バーナンキ氏には、積極的なマネー供給論者であるという文脈から、「ヘリコプター・ベン」というあだ名が奉られていたことがあったが、そうしたあだ名の由来には、この都市伝説も含まれているかもしれない。

日銀を含め多くの中央銀行がマネー供給の手段として採用している国債の買い入れは、それがいかに大量のマネーを散布するものでもヘリマネとは言わない。ケチャップは、レストランならぬ中央銀行が持っていても何も得られないし、賞味期限を過ぎれば廃棄するほかはない。だが、国債を金庫に収めておけば利子が得られ、償還期には元本が戻ってくる。だから、ケチャップを買うのはヘリマネでも、国債を買うのはヘリマネではないはずなのである。

◇金庫の中身は突然変わる

でも、いつもそうなのだろうか。金庫の中の国債が、いつのまにか賞味期限切れのケチャップに変わっている、そんなことは起こらないのだろうか。

実はそこが怖いところだ。悪夢のシナリオは、GDP(国内総生産)の2倍にまで膨張した国債発行残高、その借り換え能力に人々が疑いを持ち始めたときに始まる。そのとき人々は、日銀資産の大半、400兆円にも迫っている膨大な量の国債を、ただの不良資産、つまりは「賞味期限の過ぎたケチャップ」と思うようになるかもしれない。そうしたら何が生じるだろうか。

生じるのは、通貨価値のスリップ・ダウン、言い換えれば物価水準のジャンプ・アップ、それへの予感である。日銀が望んでいるような緩やかで持続的なインフレではない。そして、長期金利は突発的な上昇を始めることになる。中央銀行が直接にコントロールできるのは、短期の市場金利であって長期金利、つまり長期債の市場利回りではない。そこに悪夢の基本構造がある。

図1は、日本国債の保有状況を示したものである。財投債を含め1000兆円を超える国債のほとんどは、日銀を含む金融機関や機関投資家などに保有されていることが分かる。長期金利の急上昇は彼らの信用を直撃するだろう。

日本の国債は、1700兆円の家計貯蓄に支えられていると言われることがある。その通りである。だが、家計貯蓄は、直接に国債市場を支えているわけではない。日本国債のほとんどは、期間決算に拘束される法人や組織を通じて保有されているのだ。だから、国債の借り換え能力に対する疑念は、日銀と民間銀行あるいは保険会社などのバランスシート毀損(きそん)を通じて、日本円や日本の金融システムに対する信用への破壊的な衝撃になりかねない。

もちろん、黒田東彦日銀総裁の見事な手綱さばきで、異次元緩和が緩やかに「出口」を迎える可能性だってある。だが、それは保証できることではない。政府債務の基盤は盤石だと説明することと、それを信じてもらえるかどうかは別問題だからである。

