Do Taxes and Bonds Finance Government Spending? Stephanie Bell 2000

https://nam-students.blogspot.com/2019/05/do-taxes-and-bonds-finance-government.html @https://translate.google.com/translate?sl=en&tl=ja&u=https%3A%2F%2Fnam-students.blogspot.com%2F2019%2F05%2Fdo-taxes-and-bonds-finance-government.html

参考:

FUNCTIONAL FINANCE AND THE FEDERAL DEBT Author(s): ABBA P. LERNER 1943

Bell, Stephanie - Do Taxes and Bonds Finance Government Spending Weston William https://www.scribd.com/book/58324026 |

Do Taxes and Bonds Finance Government Spending?

Author(s): Stephanie Bell

Source: Journal of Economic Issues, Vol. 34, No. 3 (Sep., 2000), pp. 603-620

Published by: Association for Evolutionary Economics

Stable URL: http://www.jstor.org/stable/4227588

Accessed: 16/07/2010 13:01

603:

Do Taxes and Bonds Finance Government Spending?

Stephanie Bell

Debates over the impacts of various ways of financing government deficits and

about the relative impact of monetary and fiscal policy have, unfortunately, been

carried out without recognition of the institutional process by which modem government spending, borrowing, and taxation are accomplished.1 In the United States,

close cooperation between the Treasury, the Federal Reserve System, and depository institutions makes the traditional distinctions between monetary and fiscal policy hard to use in describing actual processes and renders irrelevant many of the

theories about the most appropriate mix of borrowing and taxation. Indeed, the entire treatment of taxation and of government borrowing assumes a monetary system

quite unlike that of the modern U.S. system. My purpose in this paper is to describe, in some detail, the way in which the Treasury and the Federal Reserve coordinate policies that are neither purely fiscal nor purely monetary and to argue that

theories of monetary/fiscal policy should incorporate more discussion of the issues

of reserve management.

The "Reserve Effects" of Taxing and Spending

Before examining the reserve effects of various Treasury operations, it is, perhaps, prudent to begin by looking closely at aggregate member bank reserves.2

____

The author is a Ph.D. candidate at The New School for Social Research and a Lecturer at the

University of Missouri-Kansas City. This paper was wntten while the author was Cambridge University

Visiting Scholar at The Jerome Levy Economics Institute at Bard College and has been presented at the

Post Keynesian Summer Conference in Knoxville, Tennessee, July 1998; the Post Keynesian Graduate

Workshop in Leeds, United Kingdom, 1998; and at the Conference on the Economics of Public Spending

in Sudbury, Ontario, 1999. Financial support from the Center for Full Employment and Price Stability is

grateftly acknowledged. Helpful comments from Victoria Chick, John F. Henry, Peter Ho, Anne

Mayhew, Edward Nell, Alain Parguez, James Tobin, Randy Wray, and twao anonymous referees greatly

improved the arguments made in this paper.

604:

Beginning with the Federal Reserve's balance sheet, equivalent terms can be added to

each side, and the entries can be manipulated algebraically in order to isolate member bank reserves.3 The result, often referred to as the "reserve equation," depicts

total member bank reserves as the difference between alternative sources and uses

of reserve funds. The reserve equation can be written as seen in Figure 1.

From Figure 1, it is clear that an increase in any of the bracketed terms on the

left will increase reserves, while an increase in any of the bracketed terms on the

right will reduce them.

The author is a Ph.D. candidate at The New School for Social Research and a Lecturer at the

University of Missouri-Kansas City. This paper was wntten while the author was Cambridge University

Visiting Scholar at The Jerome Levy Economics Institute at Bard College and has been presented at the

Post Keynesian Summer Conference in Knoxville, Tennessee, July 1998; the Post Keynesian Graduate

Workshop in Leeds, United Kingdom, 1998; and at the Conference on the Economics of Public Spending

in Sudbury, Ontario, 1999. Financial support from the Center for Full Employment and Price Stability is

grateftly acknowledged. Helpful comments from Victoria Chick, John F. Henry, Peter Ho, Anne

Mayhew, Edward Nell, Alain Parguez, James Tobin, Randy Wray, and twao anonymous referees greatly

improved the arguments made in this paper.

604:

Beginning with the Federal Reserve's balance sheet, equivalent terms can be added to

each side, and the entries can be manipulated algebraically in order to isolate member bank reserves.3 The result, often referred to as the "reserve equation," depicts

total member bank reserves as the difference between alternative sources and uses

of reserve funds. The reserve equation can be written as seen in Figure 1.

From Figure 1, it is clear that an increase in any of the bracketed terms on the

left will increase reserves, while an increase in any of the bracketed terms on the

right will reduce them.

"Reserve Effects" of Taxing and Spending

In this section, the reserve effects of two important Treasury operations-gov-

ernment spending and taxing-will be analyzed. To emphasize the impact of these

operations on bank reserves, the case in which all government payments and re-

ceipts are immediately credited/debited to accounts held at Reserve banks will be

considered.[4 ]

When the government spends, it writes a check on its account at the Federal Re-

serve. If, for example, a Social Security check is deposited into an account at a

commercial bank, member bank reserves rise (by the amount of the check) as the

Federal Reserve debits the Treasury's account, decreasing the right-hand bracket in

Figure 1, and credits the account of a commercial bank.

Figure 1. The Reserve Equation

Sources Uses

Federal Reserve Credit: Currency in Circulation

U.S. Gov't Securities +

Loans to Member Banks U.S. Treasury Balance at

Fed

Total Float +

Member Bank = + Foreign Balances at Fed

Reserves Gold +

+ Treasury Cash

SDR Certificates +

+ Other Fed Deposits and

Treasury Currency accounts (net)

税金は公的支出に充てられますか?

605:

Thus, a system-wide increase in member bank reserves results whenever a check drawn on a Treasury

account at a Federal Reserve bank is deposited with a commercial bank. Government

spending, then, increases aggregate bank reserves (ceteris paribus).

When, instead of drawing on its account at the Fed, the Treasury receives funds

into this account, the reverse is true. For example, if a taxpayer pays his/her taxes

by sending a check to the Internal Revenue Service (IRS), his/her bank and the

banking system as a whole, lose an equivalent amount of reserves, as the IRS depos-

its the check into the Treasury's account at the Federal Reserve. Total member bank

reserves decline as the right-hand bracket in Figure 1 increases. Thus, the payment

of taxes by check results in a system-wide decrease in member bank reserves (ce-

teris paribus).[5 ]

If Treasury spending out of its accounts at Federal Reserve banks were perfectly

coordinated with tax receipts deposited directly into the Treasury's accounts at Re-

serve banks, their opposing effects on reserves would offset one another. That is, if

the government ran a balanced budget with daily tax receipts and government spend-

ing timed to offset one another, there would be no net effect on bank reserves.

However, as Figure 2 shows, the Treasury's daily receipts and disbursements from

accounts at Reserve banks can be highly incommensurate. Indeed, during this short

sample period, Figure 2 shows that they can differ by almost $6 billion. This is sub-

stantial, given that total member bank reserves average only about $50 billion

[Meulendyke 1998, 145]. Thus, a one-day decline in total reserves-to $44 bil-

lion-amounts to a 12 percent decrease in member bank reserves. Such a sharp de-

cline is likely to result in an immediate bidding up of the federal funds rate.

Thus, despite an attenuation of the reserve effect due to the simultaneous injec-

tion and withdrawal of reserves, government spending and taxation will never per-

fectly offset one another. Moreover, even if a more even pattern could be

established, some discrepancies would persist because, as Irving Auerbach [1963,

349] recognized, "there is no way to determine in advance, with complete accuracy,

the total amount of the receipts or the speed at which the revenue collectors will be able to process the returns."

Figure 2. Daily Flows into/from Federal Reserve Accounts, March 1998 (Net

of Transfers to/from T&L Accounts and Debt Management)

@1

c

0

-1000.0

L 000 L---Series2 K

1~ ~ ~~~~~... .ExpendituresSeii

4000 ~eceipts .. eis

u- 2000-

0 0

0 3/5 3/9 3/10 3/11 3/13 3/16 3/17 3/18 3/19 3/20 3/23 3/25 3/26 3/27 3/30

Source: Daily Treasury Statement, http://fedbbs.access.gop.gov/dailys.htm

著者:ステファニーベル

出典:Journal of Economic Issues、Vol。 34、No.3(2000年9月)、603〜620頁。

出版社:進化経済学協会

安定したURL:http://www.jstor.org/stable/4227588

アクセス:16/07/2010 13:01

603:

税金は公的支出に充てられますか?

ステファニーベル

政府の財政赤字への資金調達のさまざまな方法の影響に関する議論

残念ながら、金融政策と財政政策の相対的な影響について

現代の政府支出、借入、および課税が達成される制度的プロセスを認識せずに実施されている1。

財務省、連邦準備制度、および預金機関の間の緊密な協力は、実際のプロセスを記述する際に金融政策と財政政策の間の伝統的な区別を使用することを困難にし、無関係な多くの

借入と課税の最も適切な組み合わせに関する理論。確かに、課税と政府の借り入れの全体的な扱いは、通貨システムを想定しています

現代のアメリカのシステムとは全く違っています。本稿での私の目的は、財務省と連邦準備制度理事会が純粋に財政的でも純粋に金銭的でもない政策を調整する方法をある程度詳細に説明し、それを主張することです。

金融/財政政策の理論には、これらの問題についてのさらなる議論を盛り込むべきである。

リザーブ管理

課税と支出の「準備効果」

さまざまな財務業務の準備金効果を検討する前に、おそらく、加盟銀行の総準備金を注意深く検討することから始めるのが賢明です。

____

著者は博士です。社会研究のための新しい学校との講師

ミズーリ大学カンザスシティ校。著者がケンブリッジ大学の間、この論文は執筆されました

Bard CollegeのJerome Levy Economics Instituteで客員研究員を務めました。

1998年7月にテネシー州ノックスビルで開催されたポストケインジアンサマーカンファレンス。ポストケインジアン大学院

1998年イギリス、リーズでのワークショップ。と公共支出の経済学会議で

1999年、オンタリオ州サドベリーで開催されました。

感謝して認めた。 Victoria Chick、John F. Henry、Peter Ho、Anneからの有益なコメント

Mayhew、Edward Nell、Alain Parguez、James Tobin、Randy Wray、そしてtwaoの匿名審判

このペーパーで行われた議論を改善しました。

604:

連邦準備制度の貸借対照表から始めて、同等の用語を追加することができます。

加盟銀行の準備金を分離するために、エントリを代数的に操作することができます。

代替の出所と用途の違いとしての全会員銀行の準備金

準備金の。予備方程式は図1のように書くことができます。

図1から、括弧で囲まれた用語のいずれかが増加していることは明らかです。

残りの金額は準備金を増やしますが、

権利はそれらを減らすでしょう。

課税と支出の「準備効果」

このセクションでは、2つの重要な財務業務の準備金効果 - 政府 -

政府支出と課税 - 分析されます。これらの影響を強調する

銀行の準備金の運用、政府のすべての支払いと

貯蓄銀行で保有されている口座への入金/引き落としは直ちに行われます。

検討された。[4]

政府が支出するとき、それは連邦政府でその口座に小切手を書く。

仕える。たとえば、社会保障小切手がの口座に入金されたとします。

商業銀行、加盟銀行の準備金が(小切手の金額分)増加すると、

連邦準備制度理事会は、財務省の口座から借方に記入して、国庫の右括弧を減らします。

図1、および商業銀行の口座に入金します。

図1.リザーブ方程式

ソース使用

連邦準備制度のクレジット:循環通貨

米国政府の証券+

メンバーバンクへの融資

連邦機関

総フロート+

加盟銀行= + FRBの対外収支

ゴールド+

+財務省現金

SDR証明書+

+その他のFRB預金と

財務通貨勘定(純額)

605:

Thus, a system-wide increase in member bank reserves results whenever a check drawn on a Treasury

account at a Federal Reserve bank is deposited with a commercial bank. Government

spending, then, increases aggregate bank reserves (ceteris paribus).

