Correspondence between Keynes and Kalecki

参考:

ミハウ・カレツキ (Michal Kalecki):マクロ経済学の知られざる英雄

http://nam-students.blogspot.jp/2015/10/michal-kalecki.html

http://nam-students.blogspot.jp/2015/10/michal-kalecki.html

ケインズ=カレツキ往復書簡1937

以下の1937年4月4日以降は短縮版。完全版はケインズ全集12(未邦訳)。

1939,1944年は未確認。

宇野とカレツキ 栗田論考

カレツキ展望 鍋島直樹論考

__________

(a)伝統的理論(ケインズ):

投 資 の

|。 。 限 界

| 。 効

|__________。____ 利子率+リスク率

| | 。率

|b |

| | 。

|__________|____

|p |

|__________|_____

k0 k

(b)カレツキ:

| 。利子率+リスク率

| 投資の限界効率 。

|__________。____

| 。 |

| 。 。 |

| b |

|__________|____

| p |

|__________|_____

k0 k

危険逓増の原理 カレツキ The Principle of Increasing Risk ,Kalecki ,1937

《まず投資規模kは,投資の限界効率MEIが利子率ρと投資に伴なうリスク率σの総和に等しくなる水準に決定されるとカレツキは想定する。そうすると図(a)から容易に理解されるように,伝統的理論においてはkの増大とともにMEIが低下する場合にのみ,一定の最適投資量k0が決定されることになる。一般にこのような下落は(1)大規模化の不経済,(2)不完全競争,によって発生するとされている.しかしカレツキは(1)の理由は非現実的であるとし,(2)についても,より現実的ではあるが,これによっては同時に異なる規模の企業が存在することが説明されないと言う.したがって企業規模の相違を説明する他の要因が存在するはずである.》Kalecki1937

96

PART ONE

…

3. Correspondence between Keynes and Kalecki

The Keynes Papers and the Kalecki Papers between them contain

fifteen letters that were exchanged between the two men over the

period 1937-44. Almost all of them (and in particular those reproduced

below) were first published (in Polish translation) in Jerzy Osiatyński's

editorial notes to volume I of Kalecki's Dzieła [Works]. One of these

letters-a most interesting one from December 1944 in which Keynes

expresses his favorable reaction to Kalecki's contribution to the Ox-

ford institute volume Economics of Full Employment (1944)-has now

been reproduced in JMK XXVII, pp. 381-83. I hope that the rest of the

Keynes-Kalecki correspondence will be published in its entirety in future

volumes of Keynes' Collected Writings [see p. xiv above]

Relying on this hope, I have largely restricted myself in this Appendix to reproducing those letters-or excerpts thereof-which refer to

writings of Kalecki discussed in chap. 3 above. The letters are in their

original English form, and I am greatly indebted to Jerzy Osiatyński,

Austin Robinson, and Mrs. Ada Kalecki for providing me with photo-

copies of them and permitting their reproduction here

The Kalecki letters are reproduced from the originals which he sent

to Keynes. Most of these contain handwritten notes which Keynes

jotted down in their margins after receipt and which in most cases he

subsequently elaborated upon and incorporated in his replies; these

marginal notes have not been reproduced here. All of Kalecki's

letters-except for the first-are typewritten. Keynes' letters have

been reproduced from the typewritten carbon copies he retained

Words or phrases italicized in the following were so emphasized in the

original correspondence. As before, my explanatory comments appear

in square brackets and in notes.

12. The original is handwritten. This seems to have been the first letter that passed

Dear Mr. Keynes,

between Kalecki and Keynes.

Appendix

97

London, February 4th, 1937(12)

I beg ta send you enclosed my paper The commodity tax, income tax and capital tax in the light of the Keynesian theory(13 and

to ask whether it might be published in the "Economic Journal."

Yours sincerely,

[signed] M. Kalecki

P.S. I tried to do my best as concerns the English but the curve of

my "marginal productivity" in this "production" is steeply falling.

[Cambridge.] February 16th, 1937

Dear Kalecki

I am happy to accept the enclosed, which I find very interesting,

for the Economic Journal. The English is not bad, and the correc-

tions required mainly affect the order of the words. The argument

would be easier for an English reader to follow if the sentences were

somewhat rearranged into our more habitual order. Could you, do

you think, pass the article on to some English friend to get him to

dictate from it in a more flowing order.

There is only one small suggestion I have to make in the text. I

think it would be advisable, in the first part, to make quite explicit

your assumption that the consumption of the capitalists is entirely

directed to goods other than wage-goods. It is clear to a careful

reader that you are assuming this, but since the assumption is a very

unrealistic one, it is desirable to make it clearly.

I have been conscious for some time of the relevance of the theory

you refer to to the choice between income tax and a capital tax, but I

had not myself worked out the conclusions as rigorously as you have

done

I return the article herewith for revision. You are too late for the

March Journal and in plenty of time for the June one.

Yours sincerely

[copy initialed] JMK

London, March 20th. 1937

Dear Mr. Keynes,

I beg to send you the revised version of my paper. The style was

corrected by one of my friends according to your kind advice. I also

acted on your suggestion to state explicitly that the capitalists consume

only goods other than wage-goods in putting the footnote on

page 4. I consider there besides the probable effect of this assumption's not being fulfilled

I enclose the reprint of my paper "A Theory of the Business

Cycle(14 and I should like very much if possible to hear your opinion on it.

Yours sincerely,

[signed] M. Kalecki

13. Subsequently published under the title "A Theory of Commodity, Income, and

Capital Taxation 1937).

14. The reference is to Kalecki's 1937 Review of Economic Studies paper.

98

PART ONE

P.S. I use the opportunity to thank you for the reprint of your article

The General Theory of Employment.(15

[Cambridge,] March 30, 1937

Dear Kalecki,

Thank you for the revised version of your article, which I now find

quite clearly written. .. . [Keynes then provides some detailed cr

cisms of Kalecki's article which concludes with the following para

graph:]

Now my impression is that your assumption about the consump-

tion of capitalists, whilst technically convenient for the particular

method of exposition you have adopted, is not really required to

establish your main conclusions about the effect of various taxes on

output. It is required, on the other hand, to establish your con-

clusions as to the effect of the taxes on the distribution of real

income between capitalists and workers. The latter, however, is a

matter in which you are only secondarily interested. Will you think

this over? My impression is that your conclusions as to the effect of

taxes on output could be established without such special assump-

tions. I am inclined to think that the very pretty technique which you

use in the section on short-period equilibrium in your article in the

[1937] Review of Economic Studies(16 would serve your purpose.

You ask me whaI think of the above-mentioned article. The first

two sections I like very much. But I am not convinced by the section

on The Inducement to Invest," particularly pages 84 and 85.

In the second complete paragraph on page 84 you seem to be

assuming not merely that the current rise of prices will have a dis-

proportionate effect on expectations as to future prices, but that

future prices will be expected to rise in exactly the same proportion.

Surely this is an extravagant over-emphasis of the effect of the im

mediate situation on long-term expectations? It appears to me that it

is only if future prices are expected to rise in the same proportion as

present prices that you have established the result that "equilibrium

is not reached and the investment continues to rise."

In the same way on page 85 you point out that the current increase

of wealth does something to diminish the marginal risk. But to

establish your conclusion you appear to be making some quantia

tive assumption that the effect will be just of the right degree,(17

which appears to be unjustified. I might mention, in passing, that the

risk relating to prospective profit is already allowed for in my for-

mula for the marginal efficiency of capital.

In general, therefore, I do not feel that you have sufficiently

established the conclusion italicized at the bottom of page 85.'*

Yours sincerely,

[copy initialed] JMK

「THE REVIEW OF ECONOMIC STUDIES

a gap between the marginal efficiency of the various assets and the rate of

interest, the investment per unit of time will rise until the increase of the prices

of investment goods caused by this will reduce the marginal efficiency of all

assets to the level of the rate of interest

There are two things lacking in this conception. First it tells us nothing

about the rate of investment decisions taken by entrepreneurs faced with givern

market prices of investment goods. It indicates only that unless the marginal

efficiencv of all assets calculated on the basis of this level of prices of investment

goods is equal to the rate of interest, a change of investment will take place

which will transform the given situation into a new one, in which the marginal

efficiency of various assets is equal to the rate of interest

But a new trouble now arises. Let us assume that the rate of investment

has really, say, risen so much that the new level of investment prices and

he initial state of expectations give a marginal efficiency equal to the rate o

interest. The increase of investment, however, will cause not only the prices

of investment goods to rise, but also a rise of prices (or, more precisely, the

upward shift of marginal revenue curves) and employment in all branches of

trade. Thus, because " the facts of the existing situation enter, in a sense

dispsoportionately, into the formation of our long-term expectations," 1 the

state of expectations will improve and the marginal efficiency of assets appear:s

again higher than the rate of interest. Consequently " equilibrium" is not

reached and the investment continues to rise

We see now that the Keynesian conception, which tells only how great

investment will be if the given " disequilibrium " changes into an "equilibrium

encounters a difficulty in this respect also, for it appears that the rise of

investment does not lead to " equilibrium" at all (in any case, not to

immediate “ equilibrium ,,). I shall further try to give an outline of a different

conception of inducement to invest which endeavours to find factors determining

he amount of investment decisions corresponding to every definite state of

long-term expectations, prices of investment goods, and rate of interest.

2. We start from the problem of uncertainty, which is also involved in

Keynes' arguments. It can be gathered from his exposition that a certain

amount has to be subtracted from the marginal efficiency of assets (calculated

on the basis of the current prospective returns) to cover risk before comparing

it with the rate of interest. We can express the same point in this manner:

the gap between the marginal efficiency of assets calculated on the basis of the

prospective current returns of these assets, which we shall call the prospective

rate of profit, and the rate of interest, is equal to the risk incurred. But here

we wish to draw attention to a point not considered by Keynes

The rate of risk of every investment is greater the larger is this investment

If the entrepreneur builds up a factory he incurs a certain risk of unprofitable

business, and these losses, if any, will be more significant for him the greater

. But besides this

in "sacrificing" his reserves (consisting of deposits or securities) or taking

credits, he exhausts his " sources of capital," and if he should need this

proportion the investment considered bears to his wealth

1 General Theory, p. 148」

「A THEORY OF THEBUSINESS CYCLE

85

capital " in the future he may be obliged to borrow at a high rate of interest

because he has overdrawn the amount of credit considered by his creditors as

normal." Thus both these aspects of risk incurred by investment show that

e rate of risk must grow with the amount invested

Now, I think we have the key to the problem of amount of investment

decisions in a given economic situation in a certain period of time, for instance

in our T-period. This amount is just so much as will equate the marginal risk

to the gap between the prospective rate of profit and the rate of interest, both

being given by the economic situation of the period in question. The greatei

the "gap" the greater is the sum of investment decisions in the period, and

his for two reasons. First the number of people undertaking investment

increases, including the more timid entrepreneurs; and, secondly, each of

them invests more

3. In all this conception, however, an obscure point still remains. The

entrepreneurs in the T-period considered have taken so many investment

decisions that any additional investment decision does not seem to thenm

sufficiently attractive because of the growing risk. Will there, then, be no

investment decision at all in the next T-period if the gap between the prospec

tive rate of profit and rate of interest remains at the same level as before?