危機の可能性を否定できない以上、私たちは備えを怠るべきではない。

◇“永久債”にするのなら

筆者は2016年5月末より、「日経ナウキャスト日次物価指数」の配信サイトである株式会社ナウキャストのホームページを借りて、一つのプランを公開している。

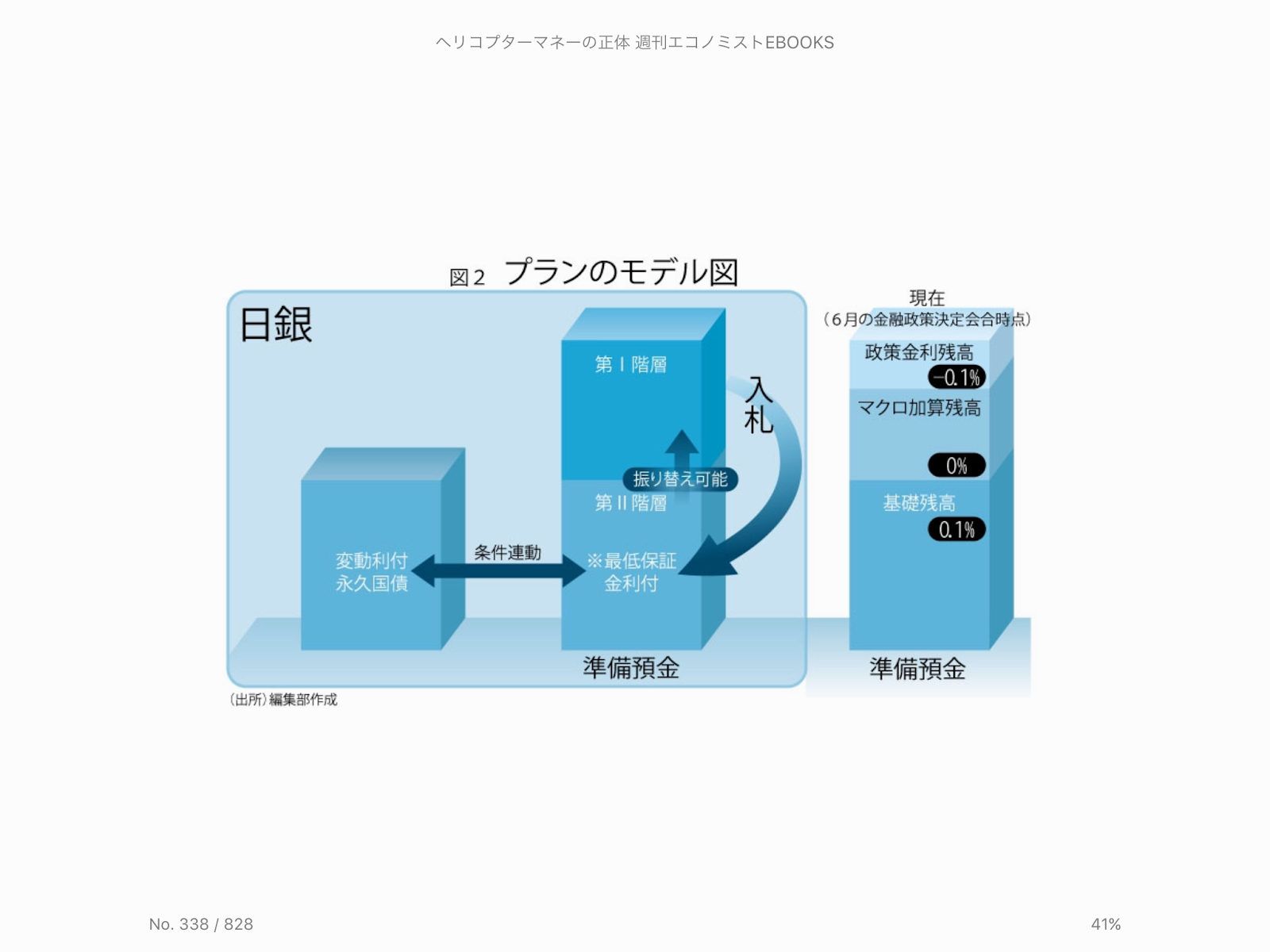

図2に示すように、その骨子は、今や国債発行高の4割にまで達している日銀保有国債を他の国債から切り離し、変動利付永久債に交換すること、そして、そこから生じるキャッシュフローを、少なくとも異次元緩和の終了まで、準備預金保有金融機関へと移転する仕組みを構築しておくところにある。

参考にしたのは、日銀自身が1月のマイナス金利導入の際に採用した仕組みだ。マイナス0・1%の金利が付される一般の準備預金から、過去の積み立て実績に応じた一定金額を基礎残高として区分し、それにプラス0・1%の金利を付すというものである。

筆者のプランでは、分離した準備預金の付利条件を入札で決定することにし、さらに、分離した準備預金を永久債に転換した変動利付国債に見合うものと位置付けてみた。国債を永久債化し変動金利に転換としたのは、政府の借り換え負担を軽減しつつ日銀のバランスシートを守るためである。だが、得られる効果はそれだけでない。

日本あるいは日本国債をみる投資家の「潮目」が変わり、価格の下落(利回りの上昇)が始まったときのことを考えてみよう。もちろん、金利の上昇は、「潮目」の変化だけで起こるとは限らない。アベノミクスが成功し、異次元緩和が「出口」に至ったときにも、これは日銀の誘導に沿って、市場金利はマイナス領域から離れ始めるはずだ。

いずれにしても、そうしたとき、政府は、自身のALM(資産・負債総合管理)的な判断から、この変動利付永久債の償還と借り換えを考え始めるはずである。異次元緩和が終わりを迎え、金利が上昇を始めれば、自身の資金調達を長期化し、再び固定金利化しておいた方が安全なはずだからだ。

