Conclusion

The vertical transactions which add to or drain the monetary base that I have outlined here are transactions between the government and the non-government sector. I note some people think the distinction between government and non-government is confusing but you should see it as an essential starting point to understanding the nature of the vertical transactions.

These transactions are thus unique – they change net financial assets in the economy.

All the transactions between private sector entities have no effect on the net financial assets in the economy at any point in time.

Anyway, we have now explicitly considered the impact of official foreign exchange transactions (which might include gold sales and purchases as well as straightforward currency deals).

Australian Federal Election

Tomorrow is our national election.

We are forced to vote here. Some democracy. The choices between the major parties are either bad or very bad. The Greens who are the third main party have no understanding of macroeconomics. Some democracy.

The Government may change tomorrow given the polls and Julia Gillard our first female prime minister will then have the record of the shortest prime minister in history. The Government should have kept the stimulus going and taken some hard decisions on climate change and stopped locking refugees up in prisons (including their children). They did not take any major progressive decisions in their term of office and were beguiled by their neo-liberal pretensions.

They deserve to be tossed out. But that is not to say that the conservatives deserve to be voted in. They are a disgrace and will seek to implement pernicious policies on the disadvantaged just like they did when they were in power last time (1996-2007). They deny climate change and want to make it even harder for refugees. They never deserve to be in government of a progressive forward-thinking nation.

The only policy that is separating them is on the construction of the national broadband network. The Government is promising to continue building a technology that will serve us well into the future whereas the conservatives want to keep us back in the past. All discussions about “costs” in that regard are irrelevant because the only costs that matter are the real resources being used and the Government’s plan is probably not much more “costly” than the status quo.

Most importantly, both major parties want to run surpluses without knowing what that means. They do not understand that at this stage of the business cycle even larger deficits are required. They will both run a macroeconomic strategy that will be detrimental to the unemployed and their families and then they will both turn on these same people and introduce punishing welfare-to-work changes that will just make the lives of the miserable even worse.

There is not much choice down here! I am not allowed under existing electoral law to encourage voters that instead of voting they should write essays on their ballot papers outlining why all major parties have lost the plot.

Saturday Quiz

The Saturday Quiz will be back sometime tomorrow. It national election day in Australia so I might have some questions relevant to that event! Our democracy is in a sad state.

That is enough for today!

{kind=link}

0 Comments:

コメントを投稿

<< Home