Certainly this is not the case. For the value of the investment in the second

period-as we know from the preceding chapter-corresponds to the invest

ment decisions in the first r-period; further, the saving in the second period

is equal to the investment in the second period; thus the capitalists as a body

save in the second τ-period just the amount which they decided to invest in

the first T-period. To the money-flow of investments there corresponds an

equal money-flow of savings, and if investment decisions of an equal amount

should not be taken, an improvement in the security of wealth and liquidity

for the entrepreneurs would result (who accumulate reserves or repay debts)

at the end of the period; hence, the marginal risk would be less than the gap

between prospective rate of profit and the rate of interest In this way if

the gap remains as supposed on the same level, a steady reinvestment of the

same amount will take place. The flow of investment decisions continuously

imposes the burden of risk on some capitalists, but the equal flow of savings

relieves other capitalists from this burden.

If the gap between the prospective rate of profit and the rate of interest

increases, the investment decisions in a T-period will be pushed to the point at

which the marginal risk is equal to the increased gap. If this gap does not

change further, reinvestment of the new higher amount will take place in the

following periods.

Thus we can now say that the rate of investment decisions is an increasing

function of the gaþ between the prospective rate of profit and the rate of interest

1 This can also be deduced as follows. It can be concluded from the above that the burden

of risk is created only by the existence of unrealised investment decisions. Thus this burden

is, caeteris paribus, higher the larger the "stock" of uncompleted orders at the end of a given

T-period, which (see p. 82) is equal to Dt. Or the marginal risk increases with the rate of invest

ment decisions D and, consequently, so must the gap between the prospective rate of profit and

the rate of interest needed to cover the risk.」

15. The reference is to Keynes' contribution to the symposium on his book which

appeared in the February 1937 Quarterly Journal of Economics.

16. The reference is presumably to Kalecki's diagrammatic analysis on p. 78 of the article.

17. This is Keynes' handwritten correction of the word "kind" which was originally

typed here. (I am indebted to Donald Moggridge and Judith Allen for this reading of

Keynes' correction.)

「78

THE REVIEW OF ECONOMIC STUDIES

equipment is essential. The objection is often raised that it is wrong to assume

a given capital equipment within a period, because the investment changes

the equipment during this perod. The answer is very simple: this period can

be made so short that the change in the equipment is small enough not to

affect the formation of output and income. For output and income are

quantities measured per unit of time and thus are not dependent on the length

of the period taken into consideration, whilst the change of equipment is

caeteris paribus, proportionate to this length.

SHORT-PERIOD EQUILIBRIUM

1. Output with a given capital equipment depends on the quantity of

labour employed and on its distribution among the various sections of this

equipment. In every enterprise the employment is pushed to the point at

which marginal revenue is equal to the marginal prime cost

We shall represent the point of intersection of the marginal revenue and

the marginal prime cost curves as follows. We subtract from both price and

prime costs the cost of raw materials, and thus we obtain so-called value added

and labour costs respectively. We can now say that the output of an enterprise

is given by the intersection of the curves of marginal value added and of mar

ginal labour-cost (see Fig. 1). Marginal value added and marginal labour-cost

are both expressed here in wage units.1 We shall call short-time equilibrium

a state in which the marginal labour-cost curves and marginal value-added

curves do not move. With a given capital equipment the curves of marginal

labour-cost are fixed. The establishment of short-time equilibrium with a given

equipment will thus consist in the shift of marginal value-added curves.

The area OABC is the value added of the enter

prise expressed in wage-units, the hatched area is

the income of the capitalists obtained from this

enterprise, while the unhatched area is the income

of the workers. Thus the sum of OABC-areas of

all enterprises- is the national income expressed in

wage-units, while the sum of the hatched areas is

the total income of the capitalists, and that of the

unhatched areas the total income of the workers

he national income is also equal to the value of

total consumption and total investment and, as we

have assumed that the workers do not save, the sum

of the unhatched areas covers the value of the consumption of the workers, while the sum of the

1 Keynes defines the wage-unit as follows

in so far as different grades and kinds of

labour and salaried assistance enjoy a more or less fixed relative remuneration, the quantity

of employment can be sufficiently defined for our purpose by taking an hour's employment of

ordinary labour as our unit and weighting an hour's employment of special labour in proportion

to its remuneration; i.e. an hour of special labour remunerated at double ordinary rates will

count as two units. We shall call the unit in which the quantity of employment is measured the

labour-unit; and the money-wage of a labour-unit we shall call the wage-unit." The General

Theory of Employment, Interest and Money, p. 41.」

April 4. 1937

Dear Mr. Keynes

Thank you very much for yours of March 30.... [After discussing

the criticisms Keynes had made in this letter of the article he had

submitted to the Economic Journal, Kalecki turns to Keynes' cri

cisms of his Review of Economic Studies article:]

May I yet make some remarks on your criticism of my paper in the

"Review"? I think that my statement in the second complete para

graph on page 84 you refer to is independent of how much expecta-

tions improve under the influence of the present rise of prices. I state

in this paragraph only that the increase of prices of investment goods

which equates the marginal efficiency based on the initial state of

expectations to the rate of interest, does not create an "equilib-

rium"; for at the same time expectations improve to some extent

and thus investment increases further. I do not deny that this in

crease may be convergent and then the point A in the Fig. 3 corre

sponding to this "equilibrium" may be reached without increase of

the rate of interest (see the bottom of the page 88); whilst if the

reaction of the entrepreneurs to the present state of affairs" is

strong enough full employment will be reached and then the rise in

the rate of interest would perform the task of stopping "inflation"

and create the "eqilibrium" represented by point A

In any case however, the process of reaching this equilibrium will

be in general spread over many 7 periods. Thus it is interesting to

know what determines the rate of investment decisions during the

process. I sought [sic] of solving this problem by introducing the

principle" of increasing risk and this enabled me to describe the

course of reaching point A (Fig. 6)

I think however that the reference to increasing risk (or something

like that) is necessary also for adequate explanation of various posi-

tions of "equilibrium" (positions in which the rate of investment has

no tendency to change). For the facts show the prices of new in

vestment goods are relatively rigid. It follows from the statistics of

Mr. Kuznets about gross capital formation that the prices of new

investment goods have fallen in U.S.A. between 1929 and 1932 only

by 15%. Thus it is clear that the gap between prospective rate of

profit and the rate of interest was much lower in the depression than

in the prosperity. But then something besides the prices of invest-

ment goods is required for the formation of equilibrium."

18. This conclusion reads, "the rate of investment decisions is an increasing function

of the gap hetween the prospective rate of profit and the rate of interest.”

You question also my explanation of why it is the rate of investment decisions which is dependent on the gap between prospective

rate of profit and the rate of interest. If in first τ period all capitalists

have decided to invest, say, £l.000.000.000 the savings of second T

period will be £1.000.000.000 too. Thus precisely this amount can be

freely reinvested in the second r period-if the gap between pro-

spective rate of profit is the same as in the first r period-because the

investment of new accumulated capital does not increase the risk

(The existence of pure rentiers creates some complication but does

not affect the argument; if the relation of the net indebtedness of ar

entrepreneur to his wealth is δ and his saving during a given period

s-he can invest without increasing risk the amount s(1 + δ), The

sum of this [sic] amounts is Σ(1 +8) Ss + Σ6s where Ss is the

total saving of entrepreneurs and Σ8s is the total saving of"pure"

rentiers, or the sum of amounts to be invested without increasing

the risk is the total saving S)

I am very sorry for troubling you with this long discussion.

Yours sincerely,

[signed] M. Kalecki

「THE REVIEW OF ECONOMIC STUDIES

art lies below OL. In other words, there exists

» a value of investment IA to which corresponds a

value of investment decisions DA equal to 1A, while

for investment lower than 1A we have D>1, and

or investments higher than Ia the opposite, i.e.

D<I. There are, a priori, three possible positions

of the curve ф besides that shown in Fig. 3 (see

Fig. 4). We shall show that they are unrealistic. It

is easy to show that if the curve lies entirely above

OL, or, which is the same, if D is always greater than

I, we shall have an unlimited cumulative upward

process. For if in a certain r-period there corresponds

to investment I a higher amount of investment decisions D, then in the next

7-period the investment will be higher; but because the curve ф lies above

.OL the investment decisions in the second r-period are again higher than the

investment, and so on. In that way the investment would increase auto-

matically without limit.

FiG. 3

Fig. 4

This is, however, impossible, for the limited amount of available labour

does not permit investment and income to pass a certain level. What is the

mechanism by which the cumulative process is stopped? In the neighbourhood

of full employment the rise of nominal wages corresponding to every small

increase of investment (measured in wage-units) will be very sharp. It will

cause a rapid rise of nominal income, of demand for money, and thus of the

rate of interest. In that way the latter will soon reach the level at which

investment decisions are equal to investment and thus there will be no tendency

for a further rise of investment. But it all amounts to nothing more than the

demonstration of the feature in question of the function φ. Because of the

rapid rise of the rate of interest with the increased investment in the neighbour-

hood of full employment, the shape of this function must be such that the

curve MAN cuts the straight line OL in a point, which cannot lie above the

investment level corresponding to full employment. But it is clear that it

may lie lower. For the investment in successive r-periods may form a con-

vergent series even without the restraining influence of the rate of interest.」

Cambridge,] April 12, 1937

Dear Kalecki

I have your letter of April 4th. We have now got to the point where

I must distinguish between what I am entitled to say to you as editor,

and my remarks I am moved to make as a private critic. [Keynes

then provides comments under both these headings and then turns to

Kalecki's discussion in his letter of his Review of Economic Studies

article:]

One word about pages 4 and 6 of your letter. On page 419 your

argument seems to me a version of Achilles and the tortoise, and you

are telling me at the bottom of the page that even though Achilles

does catch the tortoise up, it will only be after many periods have

passed by. At the bottom of page 520 I feel that you are making too

much of a discontinuity between your periods. I quite agree, how

ever, that the amount of unexecuted decisions which the entrepre-

neurs are ready, so to speak, to have at risk, is an important element

in holding up the pace of investment and cannot be neglected. It is

only the precision of your conclusion which I was criticising

Meanwhile I return the article in the hope that you will preface it

with a catalogue of your assumptions. For it is not fair to the reader

that he should be forced to disentangle them for himself and then

wonder whether or not you really are making them.

Yours sincerely,

[copy initialed] JMK

19. The reference is to the paragraph beginning "May I yet make in Kalecki's

letter. and to its third sentence in particular-opposite which Keynes had jotted down

Achilles and the tortoise" (see p. 96 above)

20. The reference is to the paragraph beginning "You question also. .." in Kalecki's

letter.