When, instead of drawing on its account at the Fed, the Treasury receives funds

into this account, the reverse is true. For example, if a taxpayer pays his/her taxes

by sending a check to the Internal Revenue Service (IRS), his/her bank and the

banking system as a whole, lose an equivalent amount of reserves, as the IRS depos-

its the check into the Treasury's account at the Federal Reserve. Total member bank

reserves decline as the right-hand bracket in Figure 1 increases. Thus, the payment

of taxes by check results in a system-wide decrease in member bank reserves (ce-

teris paribus).[5 ]

If Treasury spending out of its accounts at Federal Reserve banks were perfectly

coordinated with tax receipts deposited directly into the Treasury's accounts at Re-

serve banks, their opposing effects on reserves would offset one another. That is, if

the government ran a balanced budget with daily tax receipts and government spend-

ing timed to offset one another, there would be no net effect on bank reserves.

However, as Figure 2 shows, the Treasury's daily receipts and disbursements from

accounts at Reserve banks can be highly incommensurate. Indeed, during this short

sample period, Figure 2 shows that they can differ by almost $6 billion. This is sub-

stantial, given that total member bank reserves average only about $50 billion

[Meulendyke 1998, 145]. Thus, a one-day decline in total reserves-to $44 bil-

lion-amounts to a 12 percent decrease in member bank reserves. Such a sharp de-

cline is likely to result in an immediate bidding up of the federal funds rate.

Thus, despite an attenuation of the reserve effect due to the simultaneous injec-

tion and withdrawal of reserves, government spending and taxation will never per-

fectly offset one another. Moreover, even if a more even pattern could be

established, some discrepancies would persist because, as Irving Auerbach [1963,

349] recognized, "there is no way to determine in advance, with complete accuracy,

the total amount of the receipts or the speed at which the revenue collectors will be able to process the returns."

605:

このように、システム全体で加盟銀行の準備金が増加すると、いつでも財務省の小切手が引き出されます。

連邦準備銀行の口座は、商業銀行に預けられます。政府

支出は、その後、銀行の総準備金(ceteris paribus)を増加させます。

連邦準備制度理事会の口座から引き出すのではなく、財務省が資金を受け取るとき

このアカウントに、その逆が当てはまります。たとえば、納税者が自分の税金を支払う場合

内国歳入庁(IRS)、その銀行、および銀行に小切手を送付する。

銀行システム全体としては、IRSの預金として、同額の準備金を失う。

それは連邦準備制度理事会の財務省の口座への小切手です。総会員銀行

図1の右括弧が大きくなるにつれて、準備金は減少します。したがって、支払い

小切手による税金の徴収により、システム全体で加盟銀行の準備金が減少します。

teris paribus)[5]

連邦準備銀行の口座からの財務省の支出が完全に

当局の財務省の口座に直接預け入れられている納税領収書と調整する。

銀行にサービスを提供するならば、準備金への反対の影響は互いに相殺するでしょう。つまり、

政府は日々の納税と政府支出でバランスの取れた予算を実行しました。

互いを相殺するようにタイミングを合わせても、銀行の準備金に正味の影響はありません。

ただし、図2に示すように、財務省の1日の受領額と支出額は

準備銀行の口座は非常に矛盾している可能性があります。確かに、この短い間に

サンプル期間、図2は、それらがほぼ60億ドル異なる可能性があることを示しています。これはサブです

加盟銀行の準備金総額は平均約500億ドルにすぎないことを考えると

[Meulendyke 1998、145]。したがって、総準備金の1日の減少 - 44億ドル -

会員銀行の準備金が12%減少しました。そのような鋭いデ

clineは連邦資金のレートの即時の値上げをもたらす可能性があります。

このように、同時注入による予備効果の減衰にもかかわらず

準備金の引下げ、政府支出および課税は決して許されません。

互いに完全にオフセットします。さらに、より均一なパターンが可能であったとしても

Irving Auerbach [1963、

349]、「完全な正確さで事前に決定する方法はない。

領収書の総額、または収益収集者が返品を処理できる速度。」

of Transfers to/from T&L Accounts and Debt Management)

@1

c

0

-1000.0

L 000 L---Series2 K

1~ ~ ~~~~~... .ExpendituresSeii

4000 ~eceipts .. eis

u- 2000-

0 0

0 3/5 3/9 3/10 3/11 3/13 3/16 3/17 3/18 3/19 3/20 3/23 3/25 3/26 3/27 3/30

Source: Daily Treasury Statement, http://fedbbs.access.gop.gov/dailys.htm

図2. 1998年3月の連邦準備銀行口座への、またはそれからの1日のフロー(純額)

T&L勘定および債務管理への/からの振替の例)

@ 1

c

0

-1000.0

L 000 L ---シリーズ2 K

1〜〜~~~~~ ... .ExpendituresSeii

4000〜eceipts .. eis

u- 2000-

0 0

0 3/5 3/9 3/10 3/11 3/13 3/16 3/17 3/18 3/19 3/20 3/23 3/25 3/26 3/27 3/30

出典:毎日の財務諸表、http://fedbbs.access.gop.gov/dailys.htm

606:

Thus, while concurrent government spending and taxation have some offsetting impact on reserves, the reserve effect from the Treasury's

daily cash operations would still be substantial, especially "if they were channeled

immediately through the Treasurer's balance at the Reserve Banks" [Auerbach

1963, 333].

The Importance of the "Reserve Effect"

The inability to perfectly coordinate Treasury receipts and expenditures has serious implications for the level of bank reserves and, subsequently, the money market. Because banks are required by law to hold reserves against some fraction of

their deposits, but earn no interest on reserves held in excess of this amount, they

will normally prefer not to hold substantial excess reserves. Government spending,

then, will leave them with more reserves than they will prefer/need to hold, while

the clearing of tax payments will leave them with fewer reserves than are desired/required (ceteris paribus). The fed funds market is the "market of first resort"

for banks wishing to rid themselves of excess reserves or to acquire reserves needed

to meet deficiencies [Poole 1987, 10]. When there is a build-up of reserves within

the system, many banks will attempt to lend reserves in the federal funds market.

The problem, of course, is that lending reserves in the funds market cannot help a

banking system, which began with an "equilibrium" level of reserves, to rid itself of

excess reserves. Moreover, when the system is flush with excess reserves, banks

will find that there are no bidders for these funds, and the federal funds rate may

fall to a zero percent bid.

Likewise, the clearing of tax payments will leave a banking system that began

with an "equilibrium" level of reserves short of required (and/or desired) reserves.

Banks will look to the funds market to acquire needed reserves, but since all banks

cannot return to an "equilibrium" reserve position by borrowing federal funds, a

system-wide shortage will persist. That is, like a system-wide surplus, a system-

wide deficiency cannot be alleviated through the funds market; attempts to do so

will simply drive the funds rate higher and higher.6

Importantly, the funds rate is not the only interest rate affected by changes in the

level of bank reserves. As the "focus of monetary policy, " the funds rate is the "anchor for all other interest rates" [Poole 1987, 11]. Thus, when banks are content

with their reserve positions, Treasury operations (such as government spending and

taxation) disrupt these positions by adding or draining reserves, and banks react to

these changes by first turning to the funds market. There, the funds rate is bid up or

down, and other short-term interest rates are affected. Although some individual

banks will be successful in eliminating their own reserve deficiencies/excesses, the

banking system as a whole will not be able to alleviate a shortage/deficiency on its

own.

606:

したがって、同時の政府支出と課税が準備金にいくらか相殺する影響を与える一方で、財務省からの準備金の影響

日々の現金取引はなおも相当なものとなるでしょう。

すぐに準備銀行での会計のバランスを通して "[Auerbach

1963年、333]。

「予備効果」の重要性

財務省の収入と支出を完全に調整できないことは、銀行の準備金の水準、ひいてはマネーマーケットに深刻な影響を及ぼします。銀行は法律の一部の一部に対して準備金を保有するように義務付けられているため

彼らの預金が、この金額を超えて保有されている準備金に利子を得ていない、彼らは

通常、かなりの過剰準備金を保有しないことを好むでしょう。政府支出、

それから、彼らが彼らが保持することを好む/必要とするより多くの準備金で彼らを残します

納税の清算は、望まれる/要求されるよりも少ない準備金で彼らを残すでしょう(ceteris paribus)。フィードファンド市場は「ファーストリゾートの市場」です。

余分な準備金を取り払うか、必要な準備金を取得したい銀行にとって

欠乏を満たすために[Poole 1987、10]。内に積立金の積み上げがあるとき

このシステムでは、多くの銀行が連邦資金市場で準備金を貸し出そうとします。

問題は、もちろん、ファンド市場での準備金の貸付けは、資金調達の助けにはなれないということです。

「均衡」レベルの準備金で始まった銀行システムは、

余剰準備金。さらに、システムが過剰準備金と同じレベルになると、銀行は

これらの資金に入札者がいないことがわかります。

ゼロパーセント入札に落ちます。

同様に、納税の清算は始まった銀行システムを残すでしょう

「均衡」レベルの準備金が必要(および/または希望)準備金に満たない。

銀行は必要な準備金を獲得するためにファンド市場に目を向けますが、

連邦資金を借りて「均衡のとれた」準備金のポジションに戻ることはできません。

システム全体の不足は解決しません。つまり、システム全体の黒字、システム全体の黒字のように

ファンド市場を通じて大幅な不足を軽減することはできません。試みる

単にファンドレートをどんどん高くしていくでしょう6。

重要なことに、ファンドレートは、金利の変動によって影響を受ける唯一の金利ではありません。

銀行準備のレベル。 「金融政策の焦点」として、ファンドレートは「他のすべての金利のアンカー」です[Poole 1987、11]。したがって、銀行が満足しているとき

彼らの留保ポジション、財務業務(政府支出、

(課税)は、準備金を追加するか、または排出することによってこれらのポジションを混乱させます。

これらは、最初にファンド市場に目を向けることによって変化します。そこでは、資金レートは値上がりしているか

そして、他の短期金利が影響を受けます。一部の個人

銀行は、自らの準備金不足/超過を解消することに成功するでしょう。

銀行システム全体としては、金融システムの不足/不足を緩和することはできません。

自分の。

607:

Only through government adding/draining of reserves can a system-wide imbalance be eliminated. Because attempts to resolve system-wide reserve "disequilibrium" through the funds market can affect a number of other interest rates, a variety of procedures has been developed to mitigate the adverse impact of Treasury

operations on banks' reserve positions.