もう気付いていただけただろう。こうすれば、この仕組み自体に固定的な終了期をセットしておかなくても、変動金利のメカニズムがその代わりをしてくれるのである。そうしてこれまでの量的緩和の「成果」を切り離して凍結し、足元では日銀が追加的な緩和に動く余地を確保するとともに、事情が変わったときには、散布されたマネーを回収する仕組みを準備すること、それが今回の提案の狙いである。

これまで通りにデフレと戦い続けるのか、それとも戦いの弊害の方に眼を向けるのか、それは英明な黒田総裁が決めることである。プランを永久債ベースで考えたのは、その黒田総裁が「出口」に至るステップを語っていないからである。永久債にしておけば、総裁が異次元緩和の終わりを語り始めるまで、市場は待つことができるわけだ。

日銀総裁が「出口」を語る日は、まだまだ当分は来ないかもしれない。いや、日銀総裁が「出口」を語り始める前に、異次元緩和そのものが、予期せぬ終わりを迎えることになるかもしれない。それは楽しくない予想だが、その予想を無視できない以上、備えが必要なのである。

具体的イメージをつかむために、このプランを実施した場合、量的緩和の「終わり」の前後で何が起こるか、一例を図3に示しておこう。あえて「一例」と断ったのは、そこで何が起こるかは、具体的な制度設計、すなわちスプレッド(上乗せ金利)とフロア条項(最低保証金利)、そして第2階層から第1階層へと準備預金を振り替える際のペナルティーの設定に依存しているからである。ここで示すのは、あり得そうなシナリオの一つに過ぎない。

◇シナリオは設計次第

現行の金利体系からの移行を基本に考えてみよう。その場合、最低保証金利は移行時の基礎残高への付利水準(0・1%)と同じにするのが妥当だろう。また、ペナルティーはゼロでスタートするのが自然と思われる。その場合、スプレッドは多少のマイナスになるはずだ。そう想定する理由は、量的緩和終了前後のシナリオを考えれば分かってくる。

今のマイナス金利の状況が膠着(こうちゃく)し動かない間のことを考えてみよう。その間は、第2階層の金利は最低保証金利にくぎ付けになったままで動きそうもない。スプレッドはマイナスに設定されているが、実際の金利適用に有効なのはフロア条項の方だからだ。

では、状況が変わって第1階層預金の金利がゼロあるいはプラス領域にまで、つまりはフロア条項の意味がなくなるほどまで上がってきたとき、準備預金保有金融機関はどう反応するだろうか。

スプレッドが存在する限り、第2階層に実際に付される金利は第1階層のそれよりも低く、かつフロア条項も無意味になっているわけだが、それは金融機関に新たな不利益をもたらすものではない。彼らは、いつでも第2階層預金を第1階層に振り替えることができるからだ。彼らがそうしないとすれば、それは、いったんは引き上げた準備預金金利を再び日銀が引き下げてくる可能性を読んでいるせいである。

こう整理すれば、入札条件に応じてスプレッドがどうなるかの見当が付く。量的緩和の終わりの前でも後でも、彼らにとって第2階層預金を持つことは、第1階層預金比で必ず有利なのである。したがって、条件を入札で決めれば、スプレッドはマイナスになるはずである。入札でスプレッドがプラスになるとしたら、それは、第2階層から第1階層への振り替えにペナルティーを設定した場合である。ただ、そうした設定は、現状を基準に考える限り、あまり現実性はないように思われる。

ちなみに、このプランでは、量的緩和継続中の国債(変動利付転換された国債)の金利は、もしそれにフロア条項が付されるのなら第2階層の金利と等しく、そうでなければ単純にスプレッドに沿ってもっと低くなる。いずれにせよ、際限なくベースマネーを供給する異次元緩和下では、市場金利は第1階層預金の金利に張りついて動かないので、それに連動する国債金利も事実上の固定となるだろう。このプランによる国債の金利が上昇を始めるのは、日銀が無制限のベースマネー供給を止めたとき、すなわち量的緩和が終わりを迎える局面に至ったときである。

量的緩和が終わりを迎えれば、日銀は、保有国債の対市中売却つまり「売りオペ」を開始することになる。だが、保有国債が固定利付のままだったら、日銀は、オペ対象国債に生じる売却損だけでなく、保有国債全体に対する評価損をも気にしつつ、緩和の終わらせ方を探らねばならない。ところが、もし保有国債が変動利付に転換されていれば、わずかばかりのスプレッドに相当する売却損がオペ対象国債に生じる以外に損失は生じなくなる。それは、「出口」における金融政策運営に、新たな自由度と機動性を与えてくれるはずだ。