I do not know whether or not there was any further correspondence

on Kalecki's 1937 Economic Journal paper; in any event, none has

survived. The next letter related to chapter 3 above is the one in which

Keynes acknowledged the receipt of the proofs of Kalecki's Essays in

the Theory of Economic Fluctuations (1939):

King's College,

Cambridge

January 7th, 1939

My dear Kalecki,

Thank you very much indeed for sending me proofs of your book

I have not compared them with the original articles to see how much

you have modified them. But I get the impression of immensely

improved lucidity. I have found them exceedingly clear and in-

telligible and most agreeable (and almost easy) reading. It will be a

most valuable work

The article which I am writing for the March Journal21 is mainly

concerned with matter you discuss in your first essay.22 I had been

making several references to the [1938] Econometrica version of

that, and will now correct these so as to refer to the book. I am also

dealing, to a certain extent, with what you discuss in your new essay

on Real and Money Wages. But in actual fact, what I am writing

does not overlap with that essay nearly so much as the titles suggest.

You are considering what happens to real wages when money wages

are reduced, so to speak on purpose, other things being equal;

whereas I am considering what happens to real wages when there is

a change in the output which is what you are dealing with much more

in your first essay.

There is, by the way, one small statistical point where perhaps

you can help me. On page 14 you mention that according to Bowley

the labour share was 41.4 per cent in 1880. In the Table on page 16

you give a figure comparable to more recent figures for 1911. Is it

safe to add the 1880 figure to this table, or does that require some

modification in order to be comparable?

Yours sincerely,

[signed] J. M. Keynes

In(23 the last essay I don't really [?] follow why the fact that only

21. "Relative Movements of Real Wages and Output 1939). This was Keynes' reply

to Dunlop's (1938) and Tarshis' (1939) empirical criticisms of his statement in the General

Theory (p. 10) that "the change in real wages associated with a change in money wages

so far from being usually in the same direction, is almost always in the opposite direction.

22. Entitled "The Distribution of National Income."

23. Handwritten postscript. The misprints Keynes lists here remain in the published

version of the book, which suggests that Kalecki sent the proofs at too late a stage for any

changes to be made in them. Accordingly, I find it difficult to accept Osiatyński's state-

ment (editorial note in Kalecki, Dzieta [Works], vol. I, p. 517) that the proofs were sent to

the entrepreneurs save makes the system trendless.

Misprints p. 127 sequencies-delete the i

p. 145 cracs (under the diagram)-what is this, it sounds more Polish than English!

If Kalecki wrote a reply to this letter, it has not survived.

That is all of the surviving Keynes-Kalecki correspondence that

refers to writings discussed in chapter 3 above. I cannot however

resist the temptation to go beyond the bounds of that chapter and

reproduce the following correspondence between Keynes and Kalecki

on a subject that has long interested me: namely, what I first

called the "Pigou effect" of a declining price level, and subsequently

relabeled the "real-balance effect:

[Cambridge,] February 22, 1944

Dear Kalecki,

Looking through your note on Pigou again,24 the following point

occurs to me. Is there anything in it? I offer it to you, for what it is

worth, as a possible addition

On Pigou's assumption, the real rate of interest in Irving Fisher's

sense would be constantly rising. This would have two effects

(a) People would save more, and not less, as Pigou assumes

(b) If the real value of money is constantly increasing, there will

be a strong pressure to repay debts. Thus, at the limit, it would

become impossible for the banks to keep the stock of money con-

stant except in so far as it was backed by gold.25 Thus, in effect,

Pigou is assuming simultaneously two contradictory hypotheses

And would even the creation of more national debt help, since this

would increase personal incomes pari passu?

Yours sincerely,

[copy initialed] K

Keynes because he was supposed to write a foreword to the book, and that illness

prevented his doing so. Nor is there any indication in Keynes letter that this was the

purpose for which the proofs were sent to him.

24. The reference is to Kalecki's Professor Pigou on the 'Classical Stationary

State' "(1944), which was a comment on the article by Pigou (1943) in which the "Pigou

effect was first presented. Both of these articles appeared in the Economic Journail

25. Keynes does not seem to realize that this is precisely the point of Kalecki's note

as the latter makes clear in paragraph (2) of his reply, which follows.

University of Oxford

Institute of Statistics

28th February 1944

Dear Lord Keynes,

Thank you very much for your letter. May I make the following

observations on your points?

(1) Your point on the rising real rate of interest is valid only in the

period of adjustment. Once new equilibrium is achieved the wages

and prices stop falling. In the course of adjustment the factor you

mention will tend to reduce employment, but an even more impor-

tant influence in this direction will be exerted by whosesale

bankruptcy and the resulting "crisis of confidence" which I mention

in my note.

(2) The repayment of bank debts will not affect the situation after

the correction I suggest has been introduced: in any case it is only

the increase in the real value of gold that matters.

(3) If in the initial situation there exists a large National Debt this

makes Pigou's adjustment easier because the increase in the real

value of the National Debt does mean an increase in the real wealth

of firms and persons. (If the interest on Debt is financed by taxation

its existence does not affect the aggregate disposable income.26)

Yours sincerely,

[signed] M. Kalecki

[Cambridge,] March 8, 1944

Dear Kalecki

I agree that the real rate of interest would not go on rising for ever

But I should have supposed that at the time when it reached its

equilibrium level substantially all bank loans would have been paid

off. Thus, I do not see how the banking system is going to maintain

the quantity of money constant unless it is prepared to issue national

debt as a backing for it. Assuming that interest is paid on this out of

taxation, it cannot affect the wealth of the community one way or

another. Thus, it seems to me that Pigou is in reality depending

entirely on the increase in the value of gold.

The whole thing, however, is really too fantastic for words and

scarcely worth discussing.

Yours sincerely,

[copy initialed] K

It is not clear whether "the whole thing" in this last paragraph refers to

the specific point which Keynes raises in these letters or to Pigou's

analysis in general. If the latter, then it supports my conjecture that

even if Keynes had taken account of the real-balance effect in the

General Theory, it would not have affected his basic conclusions

(KMT, p. 110; see also my "Price Flexibility and Full Employment"

[1951], p. 281, and Money, Interest, and Prices, chap. XIV:1).

26. Note Kalecki's view (with which Keynes in the reply which follows concurs) that

government debt serviced by taxation is not part of wealth. In the last two decades this

question has received increasing attention: thus see, e.g., chap. XII:4 of my Money

Interest, and Prices (1965) and Barro (1974).

________

Kalecki, Michal, "A Theory of the BusinessCycle." Review of Economic Studies, Vol. 4, No.2, February 1937, pp. 77-97, revised and reprintedin [14], pp. 116-49.

http://crecimientoeconomico-asiain.weebly.com/uploads/1/2/9/0/1290958/kalecki_1937_-_a_theory_of_the_business_cycle.pdf

p.87We can now discover some further features of the function T which is represented here in Fig. 3. We shall try to show that the curve MAN representing this function must cut the straight line OL, drawn at 450 through the zero point 0, and that the left part MA lies above, whilst the right part AN lies below OL. …

p.87We can now discover some further features of the function T which is represented here in Fig. 3. We shall try to show that the curve MAN representing this function must cut the straight line OL, drawn at 450 through the zero point 0, and that the left part MA lies above, whilst the right part AN lies below OL. …

( 経済学、リンク::::::::::)

Ivar Jantzen 1939 「45度線分析」の創始者

http://nam-students.blogspot.jp/2016/03/ivar-jantzen-1939.html

NAMs出版プロジェクト: ケインジアンの交差図

http://nam-students.blogspot.jp/2015/03/blog-post_12.html

http://nam-students.blogspot.jp/2015/03/blog-post_12.html

鍋島論考

カレツキの貨幣経済論 :ケインズとの対比において

鍋島直樹

鍋島直樹『ケインズとカレツキ』に再録されている。第七章159頁に対応。多少の変更はある。

鍋島論考

一橋論叢 第104巻 第6号

Ⅳ 投資制約要因としての「信用の利用可能性」

さて, カレツキは「危険逓増の原理」によって投資量の決定を説明したのだ

が, これに対してケインズはどのような態度を示したのか, そして両者の貨幣

および経済メカニズムの理解にはどのような相違が存在するのか, とりあ

えず1つの手がかりとしてカレツキの主張に対するケインズの見解をみてゆく

ことにしよう.

ケインズは1937年3月30日のカレツキあての手紙において, Kalecki[1937

a]に対するコメントというかたちで,「予想収益に関する危険は,資本の限界

効率についての私の定式化においてすでに考慮されています」(Keynes [1983]

p. 793) と語っている. そして,投資の限界効率の概念によっては投資量を決

定することができないというカレツキの批判に対しては,「現在の価格上昇が

将来価格についての期待に不相応な(disproportionate)影響を及ぼすであろ

うというだけでなく,将来価格が〔現在と〕同じ割合で上昇するであろうと予

想される, とあなたは想定しているように思われます. まさに, これは長期期

待に対する即時的状態の影響の法外な過度の強調ではないでしょ うか」(同上,

p. 793, 〔 〕内は引用者のもの) と答えている. さらに同年4月12日の手紙

では,「あなたの議論は, アキレスと亀の説明のように私には思われます. あ

なたは私に, たとえアキレスが亀に追いつくとしても, それは多くの期間

が経過した後にのみであろうと語っているのです」(同上, p.798)としてカレ

ツキの見解に反論を加えているもちろん, ここで「アキレス」とは投資量を,

「亀」とは一般物価水準のことを指している. ともかく も, ケインズはカレッ

キの自らに対する批判は当たらないとし, 自らはすでに資本の限界効率概念の

なかで,投資量の増大に伴なう危険逓増を考慮していると述べたのである

以上のケインズの主張についてであるが,実際のところ,彼が『一般理論』

において「危険逓増」の問題を考慮していたとみなすのは難かしい.周知のよ

うに, ケインズは『一般理論』第11章において,投資量の決定について, (1)

資本の限界効率と利子率の均等, (2)投資財の需要価格と供給価格の均等, と

いう 2通りの解決を提示した(1)では資本の限界効率の低下を生産物供給量

の増加による企業間競争の発生と生産設備価格の上昇によって説明し,資本の

限界効率が利子率に等しくなる点まで投資が進められるとされている一方,

(2)では「借手のリスク」と「貸手のリスク」に言及し, この2種類のリスク

の逓増が投資財の需要価格·供給価格に影響を及ぽすことにより投資を制約す

るとされている. そしてケインズ自身はこれら2通りの解決を事実上同じもの

であるとみなして,主に(1)の方法に基づきながら『一般理論』の叙述を展開

した.だがミンスキーは(1)を「標準的モデル」,(2)を「資本化モデル」と名づけて,2つは内容の異なるものであると考える.彼は,「選択をしたときには何等差異がないように見える選択が,具合の悪い結果をもたらす揚合がある

のと同様,〔標準的モデル〕の選択も振り返ってみれぱ不幸な結果をもたらし

てしまった」(Minsky[1975]邦訳153頁,〔〕内は引用者のもの)とし,

「ケインズがこのようなモデルを選んだために,彼にとっては資金貸付の一属

性にすぎない利子率が,モデルの中枢として不当に強調されることになってし

まった」(同上,157頁)と論じている15).ミンスキーの説明からも明らかなよ

うに,もしケインズがカレツキあての手紙において語ったように,資本の限界

効率概念において投資増カロに伴なう危険逓増を考慮していたのであれぱ,ミン

スキーのいう「資本化モデル」を選択するべきであった.ところが実際にはそ

うしなかったのである.すなわち,ケインズは投資の大きさにかかわらず企業

に対する貸付利子率は一定であり,またそれは金融の源泉から独立であるとみ

なした.このようにケインズはカレッキとは異なり,モディリアーニ=ミラー

の世界にとどまることになるのである、少なくとも『一般理論』においては,

ケインズは投資の金融的側面を捨象することになってしまったと言ってよいだ

ろう.たとえぱカーンも「ケインズは,投資の決定要因として危険のない利子

率の一他の諸要因に比しての一重要性を誇張した点で,当然に批判されて

よい」(Kahn[1984]邦訳228頁)と指摘している.