Strategies for Reducing the Reserve Effect

In the preceding discussion, the effects of government spending and taxing on

bank reserves were examined by assuming that all disbursements and receipts were

immediately credited/debited to the Treasury's accounts at Federal Reserve banks.

This treatment allowed us to highlight the impact of each of these operations on the

level of bank reserves, but it did not paint a realistic picture of the way things currently work. If things did indeed work this way, there would be an unrelenting disruption of banks' reserve positions and, subsequently, chronic turmoil in the funds

market. Because these consequences are highly undesirable from a policy perspective, some important strategies have been developed to mitigate these persistent, yet

unpredictable, reserve effects.

The Use of Tax and Loan Accounts

The disruptive nature of the Treasury's operations was recognized under the Independent Treasury System7 and ultimately led to the use of General and Special

Depositories,8 which are private banks in which government funds could be kept.

This was the first important strategy developed to mitigate the reserve effect. As

John Ranlett recognized, the reserve effect caused by the "point inflow-continuous

outflow nature of Treasury activities" could be tempered by placing certain government receipts into tax and loan accounts at private depositories [1977, 226]. Thus,

the reserve drain that would otherwise accompany payments made to the government could be temporarily prevented.9 The benefits of using these depositories were

quickly recognized, and their functions were broadened when it became clear that

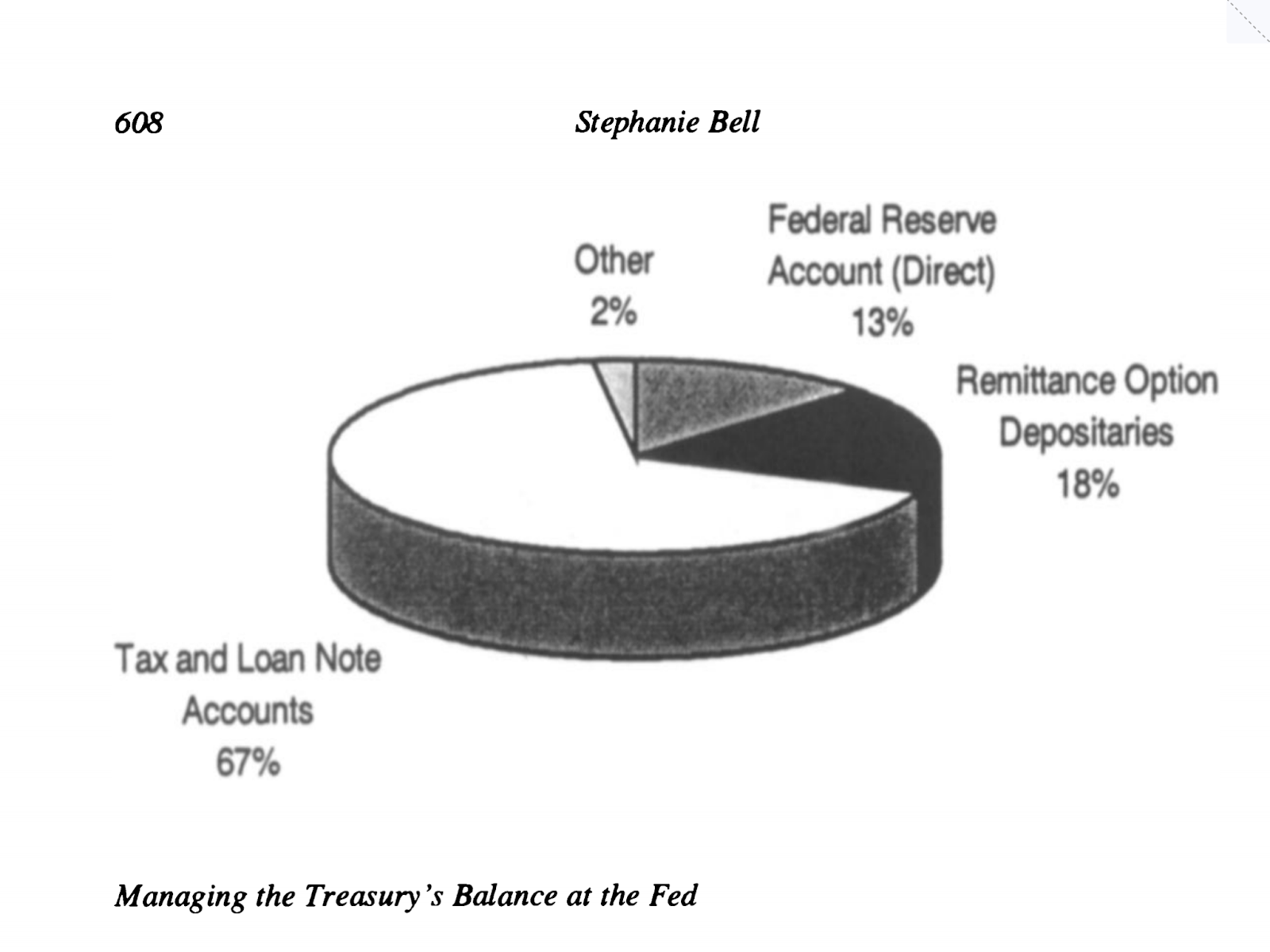

they could be used to further mitigate the reserve effect. As the size of the government's fiscal operations grew, Special Depositories quickly became the most important group of bank depositories [Auerbach 1963]. As Figure 3 shows, just over

two-thirds of all Federal tax receipts are currently deposited directly into tax and

loan accounts.

Today, the tax and loan accounts are by far the most important devices used to

guard the money market against the sizable daily differences (shown in Figure 2)

between the flows of government receipts and disbursements.

607:

608:

Managing the Treasury's Balance at the Fed

政府による埋蔵量の追加/流出によってのみ、システム全体の不均衡を解消することができます。ファンド市場を通じてシステム全体の準備金の「不均衡」を解決しようとする試みは他の多くの金利に影響を与える可能性があるため、財務省の悪影響を軽減するためにさまざまな手順が開発されています

銀行の準備ポジションに対する操作。

準備効果を減らすための戦略

これまでの議論で、政府支出と課税が

銀行の準備金は、すべての支出と領収書が

すぐに連邦準備銀行の財務省の口座に貸方記入/借方記入します。

この処理により、これらの各操作がシステムに及ぼす影響を明確にすることができました。

銀行の準備のレベル、しかしそれは物事が現在働く方法の現実的な絵を描きませんでした。物事が本当にこのように機能した場合、銀行の準備ポジションの容赦ない混乱、そしてその後の資金の慢性的な混乱があるでしょう

市場。これらの結果は政策の観点からは非常に望ましくないので、これらの持続的な、まだ緩和するためにいくつかの重要な戦略が開発されました

予測不可能な予備効果。

税金およびローン口座の使用

財務の業務の破壊的な性質は、独立財務システム7の下で認識され、最終的には一般会計および特別会計の使用につながりました。

預金、8は政府の資金を保管できる民間銀行です。

これは、準備金効果を軽減するために開発された最初の重要な戦略です。として

John Ranlett氏が認識した、「点流入連続による引当金効果」

「国庫業務の流出性」は、特定の政府の領収書を民間の預金所の税金口座およびローン口座に入れることによって和らげることができる[1977、226]。

そうでなければ政府への支払いに伴うであろう準備金の流出は一時的に防ぐことができた。9これらの貯蔵庫を使うことの利点は

すぐに認識され、その機能が明らかになったときにその機能が拡張されました。

それらは準備金効果をさらに緩和するために使用することができます。政府の財政運営の規模が大きくなるにつれて、特別寄託機関はすぐに銀行の寄託機関の最も重要なグループとなりました[Auerbach 1963]。図3に示すように、

現在、連邦の全領収書の3分の2が直接税金に振り込まれています。

ローン口座

今日では、税金とローンの勘定科目がはるかに重要な手段として使用されています。

日々の大きな違いからマネーマーケットを守る(図2参照)。

政府の収入と支出の流れの間。

608:

Managing the Treasury's Balance at the Fed

Since almost all government spending involves writing checks on accounts at the

Fed, virtually all funds in tax and loan accounts must eventually be transferred to

Reserve banks. 10 Because only net changes in the Treasury's account at the Fed im-

pact the aggregate level of reserves (ceteris paribus), maintaining "the Treasurer's

balance with the Reserve Banks at a reasonably constant level" is the second strat-

egy used to minimize the reserve effect of the Treasury's operations [Auerbach

1963, 364]. Specifically, the Treasury "aims to maintain a closing balance of $5 billion in its Federal Reserve checking accounts each day" [Manypenny et al. 1992,

728]. The trend line fitted to the data in Figure 4 shows how successful the Treasury is in its endeavor to maintain this target closing balance. With the exception of

mid-January, one of the major (quarterly) tax dates, and mid-November and mid-

March, when a variety of taxes are withheld from businesses, the closing balance

fluctuates only moderately around the $5 billion target level.

Recall that the government receives funds into its accounts at the 12 Reserve

banks as well as thousands of commercial banks each day, but that nearly all government spending is done by writing checks on accounts at Reserve banks. Maintaining a closing balance of $5 billion at Reserve banks, then, usually requires

transferring the appropriate amount from tax and loan accounts to the Treasury's account at the Fed. For example, if the Treasury expected to receive $5 billion directly into accounts at Reserve banks (today) and expected $6 billion in previously

issued checks to be presented for payment (today), $1 billion would need to be

net change in the level of reserves.