言うまでもないことだが、描いた図は、プランの採用で演出できるシナリオの一例に過ぎない。だが、こうして準備をしておけば、金融政策と国債管理政策とが区別ないまでに溶け合ってしまった日本を予期せぬ衝撃が見舞ったときにも、それで市場と政策とが同時に崩壊する事態だけは避けることができよう。

◇緩和依存症への処方箋

異次元緩和は一種の「麻薬」である。麻薬は痛みを和らげてくれるが、使い続けていれば健康を損なう。異次元緩和という処方箋に浸かりきった日本経済も同じようなものだ。そして、薬物依存症の患者を救うのには、それを断ったときへの恐怖から解放する治療が必要なのと同じように、異次元緩和依存症に陥った日本経済にも、やがて来る金利上昇への備えが不可欠なのである。このプランの狙いも、そうした備えについての議論を促すことにある。

とはいえ、ここで提案したプランは、今日明日からでもスタート可能というものではない。プランの根幹にあるのは、日銀保有既発国債と新規発行の変動利付国債とのスワップ(交換取引)だが、それを既発国債の繰り上げ償還と新規国債の引き受けというかたちで行おうとすれば、国会の議決を経ない日銀国債引き受けを禁じている財政法第5条との関係を整理しなければならないし、そうした形式上のことだけでなく、プランの考え方の全体について、それを考えざるを得なくなった背景にまでさかのぼった議論が必要だろうからである。

ただ、現実にリスクがある以上は、打てる手は早く打っておいた方がよい。また、そうして手を打っておけば、日銀保有国債への利払い負担が軽くなるだけでなく(ただし、政府と日銀を連結した「統合政府」でみれば、これは統合政府内の付け替えに過ぎず、本質的な負担軽減ではない)、日銀が国債市場の激変に備えて積み上げている自己資本(*1)の相当部分が不要になり、そこで生じた財政的余裕を、他の活動に振り向けることも可能になるからだ。

16年1月の日銀によるマイナス金利導入は、いかにも評判が良くない。それは当たり前だろう。拙著『中央銀行が終わる日』でも説明したように、停滞の色を濃くする今の世界で求められているのは、銀行券を含むベースマネーの全体にマイナスの金利を付し、デフレ時における金融政策を、ケインズのいう「流動性の罠(*2)」から自由にさせる手法を確立することである。世はマイナス金利なのに、ゼロ金利という利回りが確保され、しかも流動性まで備えた金融資産である銀行券をそのままにして、市場金利だけを強引にマイナス領域に押し下げようとする政策は、金融システムに深刻なゆがみを生じさせることになる。

マイナス金利政策が金融機関経営に及ぼす影響について問われた黒田総裁、そこで「金融政策は金融機関のためにやっていない」と切り返したと報じられたことがあった。ただ、筆者は、それは彼の真意の全部ではないと信じたい。金融政策が金融機関経営のためのものでないことは自明だが、安定した金融システムなくして実効ある金融政策運営ができないことも自明だからである。黒田総裁ほどの知見の持ち主が「社会の利益を増進しようと思い込んでいる場合よりも、自分自身の利益を追求する方が、はるかに有効に社会の利益を増進することがしばしばある」(『国富論』大河内一男監訳・中公文庫より)と説いたアダム・スミスを知らぬはずはあるまい。

危機の足音が聞こえ始めた今、日銀はこれまでにも増して市場の声に注意深く耳を傾ける必要がある。

(岩村充・早稲田大学大学院経営管理研究科教授)

◇日銀の自己資本(*1)

日銀は利益の大半を政府に納めるが、うち5%を自己資本に積み増すよう義務付けられている。資産購入で利益が増す一方、リスクが増しているため、2013年度は20%、14年度は25%を財務大臣の許可を得て自己資本に積み増した。

◇流動性の罠(*2)

名目金利がゼロ以下まで低下すると、金利ゼロの金融資産である銀行券の需要が無限大になるため、貨幣供給量を増やしても金利は下がらなくなる。

◇いわむら・みつる

1950年生まれ。東京大学経済学部卒業。74年日本銀行入行。企画局兼信用機構局参事を経て、98年より早稲田大学ビジネススクール教授。著書に『貨幣進化論』『中央銀行が終わる日』など。