これに対して,カレツキは投資・生産過程において信用の利用可能性の演じ

る役割の重要性を強調する.投資の増加に伴う危険逓増が作用するとされてい

るカレッキの世界では,投資の増加にしたがって資金調達費用が上昇すること

により,同時に,投資に対する予想収益も低下してゆくことになる.ここでは

借手のリスクと貸手のリスクが投資決定に対して大きな影響力をもつ.この視

点がミンスキーのtwo-price-level model 16〕において中心的な役割を果たして

いることはよく知られているところである.ミンスキー自身,借手のリスク

およぴ貸手のリスクという用語は,ケインズの『一般理論』にもみられるが,

通常は,カレツキに帰せられている」(Minsky[1986]邦訳234頁)と述べて

いるように,ミンスキーの投資決定理論はカレッキ理論の発展線上にあるもの

と言っても間違いではないだろう.彼は自らのモデルの想源を主としてケイン

ズの「資本化モデル」に求めているけれども,それはカレッキの「危険逓増の

原理」とも密接な関係をもつのである(17).

(136)

(17) ミンスキーは,「借手のリスクおよぴ貸手のリスクという用語は,カレツキの造語である」(Minsky[1986〕邦訳262員)としているが,管見の隈りではカレツキの文献にそのような用語は見当たらない一ただしいくつかの文猷においてそのような概念が用いられていることは確かである.たとえばKalecki[1937a]では「貸り手の確信」(lender’s confidence)という周語が使用されており,事業の状態に対 する銀行の判断を指している一これは貸手のリスクに対応するものと考えてよい.この論文では,2種類のリスクのうち主に貸手のリスクに注目している.またKalecki[1937b]では,第III節において見たように,危険逓増を(1)事業の失敗の場合の富の状態の危険性,およぴ(2)「非流動性」の危険性,によって説明したが,(1)は明らかに事業者の側にかかるもので,借手のリスクとみなされうるし,(2)についても主に借手のリスクに関係するものと恩われるが,カレツキ自身は,「もし企業者が投資活動において注意深くなけれぱ,自らの計算に基づき,利子率を引き上げることによって一定量を超える信用の継続部分に危険逓増の負担を課するのは債権者である」(同上,p.442)として貸手のリスクにも注意を払っている.このように,カレツキは「借手のリスク」「貸手のリスク」という用語こそ使っていないものの,実質的にそれと同じ概念を用いることによって投資決定理論を展開している。しかしながら,これら2種類のリスクが明確に分類されていないことも事実であり,そのどちらを重視しているのかも文猷によってまちまちである.この点において,カレツキの「危険逓増の原理」はケインズの「資本化モデル」あるいはミンスキーのtwo-price-leve-modelに比べると,やや未発達の感がある.

鍋島は以下ミンスキーを参照している。

Minsky, H. P.

[1975], John Maynard Keynes, New York: Columbia University

Press (堀内昭義訳『ケインズ理論とは何か』岩波書店,1988年)

[1982], Can "It" Happen Again?_Essays on Instability and Finance

Armork, New York : M. E. Sherpe (岩佐代市訳『投资と金融-資本主義経済

の不安定性』日本経済評論社, 1988年)

[1986], Stabilızing an Unstable Economy, New Haven, Connecticut: Yale

Universiy Press (吉野·浅田·内田訳『金融不安定性の経済学-歴史·理論

政策』, 多賀出版, 1989年).

[1989], Financial Structures: Indebtness and Credit', in Barrère, A

(ed.), Money, Credit and Prıces in Keynesian Perspective, London: Macmillan

宮崎義一·伊東光晴[1961],『コンメンタール·ケインズ一般理論』日本評論社.

Kahn, R. F. [1984], The Makrng of Keylees' General Theory, Cambridge : Cam-bridge University Press

邦訳カーン『ケインズ一般理論の形成』岩波

( 経済学、リンク::::::::::)

カレツキ:「投資と資本家消費が利潤と国民所得を決定する」という命題

http://nam-students.blogspot.jp/2012/01/blog-post_17.html

ミハウ・カレツキ (Michal Kalecki):マクロ経済学の知られざる英雄

http://nam-students.blogspot.jp/2015/10/michal-kalecki.html☆

ヒックスが『価値と資本』#17(邦訳文庫下67,73頁参照)で用例を借りたという以下のカレツキの論文は未邦訳のようだ。 追記:1944年に邦訳あり。

カレツキ:「投資と資本家消費が利潤と国民所得を決定する」という命題

http://nam-students.blogspot.jp/2012/01/blog-post_17.html

ミハウ・カレツキ (Michal Kalecki):マクロ経済学の知られざる英雄

http://nam-students.blogspot.jp/2015/10/michal-kalecki.html☆

ヒックスが『価値と資本』#17(邦訳文庫下67,73頁参照)で用例を借りたという以下のカレツキの論文は未邦訳のようだ。 追記:1944年に邦訳あり。

The Principle of Increasing Risk 1937

http://www.redeco.economia.unam.mx/home/Pdf/bibliografia/Kalecki_The_principle_of_increasing_risk.pdf原文全9頁

なお、鍋島直樹『ケインズとカレツキ』第7章155~6,198頁でこの借り手のリスクについて触れた「危険逓増の原理」1937が図解付きで解説されている(同159頁)。

中小企業ほど投資のリスクが大きいから規模の格差は決して解消されないのだ。

(ヒックスは計画期間と利率の関係を考察しただけだったが)

(ヒックスは計画期間と利率の関係を考察しただけだったが)

投資量の決定:

(a)伝統的理論(ケインズ):

投 資 の

|。 。 限 界

| 。 効

|__________。____

| | 。率

|b |

| | 。

|__________|____

|p |

|__________|_____

k0 k

(b)カレツキ:

| 。

| 投資の限界効率 。

|__________。____

| 。 |

| 。 。 |

| b |

|__________|____

| p |

|__________|_____

k0 k

危険逓増の原理 カレツキ The Principle of Increasing Risk ,Kalecki ,1937

(a)伝統的理論(ケインズ):

投 資 の

|。 。 限 界

| 。 効

|__________。____

| | 。率

|b |

| | 。

|__________|____

|p |

|__________|_____

k0 k

(b)カレツキ:

| 。

| 投資の限界効率 。

|__________。____

| 。 |

| 。 。 |

| b |

|__________|____

| p |

|__________|_____

k0 k

危険逓増の原理 カレツキ The Principle of Increasing Risk ,Kalecki ,1937

《まず投資規模kは,投資の限界効率MEIが利子率ρと投資に伴なうリスク率σの総和に等しくなる水準に決定されるとカレツキは想定する。そうすると図(a)から容易に理解されるように,伝統的理論においてはkの増大とともにMEIが低下する場合にのみ,一定の最適投資量k0が決定されることになる。一般にこのような下落は(1)大規模化の不経済,(2)不完全競争,によって発生するとされている.しかしカレツキは(1)の理由は非現実的であるとし,(2)についても,より現実的ではあるが,これによっては同時に異なる規模の企業が存在することが説明されないと言う.したがって企業規模の相違を説明する他の要因が存在するはずである.》

《カレツキによるとリスク率σは投資量とともに増大するという(図(b)).そしてその理由として次の2つが挙げられている.第1は,投資量が大きくなるほど事業の失敗における富の状態が危険になるといることであり,第2は,「非流動性」の危険性の存在, すなわち投資量の増大にしたがい,その主体の資産ポートフォリオに占める実物資産の割合が高まるということである.》

《…投資量の増大にしたがってその危険が逓増する場合には, 投資量はMEI[投資の限界効率]が一定のρおよび投資量とともに増大するσの総和に等しくなる点k0に決まる。そして企業の内部蓄積の増加(減少)は限界リスク曲線を右(左)にシフトさせるので、単一企業の投資決意率は,その資本蓄積と限界収益性の変化の速度に依存する」(Kalecki[1937b]p.447)ということになる。また以上から、同一産業における企業規模の相違の存在を説明することも可能となる。企業者はそれぞれ異なる量の白己資本を保有し,異なる規模で生産活動を開始する。だが自己資本の小さい企業者ほど投資の増加に伴う危険逓増にさらされやすい。彼らにとって生産規模の拡張は大企業者に比べると困難であり、よって企業規模の格差は温存されることになる.すなわち、「〈ビジネス・デモクラシー〉〔という仮定〕は誤りである.自己資本は〈投資の一要因〉となる」(同上,p.443,〔〕内は引用者のもの)。》鍋島

:156頁

The Money Market

投資ファイナンスと貨幣市場:

_________

| | _________

| | | |

| _____⬇︎___ ___⬇︎__ |

| | 「未拘束」預金 | | | |

| |_________| | | |

| | | | |

| I1 | 信用 | |

A1 _____⬇︎___ | | A2

| | 投資準備 |← →| | |

| |_________| | | | | |

| | | | |______| |

| A I1 I2 |

| _____⬇︎___ |

| | 流通貨幣 | |

| |_________| |

|_______| |______________________|

Kalecki[1933a]p.96

_________

| | _________

| | | |

| _____⬇︎___ ___⬇︎__ |

| | 「未拘束」預金 | | | |

| |_________| | | |

| | | | |

| I1 | 信用 | |

A1 _____⬇︎___ | | A2

| | 投資準備 |← →| | |

| |_________| | | | | |

| | | | |______| |

| A I1 I2 |

| _____⬇︎___ |

| | 流通貨幣 | |

| |_________| |

|_______| |______________________|

Kalecki[1933a]p.96

OUTLINE OF THE BUSINESS CYCLE THEORY

1990 Collected Works of Michal Kalecki. Volume 1. Capitalism: Business Cycles and Full Employment, ed.

by Jerzy Osiatynski, Oxford: Oxford University Press.