FRBにおける財務省のバランス管理

ほとんどすべての政府支出が口座に小切手を書くことを含むので

連邦機関、税金とローン口座のほとんどすべての資金は、最終的にに転送されなければなりません

銀行を予約する。 10 FRBによる財務省の口座の純変動のみ

「会計の維持」を維持しながら、積立金の合計レベル(ceteris paribus)を定める

合理的に一定の水準で準備銀行とのバランスをとることが

財務省の運用による準備金の影響を最小限に抑えるために使用されていたエギ[Auerbach

1963年、364頁]。具体的には、財務省は、「連邦準備銀行の当座預金口座で毎日50億ドルの決算残高を維持することを目指している」[Manypenny et al。 1992年

728]。図4のデータに適合するトレンドラインは、財務省がこの目標決算残高を維持するためにどの程度成功しているかを示しています。を除いて

1月中旬、主要な(四半期ごとの)納税日の1つ、および11月中旬から中旬

3月、企業からさまざまな税が差し引かれると、期末残高は

目標水準の50億ドル前後では、ほんのわずかしか変動しません。

政府は12準備金でその口座に資金を受け取ることを思い出してください

銀行だけでなく、毎日何千もの商業銀行がありますが、ほとんどすべての政府支出は準備銀行の口座に小切手を書くことによって行われています。そのため、準備銀行で50億ドルの決算残高を維持するには、通常、

税金およびローン口座からFRBの財務省口座へ適切な金額を振替える。たとえば、財務省が準備銀行で直接口座に50億ドルを受け取ると予想していた場合(今日)、それ以前に60億ドルを予想した場合

支払いのために提示される小切手が発行された場合(今日)、10億ドルを支払う必要があります。

ないようにFRB(本日)の財務省の口座に転送されます

準備金のレベルの純変動。

609:

Figure 4. Daily Closing Balance in Treasury's Account at the Federal Reserve

(November 1997-March 1998)

? 20,000-

5 A~

Q ~ ~ ~ ~ ~ ~~~~~~~1 ,,cv

10,000 v W' ___1\0%. .d _7- -

0 o w N O t C D a c

Source: Daily Treasury Statement, http://fedbbs.access.gop.gov/dailys.htm

The Treasury transfers funds to cover anticipated shortfalls by making a "call"

on tax and loan accounts. In most cases, advance notice is given before transferring

funds from these accounts.11 A "reverse-call" or "direct investment" is also possible. This would be necessary if the Treasuqr's closing balance at Reserve banks was

expected to substantially exceed $5 billion. To avoid the reserve drain that would

result from an excessive closing balance, the Treasury may place some or all of the

excessive funds into tax and loan accounts at Special Depositories (a.k.a. note-option banks). Whether "calling" funds fom tax and loan accounts to make up for an

expected shortfall or transferring funds to tax and loan accounts through direct investment (or canceling previous calls) to prevent an excessive closing balance, the

amounts transferred are intended to maintain the Treasury's balance at Reserve

banks as steady as possible. In pursuit of this goal, the Treasury relies on the cooperation of the Federal Reserve.

Coordination with the Federal Reserve

The Federal Reserve is extremely interested in helping the Treasury achieve its

target closing balance, because the Treasury's balance at the Fed "is the reserve factor

that shows the most variation from one reserve maintenance period to another"

[Meulendyke 1998, 156].

610:

Indeed, the Fed's ability to successfully conduct monetary policy (specifically, to hit its target funds rate) depends, to a large extent, on the

Treasury's ability to hit its target closing balance. Daily contact between the Treasury and the Fed provide the Treasury with "numerous occasions . . . to assist the

Reserve authorities to achieve a desired objective" [Auerbach 1963, 328].

Unfortunately, the Treasury is unable, even with the cooperation of the Federal

Reserve, to completely offset the effects of its daily spending using tax and loan

calls and direct investment. Indeed, as Table 1 shows, the Treasury's average

monthly closing balance can differ substantially from its $5 billion target.

This, again, is the result of the inherent uncertainty regarding the size/timing of

receipts and expenditures. While it is easy to see how this uncertainty would prevent

daily inflows and outflows from offsetting one another, Table 1 shows that even on

an average monthly basis, the Treasury's balance can close as much as 31 percent

above its target level. Thus, as Figure 5 confirms, one expects a non-zero change in

the Treasury's daily closing balance. Despite this, changes in the daily closing balance do tend to fluctuate fairly closely around zero, deviating most drastically with

quarterly tax payments (January, April, June, and September) and with the collection of withheld business taxes.

Table 1. (Give this a short, descriptive title)

Month Average Closing Balance ($ Millions)

November 1997 5,015

December 1997 5,371

January 1998 6,563

February 1998 5,118

March 1998 5,763

Five-Month Average 5,618

Source: Daily Treasury Statement, http://fedbbs.access.gop.gov/dailys.htm

Figure 5. Change in Daily Closing Balance (November 1997-March 1998)

10,000

= 8,000

> 6,000

4,000

2,000

O__ 0A A-

-2,000

~)-4,000

Z -6,000

. -8,000 05 ' O C LO 0 t ( DC CY

Source: Daily Treasury Statement, http://fedbb.acsgop.n co

Source: Daily Treasury Statement, http://fedbbs.access.gop.gov/dailys.htm

図4連邦準備制度理事会での財務省口座の日次決算残高

(1997年11月〜1998年3月)

? 20,000-

5 A〜

Q〜〜〜〜〜~~~~~~~ 1 ,, cv

10,000 v W '___ 1 \ 0%。 .d _7- -

0は、ありません

出典:毎日の財務諸表、http://fedbbs.access.gop.gov/dailys.htm

財務省は、「電話」をかけることによって予想される不足分を補うために資金を振り込みます。

税金とローンの口座に。ほとんどの場合、振替前に事前通知が行われます

これらの口座からの資金11。「リバースコール」または「直接投資」も可能です。これは、Treasuqrの準備銀行の期末残高が

実質50億ドルを超える見込みです。予備排水を避けるために

過度の決算残高の結果として、財務省は、一部または全部を

特別寄託機関(別名銀行)の税金およびローン口座への過剰な資金。 「呼び出し」ファンドが税金およびローン口座を補填するかどうか

過剰な決算残高を防ぐために、直接投資を通じて(または以前の電話をキャンセルすることによって)予想される不足分または資金を税金およびローン口座に振り込む。

振替金額は、準備金での財務省の残高を維持するためのものです。

銀行はできるだけ安定しています。この目標を達成するために、財務省は連邦準備制度理事会の協力に頼っています。

連邦準備制度との調整

連邦準備制度は、財務省がその達成を支援することに非常に関心があります。

「連邦準備制度理事会における財務省の残高」が準備要素であるため、目標決算残高

それはある予備保全期間から他のものへの最も変動を示します

[Meulendyke 1998、156]。

610:

実際、連邦政府が金融政策を成功させる(具体的には目標ファンドレートを達成する)能力は、大部分において、

目標の決算残高を上回る財務省の能力。財務省とFRBの間の日々の接触は財務省に「多くの機会を提供します。

望ましい目的を達成するために当局を確保しなさい」[Auerbach 1963、328]。

残念なことに、財務省は、連邦の協力があっても不可能です。

税金とローンを使った日々の支出の影響を完全に相殺するための準備金

電話と直接投資。確かに、表1が示すように、財務省の平均

月次決算残高は、目標の50億ドルとは大きく異なる可能性があります。

これもまた、のサイズ/タイミングに関する固有の不確実性の結果です。

領収書と支出。この不確実性がどのように防止するのかを理解するのは簡単ですが

相互の相殺による日々の流入と流出は、

月次平均では、財務省の残高は最大31パーセントを閉じることができます。

その目標レベルを超えています。したがって、図5が確認しているように、

財務省の毎日の決算残高。それにもかかわらず、日々の決算残高の変動はほぼゼロ付近で変動する傾向があります。

四半期ごとの納税(1月、4月、6月、9月)および源泉徴収された事業税の徴収。

表1.(これに短い説明的なタイトルを付ける)

月平均決算残高($百万)

1997年11月5,015

1997年12月5,371

1998年1月6,563

1998年2月5,118日

1998年3月5,763

5ヶ月平均5,618

出典:毎日の財務諸表、http://fedbbs.access.gop.gov/dailys.htm

図5.日次決算残高の推移(1997年11月 - 1998年3月)

10,000

= 8,000

> 6,000

4,000

2,000

O__ 0A A-

-2,000

〜) - 4000

Z-6000

。 -8,000 05 'O LO 0 t(DC CY

出典:毎日の財務諸表、http://fedbb.acsgop.n co

出典:毎日の財務諸表、http://fedbbs.access.gop.gov/dailys.htm

611:

In sum, three important points have been made regarding the Treasury's operations. First, the Treasury recognized the disruptive nature of its cash operations and

responded by maintaining accounts at private depositories. Second, the Treasury

uses these accounts to diminish the reserve effect of its operations by using tax and

loan calls and direct investments to minimize the net changes in Reserve account

balances (to coordinate the flow of its receipts with its expenditures). Finally, the

Treasury and the Fed cooperate to bring about a fairly high degree of harmony in

managing the Treasury's balances at Reserve banks.

SeUling Bonds to Coordinate the Treasury's Operations

So far we have addressed only the Treasury's attempts to balance its taxing and

spending flows in order to minimize the reserve effect of its operations. Implicit in

our discussion, therefore, was the notion that the government attempts to balance its

budget. What if it doesn't? That is, what if the government runs a budget deficit?

How does the sale of bonds affect the Treasury's cash flow operations and, subsequently, the reserve effect? There are three scenarios that must be analyzed in order to determine the reserve effect of selling bonds, the key being by whom and

how are they purchased.

First, it must be recognized that tax and loan accounts actually receive not only

proceeds from tax payments, but also funds from the sale of government debt.