{kind=link}

11 Comments:

おすすめの本の紹介:『ヘリコプターマネーの正体 週刊エコノミストebooks』(週刊エコノミスト編集部 著)

https://www.amazon.co.jp/dp/B01M29G18S/

ヘリコプターマネーは既に現実 予期せぬ“出口”への備えが必要=岩村充

2016/08/02

https://www.weekly-economist.com/2016/08/02/ヘリコプターマネーの正体-予期せぬ-出口-への備えが必要-2016年8月2日号/

「ヘリコプター・マネー」は、米経済学者のミルトン・ フリードマンが、1969年の論文(”TheOptimum Quality of Money”)ch.1のなかで提唱した。

1992年MONEY MISCHIEF 『貨幣の悪戯』(1993・三田出版会)2章で再説。

M.フリードマン著『最適通貨量』単著

昭和45年1月 世界経済 161号(p40~p45) 要約のみ

Milton Friedman;The Optimum Quantity of Money And other Essays. 1969.

国立国会図書館デジタルコレクション - 世界経済 = Journal of world economy. 25(1)(復刊161)

http://dl.ndl.go.jp/info:ndljp/pid/2283602?tocOpened=1

The Optimum Quantity Of Money - Milton Friedman - Google ブックス

https://books.google.co.jp/books?id=DZ9OTS6LbEcC&pg=PA2&hl=ja&source=gbs_toc_r&cad=4#v=onepage&q&f=false

おすすめの本の紹介:『ヘリコプターマネーの正体 週刊エコノミストebooks』(週刊エコノミスト編集部 著)

https://www.amazon.co.jp/dp/B01M29G18S/

ヘリコプターマネーは既に現実 予期せぬ“出口”への備えが必要=岩村充

2016/08/02

https://www.weekly-economist.com/2016/08/02/ヘリコプターマネーの正体-予期せぬ-出口-への備えが必要-2016年8月2日号/

5:35 午後 削除

Blogger yoji さんは書きました...

「ヘリコプター・マネー」は、米経済学者のミルトン・ フリードマンが、1969年の論文(”TheOptimum Quality of Money”最適通貨量)ch.1

のなかで提唱した。

1992年MONEY MISCHIEF 『貨幣の悪戯』(1993・三田出版会)2章で再説。

The Optimum Quantity Of Money - Milton Friedman - Google ブックス

https://books.google.co.jp/books?id=DZ9OTS6LbEcC&pg=PA2&hl=ja&source=gbs_toc_r&cad=4#v=onepage&q&f=false

おすすめの本の紹介:『ヘリコプターマネーの正体 週刊エコノミストebooks』(週刊エコノミスト編集部 著)

https://www.amazon.co.jp/dp/B01M29G18S/

ヘリコプターマネーは既に現実 予期せぬ“出口”への備えが必要=岩村充

2016/08/02

https://www.weekly-economist.com/2016/08/02/ヘリコプターマネーの正体-予期せぬ-出口-への備えが必要-2016年8月2日号/

「ヘリコプター・マネー」は、米経済学者のミルトン・ フリードマンが、1969年の論文(”TheOptimum Quality of Money”最適通貨量)ch.1

のなかで提唱した。

1992年MONEY MISCHIEF 『貨幣の悪戯』(1993・三田出版会)2章で再説。

The Optimum Quantity Of Money - Milton Friedman - Google ブックス

https://books.google.co.jp/books?id=DZ9OTS6LbEcC&pg=PA2&hl=ja&source=gbs_toc_r&cad=4#v=onepage&q&f=false

Not to be confused with People's QE or Basic income.

Helicopter money is a proposed unconventional monetary policy, sometimes suggested as an alternative to quantitative easing (QE) when the economy is in a liquidity trap (when interest rates near zero and the economy remains in recession). Although the original idea of helicopter money describes central banks making payments directly to individuals, economists have used the term 'helicopter money' to refer to a wide range of different policy ideas, including the 'permanent' monetization of budget deficits – with the additional element of attempting to shock beliefs about future inflation or nominal GDP growth, in order to change expectations.[1] A second set of policies, closer to the original description of helicopter money, and more innovative in the context of monetary history, involves the central bank making direct transfers to the private sector financed with base money, without the direct involvement of fiscal authorities.[2][3] This has also been called a citizens' dividend or a distribution of future seigniorage.[4]

The phrase "helicopter money" was first coined by Milton Friedman in 1969, when he wrote a parable of dropping money from a helicopter to illustrate the effects of a monetary expansion. The concept was revived by economists as a monetary policy proposal in the early 2000s following Japan's Lost Decade. In November 2002, Ben Bernanke, then Federal Reserve Board governor, and later chairman, suggested that helicopter money could always be used to prevent deflation.