鍋島直樹『ケインズとカレツキ』180頁参照

鍋島直樹『ケインズとカレツキ』180頁参照

投資決意と現実の投資との間にAというギャップがある

(発券銀行を含む全ての銀行についての統合された)バランスシート

負債項目 資産項目

‘unattached’ deposits

investment reserves

money in circulation

credits

「未拘束」預金

投資準備

流通貨幣

信用

:180,278頁(カレツキ別論文より)

「新しい投資準備の形成は、未拘束預金からの転換I1と銀行信用の拡大I2によって賄われる…。粗蓄積Aから未拘束預金に還流する部分をA1,同じく粗蓄積からの銀行への返済に用いられる部分をA2と表すならば、投資財に対して支出される額はA=A1+A2と表される。これより、投資準備の増加分I-Aは次のように表現することができる。

「新しい投資準備の形成は、未拘束預金からの転換I1と銀行信用の拡大I2によって賄われる…。粗蓄積Aから未拘束預金に還流する部分をA1,同じく粗蓄積からの銀行への返済に用いられる部分をA2と表すならば、投資財に対して支出される額はA=A1+A2と表される。これより、投資準備の増加分I-Aは次のように表現することができる。

I-A=(I1-A1)+(I2-A2)

I1-A1が未拘束預金の減少分を、I2-A2が銀行による信用膨張による部分をそれぞれ表している…。このようにして、産出水準の上昇には銀行組織による信用膨張が不可避的に随伴する…。」(180~1頁)

投資リスクにおいてカレツキとケインズは意見がくい違ったという。このあたりも鍋島論文に詳しい。

《1937年の4月12日付の(注:ケインズからカレツキへの)手紙

では,投資誘因に関するカレツキの議論について,「あなたの議論は,アキレ

スと亀の寓話の改作版であるように私には思われます。あなたは私に,……た

とえアキレスが亀に追いつくとしても,それは多くの期間が経過したのちにお

いてだけであろうと語っているのです」(ibid☆,p.798)と述べて,カレツキの

見解に反論を加えている。いうまでもなく,ここで「アキレス」とは投資額

を,「亀」とは一般物価水準のことを指している。カレツキの説明において投

資の増加が物価の上昇を引き起こすという過程が繰り返されるのは,寓話のな

かでアキレスが永遠に亀に追いつくことができないのと同じようなものだとい

うわけである。ともあれケインズは、カレツキが自らに向けた批判は当たらな

いものであるとし,投資の増加にともなう危険の逓増は、すでに『一般理論』

における資本の限界効率の定式化において考慮されていると主張した(ibid,

p.793)。

しかしながら,実際のところ,ケインズが『一般理論』において危険逓増の

問題を考慮していたという主張をそのまま受け取ることは難しい。…》

(鍋島論考158頁)

☆

ケインズのカレツキへの手紙は以下に所収されているという。

The Collected Writings of John Maynard Keynes; Volume XII: Economic Articles And Correspondence; Investment and Editorial (Volume 12)

関連論考:

Formal modelling vs. insight in Kalecki's theory of the ... D Besomi

http://www.unil.ch/files/live//sites/cwp/files/users/neyguesi/public/Besomi.pdf

52 Kalecki to Keynes, 4 April 1937, in Kalecki 1990, p. 525 (the point is also made in Kalecki 1939, p. 140: “It is true that […] the system always moves towards the point B, but it may, of course, take several τ periods to come close to it. Thus the time of adjustment is considerable (τ is more than half a year)”. Keynes did not think much of this approach: “your argument seems to me a version of Achilles and the tortoise, and you are telling me […] that even thought Achilles does catch the tortoise up, it will only be after many periods have passed by. […] I feel that you are making too much of a discontinuity between your periods” (letter to Kalecki, 22 April 1937, in Kalecki 1990, pp. 525– 26).

1990 Collected Works of Michal Kalecki. Volume 1. Capitalism: Business Cycles and Full Employment, ed. by Jerzy Osiatynski, Oxford: Oxford University Press.

Collected Works of Michal Kalecki: Volume 1: Capitalism: Business Cycles and Full Employment (Collected Works of Micha Kalecki): 9780198285380: Economics Books @Amazon.com

http://www.amazon.com/Collected-Works-Michal-Kalecki-Capitalism/dp/0198285388/ref=la_B001HPZFVQ_1_4?s=books&ie=UTF8&qid=1444217043&sr=1-4http://www.amazon.co.jp/Collected-Works-Michal-Kalecki-Capitalism/dp/0198285388/

以下の論考でも同カレツキ論文が言及されている。

栗田康之 :カレツキの資本主義経済論 - 宇野理論を現代にどう活かすか (Adobe PDF)

www.unotheory.org/files/No8/newsletter_2-8-2.pdf カレツキの経済理論は、そのような学説史的関係も含めて、独占度、有効需要理論、景 ...... し手のリスク」および「借りてのリスク」)を緩和することによっても、投資を拡大させ ..... Kalecki,M.[1937]“The Principle of Increasing Risk”,Economica,vol.4,no.16.

マルクス再生産表式にかんしては

邦訳1958,47頁利潤の決定要因でカレツキ自身が触れている

この新評論社版は訳注54頁もある

《 いま考察している問題の理解のために,いくらか異なった視角から,上述

したところを示してみるのも無意義でないだろう.マルクスの「再生産表式」

にしたがって,全経済を3部門に分割するものとしよう.第Ⅰ部門は投資財

を生産し,第Ⅱ部門は資本家用消費財を生産し,第Ⅲ部門は労働者用消費財

を生産する.第Ⅲ部門の資本家は,労働者たちにその賃金相当額の消費財を

売却してもなお,みずからの利潤に等しい額の消費財の剰余部分を手許にの

こすだろう.これらの財は,第Ⅰ部門と第Ⅱ部門の労働者に売られるが,か

れらは貯蓄をしないから,それはかれらの所得に等しいだろう.かくして利

潤の総額は,第Ⅰ部門の利潤と第Ⅱ部門の利潤と,そしてこれら両部門の賃

金との総和に等しいであろう·すなわち,利潤の総額は両部門の生産物の価

値,換言すれば,投資財生産と資本家用消費財生産の価値に等しいだろう. (a)☆

もし,全部門にわたって利潤と賃金の間の分配がきまっていると,第Ⅰ部

門の生産と第Ⅱ部門の生産は第Ⅲ部門の生産をも決定するであろう.第Ⅲ部

門の生産費は, この部門の生産から得られる利潤が第Ⅰ部門と第Ⅱ部門の賃

金に等しくなる点まで拡張されるであろう.あるいは,別の表現をとれば,

第Ⅱ部門の雇用量と生産量は, この部門の生産量からこの部門の労働者が

の賃金で辟入する量を差し引いた残額を,第Ⅰ・第Ⅱ部門の賃金に等置する

点まで,拡張されるであろう.》

(47頁)

☆

《第3章の訳者注

(a)この関係をマルクス流に不変資本(ただし仮定により減価償却費部分のみ

からなり,原料費部分は含まない)cと可変資本vと剰余価値mであらわす

とつぎのようになる.

第Ⅰ 部門=c1+v1+m1

第Ⅱ部門=c2+v2+m2

第Ⅲ部門 =c3+v3+m3

仮定により労働者の所得総計は労働者用消費財生産に等しいから

v1+v2+v3=c3+v3+m3 (i)

したがって,粗利潤の総計(純利潤プラス減価償却費)は第Ⅰ部門と第Ⅱ部門

の生産物の価値合計に等しくなる.

なせならば(i)式によって

v1+v2=c3+m3

だからである.》

(54頁)

邦訳1958,47頁利潤の決定要因でカレツキ自身が触れている

この新評論社版は訳注54頁もある

《 いま考察している問題の理解のために,いくらか異なった視角から,上述

したところを示してみるのも無意義でないだろう.マルクスの「再生産表式」

にしたがって,全経済を3部門に分割するものとしよう.第Ⅰ部門は投資財

を生産し,第Ⅱ部門は資本家用消費財を生産し,第Ⅲ部門は労働者用消費財

を生産する.第Ⅲ部門の資本家は,労働者たちにその賃金相当額の消費財を

売却してもなお,みずからの利潤に等しい額の消費財の剰余部分を手許にの

こすだろう.これらの財は,第Ⅰ部門と第Ⅱ部門の労働者に売られるが,か

れらは貯蓄をしないから,それはかれらの所得に等しいだろう.かくして利

潤の総額は,第Ⅰ部門の利潤と第Ⅱ部門の利潤と,そしてこれら両部門の賃

金との総和に等しいであろう·すなわち,利潤の総額は両部門の生産物の価

値,換言すれば,投資財生産と資本家用消費財生産の価値に等しいだろう. (a)☆

もし,全部門にわたって利潤と賃金の間の分配がきまっていると,第Ⅰ部

門の生産と第Ⅱ部門の生産は第Ⅲ部門の生産をも決定するであろう.第Ⅲ部

門の生産費は, この部門の生産から得られる利潤が第Ⅰ部門と第Ⅱ部門の賃

金に等しくなる点まで拡張されるであろう.あるいは,別の表現をとれば,

第Ⅱ部門の雇用量と生産量は, この部門の生産量からこの部門の労働者が

の賃金で辟入する量を差し引いた残額を,第Ⅰ・第Ⅱ部門の賃金に等置する

点まで,拡張されるであろう.》

(47頁)

☆

《第3章の訳者注

(a)この関係をマルクス流に不変資本(ただし仮定により減価償却費部分のみ

からなり,原料費部分は含まない)cと可変資本vと剰余価値mであらわす

とつぎのようになる.

第Ⅰ 部門=c1+v1+m1

第Ⅱ部門=c2+v2+m2

第Ⅲ部門 =c3+v3+m3

仮定により労働者の所得総計は労働者用消費財生産に等しいから

v1+v2+v3=c3+v3+m3 (i)

したがって,粗利潤の総計(純利潤プラス減価償却費)は第Ⅰ部門と第Ⅱ部門

の生産物の価値合計に等しくなる.

なせならば(i)式によって

v1+v2=c3+m3

だからである.》

(54頁)

ブランシャールを参照

346153759-Macroeconomics-7th-Global-Olivier-Blanchard.pdf ...

評価(評価: 5)評価:5-1件のレビュー

MacroeconoMics. Olivier Blanchard. Boston Columbus Indianapolis New York San Francisco Amsterdam Cape Town ...

- Blanchard, Olivier (2011). Macroeconomics Updated (5th ed.). Englewood Cliffs: Prentice Hall. ISBN 978-0-13-215986-9.