When commercial banks with tax and loan accounts (or customers of these banks)

purchase government bonds, there may be no immediate loss of reserves to the purchasing bank or the banking system. If, when the Treasury auctions new debt, it

specifies that at least some portion of the bonds are eligible for purchase by credit to

tax and loan accounts, Special Depositories may acquire the bonds by crediting deposits (in the name of the U.S. Treasury). These depositories, therefore, will not

lose reserves as they purchase newly issued bonds.F4 Similarly, the purchase of

newly issued government debt by a customer of a Special Depository, as long as the

Treasury specifies that some (or all) of the offering is eligible for purchase by tax

and loan credit, will leave reserves unaffected. For example, when a customer of a

Special Depository purchases government securities, the Treasury redeposits the

check into the bank on which the check was drawn. The bank then credits the Treasury's tax and loan account, offsetting the debit to the buyer's account. Thus, like the

purchase of government debt by a Special Depository, the sale of government debt

to a customer of one of these institutions can be effected without any loss of reserves.

The second method concerns the private purchase of newly issued government

debt that does not involve crediting a tax and loan account.

612:

When the securities are ineligible for purchase by tax and loan account credit and/or are not purchased by a

so-called "note-option" bank (or one of its customers), the purchase of government

bonds will immediately drain reserves from both the bank and the banking system.

This is because the proceeds from the sale of the securities will not stay "in the system," but will be deposited directly into one of the Treasury's accounts at a Federal

Reserve bank. When bonds are sold in this way, member bank reserves decline as

the Federal Reserve credits the Treasury's account, increasing the right-hand

bracket in Figure 1. Thus, a bank wishing to purchase U.S. government securities,

when tax and loan credit is not an option, will do so by drawing on its account at

the Federal Reserve. A system-wide loss of reserves will, therefore, accompany

every private purchase of newly issued government debt not eligible for payment

through tax and loan credit.

Finally, the sale of Treasury securities to the Federal Reserve must be considered. If the Fed purchases newly issued bonds directly from the Treasury, it will not

cause a change in member bank reserves. This, as Figure 1 makes clear, is because

both the right-hand bracket (U.S. Treasury Balance at Fed ) and the left-hand

bracket (U.S. Government Securities ) increase by the same amount, leaving total

reserves unaffected. Furthermore, since the government's balance sheet can be considered on a consolidated basis, given by the sum of the Treasury's and Federal Reserve's balance sheets with offsetting assets and liabilities simply canceling one

another out [Tobin 1998], the sale of bonds by the Treasury to the Fed is simply an

internal accounting operation, which provides the government with a self-constructed spendable balance. Although self-imposed institutional constraints may prevent the Treasury from creating all of its deposits in this way, there is no financial

constraint to prevent it from doing so. [15]

Now, the Treasury clearly has choices regarding the manner in which newly issued bonds will be sold. For example, if the government plans to engage in deficit

spending, the Treasury can sell bonds, allow them to be purchased by tax and loan

credit, and thereby eliminate any immediate impact on reserves. [16 ] When the Treasury sells bonds in this way, the bonds act as a sort of ex ante coordination tool.

Since the Treasury can control the size and timing of funds transferred from tax and

loan accounts, this type of bond sale helps the Treasury to drain (more or less) the

same number of reserves from the system that are being added to the system as a result of its deficit spending. [17 ]

If, however, there is a problem with the coordination (for example, if the Treasury and Fed underestimate the amount of checks that are drawn on the Treasury's

account at the Fed), bonds could be sold in order to drain excess reserves. [18] In other

words, insufficient tax and loan calls (which result in a system-wide increase in reserves and threaten to send the overnight lending rate to a zero percent bid) could

prompt the sale of bonds as an ex post coordination tool.

613:

In order to immediately drain the excess reserves, banks could not be allowed to purchase the bonds by

crediting a tax and loan account, but this is something the Treasury can specify.

The Nuances of Reserve Accounting

The purpose of this section is twofold. First, the commonly held belief that the

purpose of collecting taxes and selling bonds is to provide the government with the

financial resources that fund its expenditures will be examined. The question will be

addressed intuitively, drawing on the reserve effects analyzed in the first three sections of the paper. Second, for those who remain unconvinced by the intuitive analysis, the question as to whether the proceeds from taxes and bond sales are even

capable of financing government spending will be considered. The argument requires an application of basic accounting principles to an analysis of reserve accounting in order to determine whether it is possible to use the revenues from

taxation and the sale of bonds to finance the government's spending.

There is surely no doubt that the proceeds from taxation and bond sales are de-

posited into accounts held by the U.S. Treasury (either with commercial banks or at

the Federal Reserve) and that the government spends by writing checks on Treasury

accounts at Reserve banks. Moreover, since funds are transferred from tax and loan

accounts to the Treasury's account at the Fed in order to cover anticipated shortfalls

in these accounts, it certainly looks as though the purpose of taxing and selling

bonds is to fund expenditures. This coordination undoubtedly supports the belief that

taxes and bond sales are necessary sources of government revenue. But the coordination of taxation and bond sales with (deficit) spending is actually a somewhat different operation.

An intuitive analysis of Treasury operations suggests a practical motivation for

the coordination of taxation and bond sales with government spending. Specifically,

because of the reserve effects of taxing, spending, and selling bonds, the government chooses to coordinate these operations in order to mitigate the impact on

banks' reserve positions and, hence, on short-term interest rates. This interdependence, then, is not defacto evidence of a financing role for taxes and bonds.

Similarly, the government need not borrow from the private sector by issuing

bonds in order to enable it to spend in excess of current taxation. This, again, is because the government can always create its own spendable balance internally (on its

consolidated balance sheet) by offsetting a Treasury liability against a Federal Reserve asset (e.g., but not necessarily, a Treasury bond). In the absence of private

bond sales, deficit spending would result in a net increase in aggregate bank reserves. Bonds, then, are used to coordinate deficit spending, draining what would

otherwise become excess reserves. Govermnent debt provides the private sector

with an interest-earning alternative to non-interest-bearingovernment currency, allowing the government to spend in excess of taxation without driving the overnight lending rate down.

614:

Thus, taxes can be viewed as a means of creating and maintaining a demand for the government's money, while bonds, which are used to prevent

deficit spending from flooding the system with excess reserves, are a tool that allows positive overnight lending rates to be maintained. Their coordination, it is argued here, is undertaken for pragmatic rather than "financial" reasons.

There is a danger that this argument may be viewed as pure semantics. This is

not so. That is, while it is certainly appropriate to consider taxation and bond sales

as part of the process of government finance, the implicit treatment of money, in its

physical form, being transferred from the private to the public sector results in a

misleading treatment of taxes and bond sales as necessary sources of government

revenue. In a world where money has been effectively divorced from commodities,

and where public and private sectors can vary the amount of money to be spent, this

naive way of thinking can be highly deceptive.

That such a treatment could have gone uncontested for so long is, perhaps, surprising. Indeed, some readers may resist accepting the claims made in this paper on

the grounds that they would, were they correct, have been made long ago. But there

have been a number of earlier critics who, although they did not undertake a detailed analysis of the institutional workings of government finance, reached similar

conclusions. Abba Lerner, for example, argued that "taxing is never to be undertaken merely because the government needs to make money payments" [1943, 40].

He further recognized that the government should sell bonds "only if it is desirable

that the public should have less money and more government bonds, for these are

the effects of government borrowing," adding that "this might be desirable if otherwise the rate of interest would be reduced too low" [1943, 40]. Thus, the main

points made in this paper were made long ago, but they did not succeed in overthrowing existing theories regarding the nature of government finance.

Perhaps this was because Lerner, who attempted to persuade his opponents on

logical grounds alone, provided no evidence to support his claims. A more compelling case can be made, it is argued here, through an application of simple accounting. The argument is a technical one and requires an understanding that Federal

Reserve notes (and reserves) are booked as liabilities on the Fed's balance sheet and

that these liabilities are extinguished/discharged when they are offered in payment to

the state. It must also be recognized that when currency or reserves return to the

state, the liabilities of the state are reduced, and high-powered money is destroyed.

The destruction of these promises is no different from the private destruction of

a promise once it has been fulfilled. In other words, when a bank makes a loan to an

individual, it results in a promise to the bank. Once the promise is kept (i.e., the

loan is repaid), the loan debt is eliminated from the borrower's balance sheet. Likewise, the state, once it fulfills its promise to accept its own money (high-powered

money) at state pay-offices, eliminates an equivalent number of these liabilities from

its balance sheet.

615:

Thus, while bank money (MI) is destroyed when demand deposits are used to

pay taxes, the government's money, high-powered money, is destroyed as the funds

are placed into the Treasury's account at the Fed. Viewed this way, it can be convincingly argued that the money collected from taxation and bond sales cannot possibly finance the government's spending. This is because in order to get its hands on

the proceeds from taxation and bond sales, the government must destroy what it has

collected. Clearly, government spending cannot be financed by money that is destroyed when received in payment to the state.

How, if not by using the money received in payment of taxes and bond sales,

does the government finance its spending? Notice that the government writes checks

on an account that does not comprise part of the money supply or high-powered

money, but that when it does, the funds become part of the money supply (Ml if deposited into checking accounts, M2 if into savings accounts, etc.) and part of the

monetary base. It is therefore apparent that while the payment of taxes destroys an

equivalent amount of money (MI immediately and high-powered money as the proceeds go into the Treasury's account at the Fed), spending from this account creates

an equivalent amount of new money-both bank money and high-powered money.

In short, the government finances all of its spending through the direct creation of

new (high-powered) money.

Summary and Conclusions

If the government (Fed and Treasury) had no regard for the "reserve effect" of

its operations, it would have little use for tax and loan accounts. It could simply create its own spendable deposit (on its consolidated balance sheet) and then spend

without regard for the size/timing of its tax receipts. But this behavior would frequently leave a banking system which was previously satisfied with its reserve position, with substantially more excess reserves than it wished to maintain. A system

flush with excess reserves would find few bidders for these funds, and the overnight

lending rate would fall toward zero. Taxes, as they drifted in, would drain a portion

of the excess reserves. Still, the funds rate could remain at a zero percent bid for a

prolonged period of time.

In order to move to any positive funds rate, either the Federal Reserve or the

Treasury would be forced to sell bonds to drain excess reserves. Banks, not wishing

to hold an excessive amount of non-interest-bearing government money, would be

all too happy to exchange non-interest-earning reserves for interest-bearing Treasury

bonds. The bonds would have to be sold until enough excess reserves had been

drained to yield a positive (target) funds rate. Although this process of adding and

later draining reserves could work, it would involve substantial variation in the level

of reserves and, subsequently, significant turmoil in the market for federal funds.

616:

Knowing that these are the undesirable effects of disregarding the reserve effects of

its operations, the Treasury chooses to coordinate its operations, transferring funds

from tax and loan accounts (draining reserves) as it spends from its account at the

Fed.