Contents

Origins

Edit

Although very similar concepts have been previously defended by various people including Major Douglas and the Social Credit Movement, Nobel winning economist Milton Friedman is known to be the one who coined the term 'helicopter money' in the now famous paper "The Optimum Quantity of Money", where he included the following parable:

Let us suppose now that one day a helicopter flies over this community and drops an additional $1,000 in bills from the sky, which is, of course, hastily collected by members of the community. Let us suppose further that everyone is convinced that this is a unique event which will never be repeated.

「ある日、ヘリコプターがこのコミュニティの上を飛んで空から追加の1,000ドルの請求書を落としたとしましょう。もちろん、コミュニティのメンバーによって急いで集められました。 決して繰り返されることのないユニークなイベント。」 (ミルトン・フリードマン、「最適な金額」、1969年)

Let us now complicate our example by supposing that the dropping of money, instead of being a unique, miraculous event, becomes a continuous process, which, perhaps after a lag, becomes fully anticipated by everyone. Money rains down from heaven at a rate which produces a steady increase in the quantity of money, let us say, of 10 per cent per year. The path of the quantity of money is shown in Figure 1, M0 being the initial quantity of money ($ 1,000 in our example), t0 the date at which the money starts to rain from heaven, and μ the rate of growth of the quantity of money (10 per cent per year in our example). Mathematically,

The distribution of the additional nominal balances among individuals does not

matter for our purposes, provided that an individual is not able to affect the amount of additional cash he receives by altering the amount of cash balances he holds. The simplest assumption is that each individual gets a share of the new nominal balances equal to the percentage of nominal balances he initially held, and that this share, once determined, remains constant, whatever his future behavior. The reason for this assumption will become clear. Even with this assumption, there may be distributional effects, by contrast with the once-and-for-all case, if final equilibrium cash balances are distributed differently than initial balances. For the moment, however, we shall neglect any distributional effects. Individuals could respond to this steady monetary downpour as they did to the once-and-for-all doubling of the quantity of money, namely, by keeping real balances unchanged. If they did so, and responded instantaneously and without friction, all real magnitudes could remain unchanged. Prices would behave in precisely the same manner as the nominal money stock. They would rise from their initial level at the rate of 10 per cent per year, as shown in Figure 2. Nominal income, defined as the value of services and excluding the bonanza Fig. 2 from the sky, would behave in the same way; its time path could be represented by the same line. The bonanza, if included, would raise nominal income from

私たちの例を複雑にしてみましょう。ユニークで奇跡的な出来事ではなく、お金の落とし込みが連続的なプロセスになると仮定して、おそらく遅れた後に、誰もが完全に予期するようになります。 お金は、年間10%の、金額の着実な増加を生み出す速度で天から降りてきます。 金額の経路を図1に示します。M0は初期の金額(この例では1,000ドル)、t0は天から雨が降り始める日、およびµの成長率です。 お金(私達の例では年10%)。 数学的には、

個人間の追加の名目残高の分布は、

ただし、個人が自分の保有する現金残高の金額を変更しても、自分が受け取る追加現金の金額に影響を与えることはできません。最も単純な仮定は、各個人が自分が最初に保有していた名目残高の割合に等しい新しい名目残高の割合を取得し、この割合は一度決定されると、将来の行動に関係なく一定のままであるということです。この仮定の理由は明らかになります。この仮定があっても、最終的な均衡現金残高が当初の残高とは異なる方法で分配される場合、一度限りの場合とは対照的に、分配効果があるかもしれません。しかし現時点では、分配効果を無視します。個人は、この実質的な収支を変えないことによって、かつては2倍になる金額の倍増に対応してきたように、この着実な金銭の流れに対応することができました。彼らがそうして、そして即座にそして摩擦なしで反応したならば、すべての本当の大きさは変わらないままでいられるかもしれません。価格は名目マネーストックとまったく同じように振舞います。図2に示すように、彼らは当初の水準から年率10%の割合で上昇します。サービスの価値として定義され、空から図2の大当たりを除いた名目所得も同様に振る舞います。そのタイムパスは同じ行で表すことができます。含まれているならば、大当たりはから名目所得を上げるでしょう

m

p

価格

名目所得

コメントを投稿

<< Home