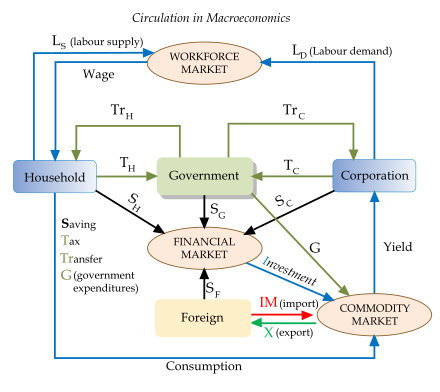

http://www.econguru.com/the-macroeconomics-circulation-flowchart/

Legends of the flows:

Legends of the flows:

- L stands for Labor.

- W can be used to stand for Wage.

- T stands for Tax.

- Tr stands for Transfer payments.

- G stands for Government expenditures.

- S stands for Savings made available in financial markets for investment.

- I stands for Investment from financial markets.

- IM stands for Import from foreign economies.

- X stands for eXport to foreign economies.

AO,MP自体がマルクスへの賛辞であり偉大さを示しているので新たな著作は必要ない

カラマーゾフの兄弟の続編みたいなもので

ドストエフスキーは読者の今この時が「ロマン」として大切だと言っていたのだ

マルクスの偉大さは資本主義に覆われた現在、自明だ

第7章

利潤の決定要因

資に関する過去に形成された資本家の決意によって決定されるのである。

以上で考察した問題を理解するために,いままで述べたことを若干異なった

視角から示しておくことは有益である。マルクスの「再生産表式」(schemes of

reproduction)に従って,経済全体を3つの部門に細分割するものとしよう。第

I 部門は投資財生産部門であり,第I部門は資本家用消費財生産部門であり,

第Ⅲ部門は労働者用消費財生産部門である。第Ⅲ部門の資本家は, 自らの部門

の労働者に賃金に相当する額の消費財を売った後になお,自らの部門の利潤に

等しい額の余剰消費財を手元に残すであろう。これらの財は第I部門と第II部

門の労働者に売られるであろうが,労働者は貯蓄をしないから,それは彼らの

所得に等しいであろう。かくして,総利潤は,第I部門の利潤,第Ⅱ部門の利

潤およびこれら2つの部門の賃金の合計に等しいであろう。あるいは,総利潤

はこれら2つの部門の生産物価値に,換言すれば,投資財と資本家用消費財の

生産物価値に等しいであろう。

もしすべての部門で利潤と賃金の間の分配が与えられているならば,第I部

門と第Ⅱ部門の生産が第Ⅲ部門の生産をも決定するであろう。第Ⅲ部門の生産

水準は,その生産によって得られる利潤が第I部門と第Ⅱ部門の賃金に等しく

なる点にまで拡張されるであろう。あるいは,別の言い方をすれば,第Ⅲ部門

の雇用量と生産量は, この部門の生産量から同一部門の労働者が賃金で購入す

る部分を差し引いた残余が第1部門と第II部門の賃金に等しくなる点まで拡張

されるであろう。

上述の議論は,利潤理論における「分配要因」,すなわち(独占度のような)所

得分配を決定する要因の役割を明らかにする。利潤が資本家の消費と投資によ

って決定されるものとすれば,「分配要因」によって決定されるのは, (ここで

は労働者の消費に等しい)労働者の所得である。このようにして,資本家の消

費と投資は「分配要因」と共同して労働者の消費を決定し,その結果国民産出

量と雇用を決定する。国民産出量は,「分配要因」に従ってそのうちから切り

出される利潤が資本家の消費と投資に等しくなる点まで拡張されるであろう1).

1)

上述の議論は,

供給が弾力的であるという第1部で設けられた仮定に基づいている。しかしながら…

資本主義経済の動態理論81頁日本経済評論社1984年

(索引になぜかマルクスの名が無い)

https://www.concertedaction.com/tag/michal-kalecki/

New Book: Vol II Of Michał Kalecki’s Intellectual Biography By Jan Toporowski

Posted on April 7, 2018 by V. Ramanan

Leave a reply

The General Theory of Employment, Interest and Money was published in January, 1936.

Meanwhile, … , Michal Kalecki had found the same solution.

His book, Essays in the Theory of Business Cycles, published in Polish in 1933, clearly states the principle of effective demand in mathematical form. At the same time he was already exploring the implications of the analysis for the problem of a country’s balance of trade, along the same lines that I followed in drawing riders from the General Theory in essays published in 1937.

The version of his theory set out in prose (published in ‘Polska Gospodarcza’ No. 43, X, 1935) could very well be used today as an introduction to the theory of employment.

He opens by attacking the orthodox theory at the most vital point – the view that unemployment could be reduced by cutting money wage rates. And he shows (a point that Keynesians came to much later, and under his influence) that , of monopolistic influences prevent prices from falling when wage costs are lowered, the situation is still worse, because reduced purchasing power causes a fall in sales on consumption goods …

…

Michal Kalecki’s claim to priority of publication is indisputable.

– Joan Robinson, Kalecki And Keynes in Essays In Honour Of Michal Kalecki, 1964.

Jan Toporowski’s intellectual biography, volume 2 of Michał Kalecki is out now.

ロビンソン

資本理論とケインズ経済学

45頁

カレツキーとケインズ

44頁

私は,はじめてミハウ·カレツキ---われわれの真新しい理論とすでに

親しんでいたばかりでなく,われわれの内輪の冗談のいくつかを発明さえし

ていた奇妙な訪問者--に会ったときのことをよく思い出す。それは,私に

ピランデルロ風の一種の感情--話しているのは,彼なのか私なのか--を

もたらした, 1934年の彼の論文を読むことによって(現在初めて英語で入

手することができる),私は同様の感情をもったのである.その頃,私は,

ケインズ理論を平易な言葉で説明しようとする--それほどの集中力もなし

にではあるが まさにそれと同じ論文を,何回か書いていたのであった.

カレツキーは,ケインズに対し, 1つの重大な強みをもっていた--つま

り,彼は,正統派経済学を学んだことがなかったのである『一般理論』の

序は,次のような言葉で終わっている、「著者が, ここに苦心して表明した

困難は,きわめて簡単であって,容易に理解されるはずである

諸概念は,新しい観念にあるのではなく,人々の心の隅々にまで拡がっている

旧い観念からの脱却である.」

:ロビンソン47頁

J.ロビンソン『資本理論とケインズ経済学』1988

50~1頁

《 ケインズは、道徳的および美学的理由から,現代資本主義にまったく嫌気

がさしていたが,彼は決して社会主義者ではなかった.ピラミッドを建造し

たり,地面に穴を掘りそれをふたたび埋めたりすることが,有効需要を維持

し, したがって,有益な生産の減少を阻止するであろうということを示した

後,彼は、次のように付け加えている。「しかしながら,ひとたび,われわ

れが,有効需要がそれらに依存する諸々の影響力を理解するならば,分別あ

る社会がこのような偶発的かつ浪費的な緩和策に依存したままで満足してい

るということは,合理的なことではない」[一般理論#16:3]と.彼は,ひとたび新しい理論が

理解されたならば,資本主義は自ら改革を行うであろう, と信じた.あるい

は,少なくとも彼がそれを望んでいることを認めていた. もし,有用な投資

によって,完全雇用が(人口の大きな増加を伴わずに) 1世代にわたって維

持されうるならば,貧困は消滅し去り,利子率は不労所得が経済の重荷とな

るのをやめるほど低下するであろう,正直な労苦と想像力に富む推察力のみ

が,社会によって報酬を与えられるであろう。(今次の大戦後,西欧におい

てはほぼ完全雇用に近い状態が,有用な投資によってではなく,穴を掘るほ

ど馬鹿らしさは少ないが,軍備を積み上げることによって維持されてきたの

をわれわれは知っている.ケインズの分析は正しいことが証明されたが,彼

の楽しい白昼夢は悪夢に変わってしまった.)

カレツキーは, それほど快適でない見通しをもっていた。大戦中に書かれ

た論文[完全雇用の政治的側面 原論文1943]において,彼は,次のように予言した.

商業的景気循環の原因が理解されたからには, その代わりに政治的景気循環が起こるであろう, と.政府は,財政赤字によって完全雇用政策を行うであろう.完全雇用が普及すれ

ば価格は騰高し,労働者の交渉上の立場は強力になるであろう.

「この状態において, ビッグ・ビジネス[大企業]と金利生活者の利益との間に強力

な連合が築かれることになりそうである.そして,彼らは,たぶん幾人もの

経済学者がそのような状態は明白に不健全であると宣告するのを知るであろ

う.」〔他方〕「健全財政」への復帰は失業をふたたびつくり出すであろう.

しかし,次の選挙が間近くなると,政府は,完全雇用という票集めの政策に

復帰するのである.》

参考:

カレツキ『資本主義経済の動態理論』147頁

カーンが

形成で引用したのは上ではなく、

xii

(4)) JOAN ROBINSON, Michal Kalecki on the Economics of Capitalism' in ÉPRIME ESHAG (ed.), "Michal Kalecki

Memorial Lectures', Oxford Bulletin of Economics and Statistics, Special Issue, February 1977, pp. 7-18.(引用

文は同誌8~9ぺージ); reprinted in JOAN ROBINSON, Collected Economic Papers, vol. V, Oxford: Basil

Blackwell, 1979, pp. 184-96. ( 引用文は同書186ぺージ)。

カーン

序文

ix

カレツキは,『一般理論』を執筆するために、勤めていたワルシャワの研究所から1年間の休暇を

とっていた。ストックホルムで彼にケインズの著書をくれた者がいた。彼はその本を読みはじめた。

ところが何とこれこそは、彼が自分で書こうとしていた本そのものであった。しかし、この本とて

もおそらくもっと後のところでは自分の考えているものと違ったところがあるに違いない、そう彼

は考えた。ところがそうではなかった。はじめから終りまで、彼の書こうとしていたものとそっく

り同じであった。カレツキは次のように言った。「告白しますが、私は病気になってしまいました。

三日間ベッドに臥せていました。それから考えました。ケインズは私よりもはるかに有名だ。この

考え方はケインズの名前でまたたく間に成功をおさめるだろう。そのあとで私たちはそれを応用し

た面白い問題に進むことができるのだ。それから私は起き上がりました」。......