Taxes are not capable of financing government spending when they are paid using high-powered money (i.e., by cash or check in a fiat money system). In order

for the government to get its hands on the proceeds from taxation, it must place

these funds into the Treasury's account at the Fed. As it does, the banking system

loses an equivalent amount of desired and/or required reserves (either immediately

or as the Treasury transfers the proceeds from tax and loan accounts into its accounts at Reserve banks), and an equivalent amount of high-powered money is destroyed. Similarly, reserves are drained, and high-powered money is destroyed

when the Treasury issues bonds (immediately if tax and loan credit is not allowed or

with a lag as the proceeds are transferred from tax and loan accounts). In contrast,

government spending from the Treasury's account at the Fed injects reserves and

creates an equivalent amount of new money (MI, M2, etc., and high-powered

money).

It is impossible to perfectly balance (in timing and amount) the government's receipts with its expenditures. The best the Treasury and the Fed can do is to compare

estimates of anticipated changes in the Treasury's account at the Fed and to transfer

approximately the correct amount to/from tax and loan accounts. Errors due to excessive or insufficient tax and loan calls are the norm. Although same-day calls and

direct investments are designed to permit the authorities to react to these errors,

they are not always an option.

When the Treasury is unable to correct these errors on its own, the Federal Reserve may have to offset changes in the Treasury's closing balance. This will be

necessary whenever the errors are large enough to move the funds rate away from

its target rate. In fact, as argued previously, the uncertainty faced by monetary

authorities is often primarily due to uncertainty regarding the Treasury's balance at

the Fed. Its role as an offsetting agency is essentially forced upon it by its commitment to a target funds rate. Indeed, William Poole [1975] goes further, stating that

the Fed will usually abandon any other objective target in order to maintain the

funds rate within its tolerance range. The adding/draining of reserves, then, is

largely non-discretionary, as monetary policy is concerned primarily with maintaining the overnight lending rate. Fiscal policy, in contrast, has more to do with determining the supply of high-powered money than is usually acknowledged. Moreover,

while both taxation and bond sales drain reserves from the banking system, neither

provides the government with money with which to finance its spending. Indeed,

both taxation and bond sales lead (ultimately) to the destruction of high-powered

money.

In addition to a reconsideration of taxation and bond sales as financing operations, perhaps it is time to reassess the definitions of monetary and fiscal policy.

account at the Fed), bonds could be sold in order to drain excess reserves. [18] In other

words, insufficient tax and loan calls (which result in a system-wide increase in reserves and threaten to send the overnight lending rate to a zero percent bid) could

prompt the sale of bonds as an ex post coordination tool.

611:

要するに、財務省の業務に関して3つの重要な点が指摘されています。第一に、財務省はその現金業務の破壊的な性質を認識し、

民間の保管庫で口座を維持することによって対応した。第二に、財務省

これらの勘定科目を使用して、税金を使用して事業の準備金効果を軽減します。

準備金口座の純変動を最小限に抑えるためのローンコールおよび直接投資

収支(領収書の流れと支出の調整)最後に、

財務省とFRBは共同でかなり高度の調和をもたらすために協力する。

準備銀行で財務省の残高を管理する。

財務省の業務を調整するための保証債券

これまでのところ、我々は、その課税と財務のバランスをとるための財務省の試みのみを取り上げてきた。

事業の準備金効果を最小限に抑えるための支出の流れ。に暗黙のうちに

したがって、私たちの議論は、政府が政府のバランスを取ろうとしているという考えでした。

予算。そうでない場合はどうなりますか?つまり、政府が財政赤字を抱えているとしたらどうでしょうか。

債券の売却は財務省のキャッシュフロー業務にどのような影響を及ぼし、ひいては引当金の効果にどのような影響を与えるのでしょうか。売却債券の準備効果を決定するために分析しなければならない3つのシナリオがあります。

購入方法は?

第一に、税金とローンの口座は実際に受け取るだけではないことを認識しなければなりません。

納税による収入だけでなく、政府債務の売却による資金もあります。

税金およびローン口座を持つ商業銀行(またはこれらの銀行の顧客)

国債を購入した場合、購入銀行または銀行システムへの準備金の即時損失はない可能性があります。もし、財務省が新しい債務を競売にかけたとき、それは

債券の少なくとも一部が貸付対象として購入する資格があることを指定します。

税金とローンの口座では、特別寄託機関は(米国財務省の名義で)預金を貸方に入れることによって債券を取得することができます。したがって、これらの寄託機関はそうではありません。

彼らが新しく発行された債券を購入するときに準備金を失う。F4同様に、の購入

特別預託金の顧客による新たに発行された政府債務

財務省は、オファリングの一部(または全部)が税金による購入の対象であると明記しています。

そして貸付金は、準備金に影響を与えないままになります。たとえば、の顧客が

特別預金は政府証券を購入し、財務省は

小切手が描かれた銀行にチェックインします。その後、銀行は財務省の税金およびローン勘定を貸方記入し、借方を買い手の口座に振り替えます。したがって、のように

特別寄託による公債の購入、公債の売却

これらの機関のうちの1つの顧客への支払は、積立金を失うことなく行うことができます。

2番目の方法は、新たに発行された政府の私募に関するものです。

税金およびローン口座への入金を含まない債務。

612:

有価証券が税金およびローン口座のクレジットによる購入に不適格であるか、または

いわゆる "ノートオプション"銀行(またはその顧客の一人)、政府の購入

債券は直ちに銀行と銀行システムの両方から準備金を排出します。

これは、有価証券の売却による収入が「システム内」に留まるのではなく、連邦の財務省の口座に直接入金されるためです。

準備銀行このように債券が売られると、加盟銀行の準備金は以下のように減少します。

連邦準備制度理事会は財務省の口座を貸方に記入し、右側の

したがって、米国政府の証券を購入したい銀行は、

税金とローンの貸方が選択肢ではない場合は、以下の口座から引き出してください。

連邦準備制度。したがって、システム全体での準備金の損失はそれに伴います。

新たに発行された公債のうち、支払いの対象にならないものを個人で購入するたび

税金とローンのクレジットを通じて。

最後に、連邦準備制度への財務省証券の売却を考慮する必要があります。 FRBが財務省から直接新たに発行された債券を購入する場合、それはしません。

加盟銀行の準備金を変更する。これは、図1から明らかなように、

右側の括弧(米国財務省FRB)と左側の括弧の両方

かっこ(米国政府証券)も同額増加し、合計が残ります。

影響を受けない予約。さらに、政府の貸借対照表は連結ベースで検討することができるので、財務省と連邦準備制度の貸借対照表と資産と負債を相殺して単純に相殺することによって得られる。

もう1つのアウト[Tobin 1998]、財務省によるFRBへの債券の売却は、単に

これは政府に自己構築された支出バランスを提供するものです。自主的な制度上の制約により、財務省がこのようにしてすべての預金を創出することを妨げる可能性がありますが、経済的な理由はありません。

それを防ぐための制約。 [15]

現在、財務省には、新たに発行された債券の売却方法に関する選択が明確にあります。たとえば、政府が赤字に取り組むための車線

支出、財務省は債券を売却することができ、それらを税金とローンで購入することができます。

それにより、積立金への即時の影響がなくなります。このように財務省が債券を売却すると、その債券は一種の事前調整ツールとして機能する。

財務省は税金から譲渡される資金の規模と時期を管理できるため、

ローン口座、この種の債券売却は、財務省が(多かれ少なかれ)資金を流出させるのに役立ちます。

赤字支出の結果としてシステムに追加されているシステムからの同数の準備金。 [17]

ただし、調整に問題がある場合(たとえば、財務省とFRBが財務省の小切手に引き出される小切手の金額を過小評価している場合など)

連邦準備制度によると、余剰準備金を流出させるために債券を売却することができます。 [18]その他

つまり、不十分な税金やローンの呼び出し(システム全体の準備金の増加につながり、夜間の貸出金利を0%の入札に送信する恐れがあります)。

事後調整ツールとして債券の売却を促進する。

613:

In order to immediately drain the excess reserves, banks could not be allowed to purchase the bonds by

crediting a tax and loan account, but this is something the Treasury can specify.

The Nuances of Reserve Accounting

The purpose of this section is twofold. First, the commonly held belief that the

purpose of collecting taxes and selling bonds is to provide the government with the

financial resources that fund its expenditures will be examined. The question will be

addressed intuitively, drawing on the reserve effects analyzed in the first three sections of the paper. Second, for those who remain unconvinced by the intuitive analysis, the question as to whether the proceeds from taxes and bond sales are even

capable of financing government spending will be considered. The argument requires an application of basic accounting principles to an analysis of reserve accounting in order to determine whether it is possible to use the revenues from

taxation and the sale of bonds to finance the government's spending.

There is surely no doubt that the proceeds from taxation and bond sales are de-

posited into accounts held by the U.S. Treasury (either with commercial banks or at

the Federal Reserve) and that the government spends by writing checks on Treasury

accounts at Reserve banks. Moreover, since funds are transferred from tax and loan

accounts to the Treasury's account at the Fed in order to cover anticipated shortfalls

in these accounts, it certainly looks as though the purpose of taxing and selling

bonds is to fund expenditures. This coordination undoubtedly supports the belief that

taxes and bond sales are necessary sources of government revenue. But the coordination of taxation and bond sales with (deficit) spending is actually a somewhat different operation.

An intuitive analysis of Treasury operations suggests a practical motivation for

the coordination of taxation and bond sales with government spending. Specifically,

because of the reserve effects of taxing, spending, and selling bonds, the government chooses to coordinate these operations in order to mitigate the impact on

banks' reserve positions and, hence, on short-term interest rates. This interdependence, then, is not defacto evidence of a financing role for taxes and bonds.

Similarly, the government need not borrow from the private sector by issuing

bonds in order to enable it to spend in excess of current taxation. This, again, is because the government can always create its own spendable balance internally (on its

consolidated balance sheet) by offsetting a Treasury liability against a Federal Reserve asset (e.g., but not necessarily, a Treasury bond). In the absence of private

bond sales, deficit spending would result in a net increase in aggregate bank reserves. Bonds, then, are used to coordinate deficit spending, draining what would

otherwise become excess reserves. Govermnent debt provides the private sector

with an interest-earning alternative to non-interest-bearingovernment currency, allowing the government to spend in excess of taxation without driving the overnight lending rate down.

614:

Thus, taxes can be viewed as a means of creating and maintaining a demand for the government's money, while bonds, which are used to prevent

deficit spending from flooding the system with excess reserves, are a tool that allows positive overnight lending rates to be maintained. Their coordination, it is argued here, is undertaken for pragmatic rather than "financial" reasons.