カレツキは、生涯の終りに、自分はケインズに対して敵対的な主張をしないようにうまくやった、

という感慨を私にもらした。そのことをもし言い出せばうんざりするような話にしかならないだろ

う。私[ジョーン· ロビンソン]が彼の正当な権利を主張しているのをいぶかしく思う人たちは、現

在の堕落した時代にこのような高貴な考え方をする者がいることを信じ難くなっているためである。

タイトル ケインズ『一般理論』の形成

叢書名 岩波モダンクラシックス

著者名等 リチャード・カーン/〔著〕

著者名等 浅野栄一/訳

著者名等 地主重美/訳

出版者 岩波書店

出版年 2006.10

大きさ等 20cm 387p

注記 The making of Keynes’ general theory./の翻

訳

NDC分類 331.74

件名 ケインズ ジョン・メイナード

要旨 難解なことで知られる『一般理論』はどのように誕生したのか?ケインズの学問上の盟友

R.カーンが、20世紀最大の経済学者のダイナミックな思想展開を6回の講演でわかり

やすく解説。同時代の諸学説の影響や交友関係を通してケインズ理論の核心に肉薄する本

書は、初学者から研究者に至るまで必携のケインズ入門書である。

目次 第1講 初期ケインズ以前の経済学者への論評;第2講 貨幣数量説;第3講 『貨幣論

』と経済政策問題一九二八‐一九三一年;第4講 「乗数」から『一般理論』へ;第5講

『雇用・利子および貨幣の一般理論』;第6講 ケインズの個人的交友関係;討論

内容 「一般理論」はどのように誕生したのか。ケインズの学問上の盟友R.カーンが、彼のダ

イナミックな思想展開をわかりやすく解説。同時代の諸学説の影響や交友関係を通して、

ケインズ理論の核心に肉薄する入門書。

ケインズはヴィクセルと違って完全雇用を想定していない

カレツキもそうだが完全雇用の反動をケインズは知っていた

ヒトラーやニューディールールともそこが違う

投資の重要性はカレツキがやったように

マルクス再生産表式からも導き出される

ケインズはブルジョアを自認したが芸術にも投資した

審美眼がありなおかつお金の運用に対して責任を持っていたといえよう

『平和の経済的帰結』の権利を自分で保持した点は今日の知識人のお手本とさえ言える

マルクス役とエンゲルス役の一人二役をケインズは1人で行った

そうでなければ当時のチャーチルを批判したりは出来なかった

お金持ちになったらブルースなんて演奏できないのでは?

とジミヘンが言われてこう答えた

お金を稼げば稼ぐほどブルースはうまく演奏できるのさ、と

現在必要なのは持たざる者の自暴自棄な対抗運動ではなく

内在的かつ持続的な対抗運動だ

例えば労働の場では無理でも消費の段階でフェアトレード商品を選ぶことはできる

現在二つの階級が戦っているのではなく大きな中産階級が上下に引き裂かれつつある。

階級闘争は形を変えている。

また労働者自らが株主になるというような戦い方も有効だろう

投資の全否定ではそうした戦い方を見出だせない

また、ケインズ晩年の闘い、

国際通貨への闘いは一般に知られていない

アメリカのヘゲモニーが弱体化しつつある現在

再評価すべきだ事案だ

{kind=link}

13 Comments:

カレツキ - J-Stage (Adobe PDF)

www.jstage.jst.go.jp/article/peq/47/4/47.../_pdf

るが)検討するとともに,「景気循環理論概説」が1933. 年時点の『 ...... ─[1933(1990) ]Próba teorii koniunktury, Instytut Ba-.

CiNii 論文 - カレツキ経済学の基本構造の成立過程

ci.nii.ac.jp/naid/120005440809

論説本稿では, Kalecki(1933)において示された, 有効需要の論理に基づく利潤決定の理論に, Kalecki(1938)による ... of effective demand in Kalecki's 1933 work Próba teorii koniunktury (Essay on the Business ...

Title カレツキ経済学の基本構造の成立過程 Sub Title The economics ... (Adobe PDF)

koara.lib.keio.ac.jp/.../AN00234610-20040701-0059.pdf?...

Kalecki's 1933 work Próba teorii koniunktury (Essay on the Business Cycle Theory) and ... 解を踏まえれば,短期における国民所得の決定の理論が,カレツキ経済学の根底にあることが認め. られる。本稿では, ...

有効需要の理論 - 経済学史学会 (Adobe PDF) -htmlで見る

jshet.net/docs/journal/56/562nabeshima.pdf

第 I 部には,ケインズの『一般理論』が出現する以前の 1933 年,1934 年,1935. 年にそれぞれポーランド語で ...... 1933 a. Proba teorii koniunktury(Essays on the Business Cycle Theory). Warsaw: Institute of ...

このコメントは投稿者によって削除されました。

カレツキの貨幣経済論 :ケインズとの対比において

鍋島直樹

https://hermes-ir.lib.hit-u.ac.jp/rs/bitstream/10086/12562/1/ronso1040601240.pdf

鍋島直樹『ケインズとカレツキ』に再録されている。第七章159頁に対応。多少の変更はある。

http://2.bp.blogspot.com/-8IhzjVz35w0/VhSyDzsNw_I/AAAAAAAAyzQ/cyTDJIofQtA/s1600/nabeshima-kalecki-7.jpg

(a)伝統的理論(ケインズ):

投 資 の

|。 。 限 界

| 。 効

|__________。____

| | 。率

|b |

| | 。

|__________|____

|p |

|__________|_____

k0 k

(b)カレツキ:

| 。

| 投資の限界効率 。

|__________。____

| 。 |

| 。 。 |

| b |

|__________|____

| p |

|__________|_____

k0 k

危険逓増の原理 カレツキ The Principle of Increasing Risk ,Kalecki ,1937

《まず投資規模kは,投資の限界効率MEIが利子率ρと投資に伴なうリスク率σの総和に

等しくなる水準に決定されるとカレツキは想定する。そうすると図(a)から容易に理解

されるように,伝統的理論においてはkの増大とともにMEIが低下する場合にのみ,

一定の最適投資量k0が決定されることになる。一般にこのような下落は(1)大規模化

の不経済,(2)不完全競争,によって発生するとされている.しかしカレツキは(1)

の理由は非現実的であるとし,(2)についても,より現実的ではあるが,これによって

は同時に異なる規模の企業が存在することが説明されないと言う.したがって企業規模の

相違を説明する他の要因が存在するはずである.》

『ケインズとカレツキ』鍋島直樹(参照Kalecki1937)

《カレツキによるとリスク率σは投資量とともに増大するという(図(b)).そしてその

理由として次の2つが挙げられている.第1は,投資量が大きくなるほど事業の失敗における

富の状態が危険になるといることであり,第2は,「非流動性」の危険性の存在, すなわち

投資量の増大にしたがい,その主体の資産ポートフォリオに占める実物資産の割合が高まる

ということである.》同

《…投資量の増大にしたがってその危険が逓増する場合には, 投資量はMEI[投資の限界効率]が

一定のρおよび投資量とともに増大するσの総和に等しくなる点k0に決まる。そして企業の

内部蓄積の増加(減少)は限界リスク曲線を右(左)にシフトさせるので、単一企業の投資

決意率は,その資本蓄積と限界収益性の変化の速度に依存する」(Kalecki[1937b]p.447)

ということになる。また以上から、同一産業における企業規模の相違の存在を説明すること

も可能となる。企業者はそれぞれ異なる量の自己資本を保有し,異なる規模で生産活動を

開始する。だが自己資本の小さい企業者ほど投資の増加に伴う危険逓増にさらされやすい。

彼らにとって生産規模の拡張は大企業者に比べると困難であり、よって企業規模の格差は

温存されることになる.すなわち、「〈ビジネス・デモクラシー〉〔という仮定〕は誤り

である.自己資本は〈投資の一要因〉となる」」。》同

という認識が貨

幣の価値保蔵機能の重視に反映されていると思われるのである。だがここで注目すべきことは,流動性選好説をめぐってのロバートソン・オリーンらとの論争の過程において,ケインズが貨幣需要の4番目の動機として「金融動機」を導入したことである.ケインズは,1937年の論文r利子率の「事前的」理論」において,この金融動機を流動性選好説の「笠石」(copmgstone),すなわちその最後の仕上げをなすものと位置づけている(Keynes[1973]p・220).カーンはこのことについて次のような説明を行なっている.

「ケインズによる「金融」の概念の提示は,投資率の決定に関する『一般理論』の説明に対する重要な修正である.……ケインズはここで,利子率とはかかわりなくより重要な抑止カとして作用する,資金の利用可能性を導入した」(Kahn[1984]邦訳249-50頁).

ケインズによる金融動機の導入は彼の貨幣的分析をカレッキのそれに近づけるものと言ってよい.実際に,ケインズ自身,信用供与には一定の制限があるとして,「この指摘はカレッキ「景気循環の理論」〔Kalecki[1937a]〕……によってなされた」(Keynes[1973]P・208,〔〕内は引用者のもの)と述べ,この側面に関してのカレツキの先行性を認めている20)、ケインズによる金融動機の認識は,その世界観についてはともかく,少なくとも経

Kahn, R. F. [1984], The Makrng of Keylees' General Theory, Cambridge : Cam-bridge University Press (ケインズ一般理論の形成1987 LP).

ケインズ『一般理論』の形成 (岩波モダンクラシックス) 単行本 – 2006/10/24

リチャード カーン (著), Richard F. Kahn (原著), 浅野 栄一 (翻訳), 地主 重美 (翻訳)

ケインズ『一般理論』の形成

叢書名 岩波モダンクラシックス ≪再検索≫

著者名等 リチャード・カーン/〔著〕 ≪再検索≫

著者名等 浅野栄一/訳 ≪再検索≫

著者名等 地主重美/訳 ≪再検索≫

出版者 岩波書店

出版年 2006.10

大きさ等 20cm 387p

注記 The making of Keynes’ general theory./の翻

訳

NDC分類 331.74

件名 ケインズ ジョン・メイナード

要旨 難解なことで知られる『一般理論』はどのように誕生したのか?ケインズの学問上の盟友

R.カーンが、20世紀最大の経済学者のダイナミックな思想展開を6回の講演でわかり

やすく解説。同時代の諸学説の影響や交友関係を通してケインズ理論の核心に肉薄する本

書は、初学者から研究者に至るまで必携のケインズ入門書である。

目次 第1講 初期ケインズ以前の経済学者への論評;第2講 貨幣数量説;第3講 『貨幣論

』と経済政策問題一九二八‐一九三一年;第4講 「乗数」から『一般理論』へ;第5講

『雇用・利子および貨幣の一般理論』;第6講 ケインズの個人的交友関係;討論

内容 「一般理論」はどのように誕生したのか。ケインズの学問上の盟友R.カーンが、彼のダ

イナミックな思想展開をわかりやすく解説。同時代の諸学説の影響や交友関係を通して、

ケインズ理論の核心に肉薄する入門書。

ISBN等 4-00-027146-6

1973], The General Theory and After : Part 11 Defence and Develo-pment, in CW Vol. 14.