There is a danger that this argument may be viewed as pure semantics. This is

not so. That is, while it is certainly appropriate to consider taxation and bond sales

as part of the process of government finance, the implicit treatment of money, in its

physical form, being transferred from the private to the public sector results in a

misleading treatment of taxes and bond sales as necessary sources of government

revenue. In a world where money has been effectively divorced from commodities,

and where public and private sectors can vary the amount of money to be spent, this

naive way of thinking can be highly deceptive.

That such a treatment could have gone uncontested for so long is, perhaps, surprising. Indeed, some readers may resist accepting the claims made in this paper on

the grounds that they would, were they correct, have been made long ago. But there

have been a number of earlier critics who, although they did not undertake a detailed analysis of the institutional workings of government finance, reached similar

conclusions. Abba Lerner, for example, argued that "taxing is never to be undertaken merely because the government needs to make money payments" [1943, 40].

He further recognized that the government should sell bonds "only if it is desirable

that the public should have less money and more government bonds, for these are

the effects of government borrowing," adding that "this might be desirable if otherwise the rate of interest would be reduced too low" [1943, 40]. Thus, the main

points made in this paper were made long ago, but they did not succeed in overthrowing existing theories regarding the nature of government finance.

Perhaps this was because Lerner, who attempted to persuade his opponents on

logical grounds alone, provided no evidence to support his claims. A more compelling case can be made, it is argued here, through an application of simple accounting. The argument is a technical one and requires an understanding that Federal

Reserve notes (and reserves) are booked as liabilities on the Fed's balance sheet and

that these liabilities are extinguished/discharged when they are offered in payment to

the state. It must also be recognized that when currency or reserves return to the

state, the liabilities of the state are reduced, and high-powered money is destroyed.

The destruction of these promises is no different from the private destruction of

a promise once it has been fulfilled. In other words, when a bank makes a loan to an

individual, it results in a promise to the bank. Once the promise is kept (i.e., the

loan is repaid), the loan debt is eliminated from the borrower's balance sheet. Likewise, the state, once it fulfills its promise to accept its own money (high-powered

money) at state pay-offices, eliminates an equivalent number of these liabilities from

its balance sheet.

613:

余剰準備金を即座に排出するために、銀行は

税金とローンの勘定科目を入金するが、これは財務省が指定できるものです。

準備会計のニュアンス

このセクションの目的は2つあります。まず、一般的に考えられている

税金を徴収し、債券を販売する目的は、政府に

その支出を賄う財源が検討されます。質問は

本稿の最初の3つのセクションで分析した予備効果を利用して直感的に説明した。第二に、直感的な分析に納得がいかない人々にとって、税金と債券売却による収入が平等であるかどうかについての質問です。

政府の支出に資金を供給できる能力が考慮されるでしょう。議論は、からの収益を使用することが可能であるかどうかを判断するために、予備会計の分析への基本的な会計原則の適用を要求する。

政府の支出を賄うための課税および公債の売却。

課税や債券売却による収入が減っていることは間違いありません。

米国財務省が保有する口座に(商業銀行または

そして連邦政府が財務省に小切手を書くことによって費やすこと

準備銀行の口座。さらに、資金は税金とローンから転送されるので

予想される不足分を補うために連邦準備理事会の財務省の口座に口座

これらの勘定科目では、課税と売却の目的のように見えます。

債券は支出に資金を提供することです。この調整は、次のような考えを疑いなく支持しています。

税金と債券の売り上げは、政府の収入の必要な源です。しかし、課税と債券販売と(赤字)支出の調整は、実際には多少異なる操作です。

財務業務の直観的な分析は、

政府支出による課税および債券販売の調整。具体的には、

課税、支出、および債券の売却による準備金の影響により、政府はこれらの業務を調整して、

銀行の準備ポジション、したがって、短期金利。それで、この相互依存は、税金と債券のための資金調達の役割の事実上の証拠ではありません。

同様に、政府は民間セクターからの発行によって借りる必要はない。

それが現在の課税を超えて使うことを可能にするために債券。これもまた、政府が常に国内で(支出に関して)自らの支出可能な収支を作り出すことができるからである。

連邦準備資産に対する財務省負債を相殺することによる連結貸借対照表(例えば、必ずではないが財務省債)。プライベートがない場合

債券の売上げ、赤字の支出は、銀行の準備金総額の純増につながります。そして、債券は赤字支出を調整するために使われ、

それ以外の場合は超過準備になります。政府債務は民間部門を提供する

利子のない政府通貨の代わりに利子を稼ぐ代替手段を使用すると、政府は一晩の貸出金利を引き下げることなく課税を超えて費やすことができます。

614:

このように、税は政府のお金の需要を創出し維持するための手段と見なすことができます。

システムに過剰な準備金があふれることによる赤字支出は、前向きな一晩の貸出金利を維持することを可能にするツールです。彼らの調整は、ここで論じられているように、「経済的」な理由ではなく実際的な理由で行われています。

この議論が純粋な意味論と見なされるかもしれないという危険があります。これは

そうではありません。つまり、課税と債券売却を検討することは確かに適切ですが

政府の資金調達のプロセスの一部として、暗黙の

民間部門から公共部門に移管される物理的形態は、

政府の必要な情報源としての税および債券売却の誤解を招く取り扱い

収入お金が商品から効果的に分離されている世界では、

そして公共部門と民間部門が費やす金額を変えることができるところでは、

素朴な考え方は非常に欺くことができます。

そのような治療法が長い間論争の余地がなかったかもしれないということは、おそらく驚くべきことです。確かに、何人かの読者はこのペーパーでなされる要求を受け入れることに抵抗するかもしれません

彼らがするであろう根拠は、彼らが正しいとすれば、ずっと前になされたものです。しかしそこに

彼らは政府財政の制度的な働きの詳細な分析を引き受けなかったけれども、それらが類似したに達した多くの初期の批評家であった

結論例えば、Abba Lernerは、「政府が金銭を支払う必要があるからといって、課税が行われることは決してない」と主張した[1943、40]。

彼はさらに、政府が債券を売却すべきであることを認めた」

公衆はより少ないお金とより多くの国債を持っているべきだと

「借りる」政府の借用の影響

利子率が低くなり過ぎるだろう」[1943、40]。

この論文で述べられた点はずっと前になされたものですが、政府財政の本質に関する既存の理論を覆すことには成功しませんでした。

おそらくこれは、対戦相手を説得しようとしたLernerが

論理的な理由だけでは、彼の主張を支持する証拠は得られなかった。より説得力のある訴訟を起こすことができます、それはここで、単純な会計の適用を通して論じられます。議論は技術的なものであり、その連邦の理解を必要とします

準備手形(および準備金)は、連邦準備理事会の貸借対照表に負債として計上されている。

これらの負債は、支払われたときに消滅/消滅すること。

状態。また、通貨や準備金が

国家、国家の責任が軽減され、強力な資金が破壊されます。

これらの約束の破壊は、の私的な破壊と変わらない。

それが達成されたら約束。言い換えれば、銀行が

個人、それは銀行への約束をもたらします。約束が守られると(すなわち、

ローンが返済された場合、ローン債務は借り手の貸借対照表から消去されます。同様に、国家は、いったんそれ自身のお金を受け入れるという約束を果たしたら

州の有料事務所では、同額のこれらの負債を

そのバランスシート。

615:

Thus, while bank money (MI) is destroyed when demand deposits are used to

pay taxes, the government's money, high-powered money, is destroyed as the funds

are placed into the Treasury's account at the Fed. Viewed this way, it can be convincingly argued that the money collected from taxation and bond sales cannot possibly finance the government's spending. This is because in order to get its hands on

the proceeds from taxation and bond sales, the government must destroy what it has

collected. Clearly, government spending cannot be financed by money that is destroyed when received in payment to the state.

How, if not by using the money received in payment of taxes and bond sales,

does the government finance its spending? Notice that the government writes checks

on an account that does not comprise part of the money supply or high-powered

money, but that when it does, the funds become part of the money supply (Ml if deposited into checking accounts, M2 if into savings accounts, etc.) and part of the

monetary base. It is therefore apparent that while the payment of taxes destroys an

equivalent amount of money (MI immediately and high-powered money as the proceeds go into the Treasury's account at the Fed), spending from this account creates

an equivalent amount of new money-both bank money and high-powered money.

In short, the government finances all of its spending through the direct creation of

new (high-powered) money.

Summary and Conclusions

If the government (Fed and Treasury) had no regard for the "reserve effect" of

its operations, it would have little use for tax and loan accounts. It could simply create its own spendable deposit (on its consolidated balance sheet) and then spend

without regard for the size/timing of its tax receipts. But this behavior would frequently leave a banking system which was previously satisfied with its reserve position, with substantially more excess reserves than it wished to maintain. A system

flush with excess reserves would find few bidders for these funds, and the overnight

lending rate would fall toward zero. Taxes, as they drifted in, would drain a portion

of the excess reserves. Still, the funds rate could remain at a zero percent bid for a

prolonged period of time.

In order to move to any positive funds rate, either the Federal Reserve or the

Treasury would be forced to sell bonds to drain excess reserves. Banks, not wishing

to hold an excessive amount of non-interest-bearing government money, would be

all too happy to exchange non-interest-earning reserves for interest-bearing Treasury

bonds. The bonds would have to be sold until enough excess reserves had been

drained to yield a positive (target) funds rate. Although this process of adding and

later draining reserves could work, it would involve substantial variation in the level

of reserves and, subsequently, significant turmoil in the market for federal funds.