ケインズ全集 第14巻 一般理論とその後―第II部 弁護と発展 単行本 – 2016/1/15

ジョン・メイナード・ケインズ (著), ドナルド・モグリッジ (編集), 清水 啓典 (翻訳), 柿原 和夫 (翻訳), 細谷 圭 (翻訳)

タイトル ケインズ全集 第14巻 一般理論とその後

著者名等 ケインズ/〔著〕 ≪再検索≫

著者名等 中山伊知郎/〔ほか〕編 ≪再検索≫

出版者 東洋経済新報社

出版年 2016.1

大きさ等 22cm 454,198p

注記 The collected writings of John Maynard K

eynes.の翻訳

NDC分類 331.74

件名 経済学‐ケンブリッジ学派 ≪再検索≫

要旨 有効需要の原理、流動性選好利子理論、非自発的失業、資本の限界効率―ケインズ理論の

核心に、ホートリー、ロバートソン、ピグー、ヒックス等からよせられた誤解、疑問や批

判に対し、論文・書簡などで応答した論争の記録。『一般理論』草稿の集注版も収録。

目次 第2部 弁護と発展(一般理論以後);付録 『一般理論』草稿の集注版

内容 有効需要の原理、非自発的失業、資本の限界効率…。ケインズ理論の核心に、ホートリー

、ロバートソン、ピグー、ヒックスなどからよせられた誤解、疑問や批判に対し、論文・

書簡などで応答した論争の記録。

Kalecki, M. [1933a], Proba teori koniunktury (Essay on the Business Cycle Theory),

Warsaw: Institute of Reserch on Business Cycles and Prices, partially reprinted in

Kalecki [1966] and Kalecki [197la]; integrally reprinted in Kalecki [1990]

Kalecki, M. [1933], Proba teorti koniunktury, Warsaw : Institute of Reserch on Business Cycles and Prices.

[1935 a], 'Essai d'une th~0rie du mouvenent cyclique des affaires', Revue d'economie politique. Vol. 2.

[1935 b], 'A Macrodynamic Theory of Business Cycle', Econowetrica, Vol. 3.

[1935 c], 'Istota poprawy koniunkturalnej', Polsha Gospodarcza, no. 43.

[1935 d], 'koniunktura a bilance platniczy', Polska Gospodarcz,~, no. 45.

[1936], 'Pare uwag o teorii Keynesa", Ekonomista, no. 3, in Targetti= Kinda-Hass [1982].

[1937 a], 'A Theory of the Business Cycle', Review of Economic Studies, Vol. 4.

[1937 b], 'The Principle of Increasing Risk', Economica, Vol. 3.

[1954], Theory of Economic Dyleamics, London : Allen & Unwin (~~ph~ -(~}~~~~~ ~~~i~i:~~.c4~~la)~~~~~ ~~~p~~, 195S~F)-[1966], Studies iu the Theory of Business Cycle: 7933-39., Oxford : Blackwell. [197l], Sellected Essays on the Dynamics of the Capitalist Economy., Cambridge : Cambridge Universiy Press (j~~EI ' ~~l~~~ ~~~~~;S;~~:i~;~c)~~ii~3~ ~~J R ~;;~~i~:~z~~~i:, 1984 ~p). Keynes, J. M. [1936], The Ge'eeral Theory of Employment, Interest and Money, in

280

and Social Studies, Vol. 32, No. 3, reprinted in Kalecki [1991].

Kalecki, M. [1962b], "Koniunktura gospodarcza w Stanach Zjednoczonych w okresi

1956-61" (The Economic Situation in the USA, 1956 61), in Kalecki, M., Szkice o

Junkcjonowaniu wspolczesnegi kapitalizmu (Sketches on the Functioning of

Modern Capitalism), Warsaw: Panstwowe Wydawnictwo Naukowe, reprinted in

Kalecki [1991]

Kalecki, M. [1962e], "Observations on the Theory of Growth", Economic Journal, Vol.

72, No. 2, reprinted in Kalecki [1991]

Kalecki, M. [1966], Studies in the Theory of Business Cycle: 1933-39, Oxford: Basi

Blackwell

Kalecki, M. [1967a], "Zagadnienie realizacji u Tugana-Baranowskiego i Rozy Luksem

burg" (The Problem of Effective Demand with Tugan-Baranovsky and Rosa

Luxemburg), Ekonomista, No. 2, reprinted in Kalecki [1971a] and Kalecki [1991].

Kalecki, M. [1967b], “Wietnam przez pryzmat USA" (Vietnam and US Big Business),

Polityka, Vol. 10, No. 3, reprinted in Kalecki [1997]

78, No. 2, reprinted in Kalecki [1971a] and Kalecki [1991].

6, reprinted in Kalecki [1993]

Kalecki, M. [1968], "Trend and Business Cycle Reconsidered", Economic Journal, Vol.

Kalecki, M. [1970], "Theories of Growth in Different Social Systems", Scientia, No. 5

Kalecki, M. [1971a], Selected Essays on the Dynamics of the Capitalist Economy,

Cambridge: Cambridge University Press (浅田統一郎·間宮陽介(訳)「資本主義経

Kalecki, M. [1971b], "The Class Struggle and the Distribution of National Income",

Kalecki, M. [1990], Collected Works of Michal Kalecki, Vol. 1, Capitalism: Business

Kalecki, M. [1991], Collected Works of Michal Kalecki, Vol. 2, Capitalism: Economic

済の動態理論』日本経済評論社, 1984年).

Kyklos, Vol. 24, No. 1, reprinted in Kalecki [197la] and Kalecki [1991].

Cycles and Full Employment, ed. by Osiatynski, J., Oxford: Clarendon Press.

Dynamics, ed. by Osiatynski, J., Oxford: Clarendon Press.

Kalecki, M. [1993]. Collected Works of Michal Kalecki, Vol. 4, Socialism: Economic

Growth and Efficiency of Investment, ed. by Osiatynski, J., Oxford: Clarendon

Press.

Kalecki, M. [1997)], Collected Works of Michal Kalecki, Vol. 7. Studies in Ap

Applied

nomics, 1940-1967: Miscellanea, ed. by Osiatynski, J., Oxford: Clarendon Press

Kalecki, M. and Kowalik, T. [1971], "Osservazioni sulla 'riforma cruciale" (Observa

tions on the 'Crucial Reform), Politica ed Economia, No. 2-3, reprinted in Kalecki

[1991].

鍋島直樹ケインズとカレツキ

Kalecki, M. [1966], Studies in the Theory of Business Cycle: 1933-39, Oxford: Basi

Blackwell.

Kalecki, M. [1971a], Selected Essays on the Dynamics of the Capitalist Economy,

Cambridge: Cambridge University Press (浅田統一郎·間宮陽介(訳)「資本主義経済の動態理論』日本経済評論社, 1984年).

Kalecki, M. [1990], Collected Works of Michal Kalecki, Vol. 1, Capitalism: Business

Cycles and Full Employment, ed. by Osiatynski, J., Oxford: Clarendon Press.

Kalecki, M. [1933a], Proba teori koniunktury (Essay on the Business Cycle Theory),

Warsaw: Institute of Reserch on Business Cycles and Prices, partially reprinted in

Kalecki [1966] and Kalecki [197la]; integrally reprinted in Kalecki [1990]

Kalecki, M. [1966], Studies in the Theory of Business Cycle: 1933-39, Oxford: Basi

Blackwell.

Kalecki, M. [1971a], Selected Essays on the Dynamics of the Capitalist Economy,

Cambridge: Cambridge University Press (浅田統一郎·間宮陽介(訳)「資本主義経済の動態理論』日本経済評論社, 1984年).

Kalecki, M. [1990], Collected Works of Michal Kalecki, Vol. 1, Capitalism: Business

Cycles and Full Employment, ed. by Osiatynski, J., Oxford: Clarendon Press.

Kalecki, M. [1933a], Proba teori koniunktury (Essay on the Business Cycle Theory),

Warsaw: Institute of Reserch on Business Cycles and Prices, partially reprinted in

Kalecki [1966] and Kalecki [197la]; integrally reprinted in Kalecki [1990]

Kalecki, M. [1966], Studies in the Theory of Business Cycle: 1933-39, Oxford: Basil Blackwell.

Kalecki, M. [1971a], Selected Essays on the Dynamics of the Capitalist Economy,

Cambridge: Cambridge University Press (浅田統一郎·間宮陽介(訳)「資本主義経済の動態理論』日本経済評論社, 1984年).

Kalecki, M. [1990], Collected Works of Michal Kalecki, Vol. 1, Capitalism: Business

Cycles and Full Employment, ed. by Osiatynski, J., Oxford: Clarendon Press.

Capitalism, business cycles and full employment / Michał Kalecki ; edited by Jerzy Osiatyński ; translated by Chester Adam Kisiel (Collected works of Michał Kalecki ; v. 1)

図書 Clarendon Press, 1990

記事・論文名

outline of the business cycle theory

著者名

kalecki

巻号、ページ

63~144

備考(その他の指定)

表紙 / 目次 / 奥付 / 文字、写真が不鮮明になることを了承

https://books.google.co.jp/books?id=e-EErFm5CpMC&printsec=copyright&hl=ja#v=onepage&q&f=false

カレツキは、社会主義制度においては「完全雇用は、原価に比して価格を引き下げることを

つうじて維持されるであろう」が、他方、「資本主義制度においては‥‥価格・原価関係は……

維持され、利潤は、産出高と雇用の削減をつうじて、投資プラス資本家の消費と同じ額だけ

低下する。資本主義の弁護論者たちは『価格機構』を資本主義制度の大きな利点とみなして

いるのが通常なのに、価格の柔軟性が社会主義経済の特徴であることが明らかになるのは、

まことに逆説的である。」(2)

https://lh3.googleusercontent.com/-riHhbnGXVzE/WxdXcBgc75I/AAAAAAABccg/oIESQbHEDR0cQ6bnvWXrulZRBp3aveE5gCHMYCw/s640/blogger-image-1853320315.jpg

ブルス『社会主義における政治と経済』における解説

カレツキ:投資の低下が資本主義経済で雇用と国民所得におよばす結果

p=(1+Cc)

利潤 | / 45度

| /

| /

| /

| /

A |_____/____ _ーB p/y 資本主義

| / _ー |

A・|___/__ _ー___|B' (p/y)' 社会主義

| / _ー _- ̄

| / _ー |_- ̄ |

|/_ー_- ̄|_____|______

C' C y 国民所得

[AからA'への投資活動の低下]

p=(I+Cc):利潤は、投資(I)に資本家の消費(Cc)を加えたものに等しい

p/y:国民所得に占める所与の利潤の割合

資本主義(p/y)

社会主義(p/y)'

ふたつの社会体制[注:資本主義(p/y)と社会主義(p/y)']では、「投資性向」の低下[A→A']に

たいする反応のしかたが異なるのである。

一方[資本主義]は、賃金と利潤への所得分配の所与のパターンに産出高と雇用を適応させるという反応のしかたをし、

他方[社会主義]は、産出と雇用の能力水準に所得分配を適応させるという反応のしかたをするのである。

(2)

Determimtion of National Income and Consumption 1971

(邦訳『経済変動の理論』1958,67頁 新訳『資本主義経済の動態理論』1984もある)

3:02 午後 削除

コメントを投稿

<< Home