615:

したがって、デマンドデポジットを使用した場合、銀行のお金(MI)は破壊されます。

納税、政府の資金、強力な資金は、資金として破壊されます。

連邦機関の財務省の口座に置かれています。このように考えれば、課税や債券売却から集められたお金は政府の支出におそらく資金を供給することはできないと説得力を持って主張することができます。これは、手にするために

課税や債券売却からの収入、政府はそれが持っているものを破壊する必要があります

集めました。明らかに、政府支出は国家への支払いで受領されたときに破壊されるお金で賄われることはできません。

税金や債券の販売で受け取ったお金を使っていないのであれば、

政府はその支出に資金を供給していますか?政府が小切手を書くことに注意してください

マネーサプライの一部を構成していないアカウントまたは高電力

しかし、それが行われると、資金はマネーサプライの一部(当座預金口座に入金されている場合はM1、普通預金口座に入金されている場合はM2など)になります。

通貨ベース。したがって、税金の支払いが

この口座からの支出により、相当額の金額(MIが直ちに、収益がFRBの財務省の口座に入金されると高額の資金)が生み出されます。

同額の新しいお金 - 銀行のお金と強力なお金の両方。

要するに、政府はその直接の創出を通じてその支出のすべてに資金を供給しています。

新しい(強力な)お金。

まとめと結論

政府(FRBと財務省)が「予備力」を考慮しなかった場合

その操作は、それは税金やローンのアカウントにはほとんど使用されないでしょう。それは単に(自身の連結貸借対照表に)それ自身の支出可能な預金を作成してから支出することができます

その領収書のサイズ/タイミングに関係なく。しかし、この行動により、以前はその準備ポジションに満足していた銀行システムが頻繁に残され、維持することを望んでいたよりもはるかに多くの超過準備があります。システム

余分な準備金と同じ高さになると、これらの資金の入札者はほとんどなくなり、

貸出金利はゼロに向かって低下します。彼らが漂ったように、税金は一部を流出させるでしょう

余分な準備金の。それでも、ファンドレートはのために0パーセントの入札を維持することができます

長期間

任意のプラスの資金レートに移行するためには、連邦準備制度理事会または

財務省は余剰準備金を排出するために債券を売却することを余儀なくされるでしょう。銀行、希望しない

無利子の政府資金を過剰に保有することは、

無利子準備金を有利子負債に交換するのは非常にうれしいことです。

債券十分な余剰準備金が支払われるまで債券は売却されなければならないでしょう

プラスの(目標)ファンドレートを生み出すために排出された。この追加プロセスと

後に埋蔵量を枯渇させることはうまくいくかもしれない、それはレベルの実質的な変動を伴うだろう

その結果、連邦基金の市場に大きな混乱が生じました。

616:

Knowing that these are the undesirable effects of disregarding the reserve effects of

its operations, the Treasury chooses to coordinate its operations, transferring funds

from tax and loan accounts (draining reserves) as it spends from its account at the

Fed.

Taxes are not capable of financing government spending when they are paid using high-powered money (i.e., by cash or check in a fiat money system). In order

for the government to get its hands on the proceeds from taxation, it must place

these funds into the Treasury's account at the Fed. As it does, the banking system

loses an equivalent amount of desired and/or required reserves (either immediately

or as the Treasury transfers the proceeds from tax and loan accounts into its accounts at Reserve banks), and an equivalent amount of high-powered money is destroyed. Similarly, reserves are drained, and high-powered money is destroyed

when the Treasury issues bonds (immediately if tax and loan credit is not allowed or

with a lag as the proceeds are transferred from tax and loan accounts). In contrast,

government spending from the Treasury's account at the Fed injects reserves and

creates an equivalent amount of new money (MI, M2, etc., and high-powered

money).

It is impossible to perfectly balance (in timing and amount) the government's receipts with its expenditures. The best the Treasury and the Fed can do is to compare

estimates of anticipated changes in the Treasury's account at the Fed and to transfer

approximately the correct amount to/from tax and loan accounts. Errors due to excessive or insufficient tax and loan calls are the norm. Although same-day calls and

direct investments are designed to permit the authorities to react to these errors,

they are not always an option.

When the Treasury is unable to correct these errors on its own, the Federal Reserve may have to offset changes in the Treasury's closing balance. This will be

necessary whenever the errors are large enough to move the funds rate away from

its target rate. In fact, as argued previously, the uncertainty faced by monetary

authorities is often primarily due to uncertainty regarding the Treasury's balance at

the Fed. Its role as an offsetting agency is essentially forced upon it by its commitment to a target funds rate. Indeed, William Poole [1975] goes further, stating that

the Fed will usually abandon any other objective target in order to maintain the

funds rate within its tolerance range. The adding/draining of reserves, then, is

largely non-discretionary, as monetary policy is concerned primarily with maintaining the overnight lending rate. Fiscal policy, in contrast, has more to do with determining the supply of high-powered money than is usually acknowledged. Moreover,

while both taxation and bond sales drain reserves from the banking system, neither

provides the government with money with which to finance its spending. Indeed,

both taxation and bond sales lead (ultimately) to the destruction of high-powered

money.

In addition to a reconsideration of taxation and bond sales as financing operations, perhaps it is time to reassess the definitions of monetary and fiscal policy.

616:

617:

Fiscal policy has more, and monetary policy less, to do with the money supply than

is usually recognized. An analysis of reserve accounting reveals that all government

spending is financed by the direct creation of high-powered money; bond sales and

taxation are merely alternative means by which to drain reserves/destroy high-powered money. The debate over alternative "financing" methods, then, should really

be a debate over the alternative methods for draining reserves (taxes vs. bond sales)

in order to prevent the overnight lending rate from falling to zero. As Lerner

argued, it is not so-called "sound" but "functional" finance that modern governments

should practice, and this means using taxes and bonds "simply as instruments, and

not as magic charms that will cause mysterious hurt if they are manipulated by the

wrong people or without due reverence for tradition" [1943, 51].

これらの予備効果を無視することの望ましくない効果であることを知っている

その運用、財務省はその運用を調整し、資金を移動することを選択します

税金およびローン口座(準備金の流出)から

連邦機関

税金は、強力な資金を使って(すなわち、現金または金融システムでチェックインすることによって)支払われる場合、政府支出に資金を供給することはできません。順番に

政府が課税からの収入を手に入れるためには、

これらの資金はFRBの財務省の口座に入れられます。そうであるように、銀行システム

同額の希望および/または必要準備金を失う

あるいは、財務省が税金および融資口座からの収益を準備銀行の口座に振り込むと、相当額の高額の資金が破壊されます。同様に、準備金は排出され、強力な資金は破壊されます

財務省が債券を発行したとき(税金およびローンの貸方が認められない場合は直ちに

収入が税金とローンの口座から転送されるように遅れて)。対照的に、

連邦機関の財務省の口座からの政府支出は準備金を注入します

同等の量の新しいお金(MI、M2など)を作成し、高性能

お金)。

政府の収入とその支出を完全に(時期と量で)バランスさせることは不可能です。財務省とFRBができる最善のことは、比較することです。

FRBの財務省口座の予想される変更および譲渡の予想

税金とローンの勘定科目への/からのほぼ正しい金額。過剰または不十分な税金やローンの呼び出しによるエラーが一般的です。同日の電話と

直接投資は、当局がこれらの過誤に対応できるように設計されています。

それらは常に選択肢とは限りません。

財務省が単独でこれらの誤謬を訂正することができないとき、連邦準備制度理事会は財務省の決算残高の変動を相殺しなければならないかもしれない。これは次のようになります

エラーがファンドレートを変動させるのに十分なほど大きい場合はいつでも必要

目標レート実際、以前に議論されたように、金銭が直面する不確実性

当局は、多くの場合、主に財務省の財政状態に関する不確実性に起因します。

連邦機関。相殺機関としてのその役割は、基本的に目標資金率へのコミットメントによって強制されています。確かに、William Poole [1975]はさらに進んで、

連邦準備制度を維持するため、FRBは通常他の客観的目標を放棄します。

資金は許容範囲内で評価されます。したがって、準備金の追加/排出は、

金融政策は主に翌日物貸出金利の維持に関係しているため、大部分は裁量ではない。対照的に、財政政策は、通常認められている以上に、高資金の供給を決定することと関係があります。また、

課税と債券販売の両方が銀行システムから準備金を排出している間、どちらも

政府にその支出をまかなうための資金を提供します。確かに、

課税と債券販売の両方が(最終的には)強力なものの破壊につながる

お金。

財政運営としての課税と債券売却の再考に加えて、おそらく金融政策と財政政策の定義を見直す時が来たでしょう。

617:

Fiscal policy has more, and monetary policy less, to do with the money supply than

is usually recognized. An analysis of reserve accounting reveals that all government

spending is financed by the direct creation of high-powered money; bond sales and

taxation are merely alternative means by which to drain reserves/destroy high-powered money. The debate over alternative "financing" methods, then, should really

be a debate over the alternative methods for draining reserves (taxes vs. bond sales)

in order to prevent the overnight lending rate from falling to zero. As Lerner

argued, it is not so-called "sound" but "functional" finance that modern governments

should practice, and this means using taxes and bonds "simply as instruments, and

not as magic charms that will cause mysterious hurt if they are manipulated by the

wrong people or without due reverence for tradition" [1943, 51].

Notes

1. Early debates [Modigliani 1961; Blinder and Solow 1973, 1976; Barro 1974; Buiter 1977;

Lerner 1973; Tobin 1961] over the optimal method by which to finance deficit spending

remain a controversial topic today [Trostel 1993; Ludvigson 1996; Smith and Villamil

1998]. Despite differing beliefs about the macroeconomic consequences of, say, borrow-

ing vs. "printing money," economists on both sides of these debates clearly accept that the

purpose of collecting taxes and selling bonds is to secure funds that are then respent by the

government. In other words, it is generally agreed that the role of taxation and bond sales

is to transfer financial resources from households and businesses (as if transferring actual

dollar bills or coins) to the government, where they are respent (i.e., in some real sense

"used" to finance government spending). This erroneous view follows from an implicit

treatment of money in its physical form and can be avoided by considering the balance

sheet and reserve effects of taxation and bond sales. This, in short, is the purpose of this

paper.

2. Although reserve requirements are generally met by holding a combination of vault cash

and checking accounts at district Federal Reserve banks, accounts held by depository insti-

tutions at Federal Home Loan Banks, the National Credit Union Administration Central

Liquidity Facility, or correspondent banks may also count toward satisfying the reserve re-

quirement. Depository institutions do not have to meet these reserve requirements on a

daily basis. They have a two-week "reserve period" (ending on Wednesdays) within which

they must maintain average daily total reserves equal to the required percentage of average

daily transactions accounts held during the two-week period ending the preceding Mon-

day. Thus, despite being referred to as a contemporaneous reserve accounting (CRA) sys-

tem, it is, in practice, lagged for two days. That is, banks always have two days (Tuesday

and Wednesday) within which to acquire (ex post) reserves needed to eliminate a known

deficiency. While some banks may choose to hold excess reserves, profit-maximizing

banks will economize on reserves. Unless a bank has a preference for idle funds, it will

exchange excess reserves for "earning assets" such as loans or securities.

3. See Ranlett [1977, 191-1931 for the derivation.

4. It is, of course, true that the Treasury keeps accounts at thousands of commercial banks

and other depository institutions as well as Federal Reserve banks. This changes things

considerably and will be taken up in the next section.

5. It is worth noting that government spending must originally have preceded taxation. That

is, the payment of taxes could not increase the Treasury's account at the Fed (Figure 1,

right-hand bracket), reducing bank reserves, until the reserves had been created.

617: