Fiscal Requirements for Price Stability 2000

PAPER MONEY Sims

シムズが参照するのはWoodford 1995

WOODFORD, M. (1995): “Price Level Determinacy Without Control of a Monetary Aggregate,” Carnegie-Rochester Conference Series on Public Policy, 43, 1–46.

DEPARTMENT OF ECONOMICS, PRINCETON UNIVERSITY E-mail address: sims@princeton.edu

ワーキングペーパー

ウッドフォード1995は以下を参照

シムズは以下を

The optimum quantity of money - IDEAS/RePEc

Woodford, Michael, 1990. "The optimum quantity of money," Handbook of Monetary Economics,in: B. M. Friedman ...

Michael Dean Woodford (born 1955) is an American macroeconomist and monetary theorist who currently teaches at Columbia University.

Academic career

Woodford holds B.A. from the University of Chicago (1977) and a J.D. from Yale Law School (1980).[2] He completed his Ph.D. in economics at MIT in 1983.[3]

He began his teaching career at Columbia, and then taught at Chicago and Princeton before returning to Columbia to accept the John Bates Clark chair in 2004. He was awarded the John D. and Catherine T. MacArthur Foundation Prize Fellowship, which financed his research from 1981 to 1986. In 2007, he was awarded the Deutsche Bank Prize.[4]

Theoretical contributions

Woodford's early research topics included sunspot equilibria,[5] and imperfect competition.[6] Thereafter he began to work on macroeconomic models with sticky prices; together with Julio Rotemberg he developed one of the first microfounded New Keynesianmacroeconomic models.[7] Since then he has used this framework to study many topics related to monetary policy, including the fiscal theory of the price level,[8] the effectiveness of monetary policy as consumers use more credit and less cash,[9] and inflation targeting rules.[10] Michael Woodford has especially praised Knut Wicksell's advocacy of using the interest rate to maintain price stability, noting that this was a remarkable insight at a time when most monetary policy was based on the gold standard (Woodford, 2003, p. 32). Woodford calls his own framework 'neo-Wicksellian', and he titled his textbook on monetary policy in homage to Wicksell's work.

Interest and Prices

Woodford is probably best known as the author of an advanced textbook on monetary macroeconomics entitled Interest and Prices: Foundations of a Theory of Monetary Policy.[11][12] The book has, in the words of the Deutsche Bank Prize Committee, "quickly become the standard reference for monetary theory and analysis among academic economists and their colleagues at central banks."[4]

References

- ^ Woodford, Michael (1983), Essays in intertemporal economics. Ph.D. dissertation, Massachusetts Institute of Technology.

- ^ "Curriculum Vitae MICHAEL WOODFORD July 2017" (PDF). columbia.edu.

- ^ Woodford, Michael Dean (1983), Essays in Intertemporal Economics. Ph.D. dissertation, Massachusetts Institute of Technology.

- ^ a b "Michael Woodford: The Prize Winner 2007". October 4, 2007.

- ^ Woodford, Michael (1990). "Learning to believe in sunspots". Econometrica. 58 (2): 287–307. JSTOR 2938205.

- ^ Rotemberg, Julio; Woodford, Michael (1995). "Dynamic general equilibrium models with imperfectly competitive product markets". In Cooley, Thomas. Frontiers of Business Cycle Research. Princeton University Press. ISBN 0-691-04323-X.

- ^ Rotemberg, Julio J.; Woodford, Michael (1997). "An optimization-based econometric framework for the evaluation of monetary policy". NBER Macroeconomics Annual. 12: 297–346. JSTOR 3585236.

- ^ Woodford, Michael (2001). "Fiscal requirements for price stability". Journal of Money, Credit, and Banking. 33 (3): 669–728. JSTOR 2673890.

- ^ Woodford, Michael (1998). "Doing without money: controlling inflation in a post-monetary world". Review of Economic Dynamics. 1 (1): 173–219. doi:10.1006/redy.1997.0006.

- ^ Giannoni, Marc P.; Woodford, Michael (2005). "Optimal inflation targeting rules". In Bernanke, Ben; Woodford, Michael. The Inflation-Targeting Debate. Chicago: University of Chicago Press. pp. 93–172. ISBN 0-226-04472-6.

- ^ Woodford, Michael (2003). Interest and prices: Foundations of a theory of monetary policy. Princeton, New Jersey: Princeton University Press. ISBN 0-691-01049-8.

- ^ Green, Edward (2005). "A review of Interest and Prices". Journal of Economic Literature. 43: 121–134. doi:10.1257/0022051053737799.

External links

今週のJBpressのコラムもむずかしいので、FTPLの理論をちょっと解説しておこう。「ドルの取り付け」というのはCochraneの表現で、彼もいうように「インフレは貨幣的現象だ」というフリードマンの時代は終わった。需給ギャップの小さい低成長時代に物価を決めるのは、通貨供給ではなく財政赤字である。各国でデフレが続いているのは、政府債務が積み上がって財政赤字を削減しているためだ。

Pt=βtWt/wt

ここでβt≡1+itは、グロスの金利(割引率)である。t+1期の実質資産をwt+1、財政赤字(プライマリーバランス)をsとし、βとsを一定とすると、政府資産wtは

wt+1=β(wt-s)

という簡単な差分方程式で表現できる。金利iをプラスとするとβ>1なので、この式は図の実線のように、傾きが1より大きい直線になる。実質資産の初期値がw0だとすると、w1=β(w0-s)となり、同様にw2、w3…が決まる。

初期値がw*だった場合はw=w*となる45度線との交点(均衡財政)で安定するが、プライマリー黒字でw0>w*の場合(図の右上)は、Wtを一定とするとwtが上がってPが下がり、天井にぶつかって実質資産が拡大する非リカーディアン均衡になる。プライマリー赤字の場合(図の左下)は実質資産が縮小し、インフレで実質債務のデフォルトが起こる。物価(名目資産/実質資産)は上昇し、一定の水準で止まって非リカーディアン均衡(左下)になる。

これは複数均衡で、すべての人々が未来を合理的に予想するw*が(偶然)初期値だったときだけ、真ん中のリカーディアン均衡で安定する。そこに収斂するメカニズムはないので、それ以外の場合は実質資産と物価は発散するが、今の日本のように均衡からはずれているときは、非リカーディアン均衡に近づけば安定する。

追記:シムズのAEA会長講演は、この調整過程をテイラールールで分析し、財政インフレは収束すると論じている。直観的にいうと、代表的家計は政府から借金できないので、将来のある時点で予算制約に直面し、消費を縮小する。中央銀行が物価上昇率と同じ名目金利を設定すると実質所得は同じなので、消費はインフレに中立になり、予算制約で財政赤字はゼロに収束する。合理的予想の仮定をはずすと政府債務は振動するが、インフレが無限大に発散することはなく、物価水準は数倍ぐらいで安定する。

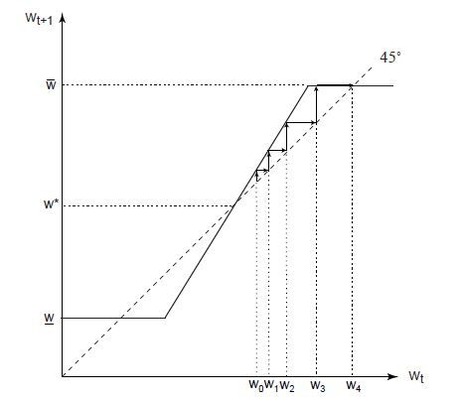

これをWoodford[Fiscal Requirements for Price Stability 2000 http://www.columbia.edu/~mw2230/jmcb.pdf]のモデルをさらに単純化して考えてみよう。t期の政府の名目資産をWt、実質資産をwtとし、物価水準Ptは政府の名目資産と実質資産の比(通貨供給の一般化)で決まるとすると、

Pt=βtWt/wt

ここでβt≡1+itは、グロスの金利(割引率)である。t+1期の実質資産をwt+1、財政赤字(プライマリーバランス)をsとし、βとsを一定とすると、政府資産wtは

wt+1=β(wt-s)

という簡単な差分方程式で表現できる。金利iをプラスとするとβ>1なので、この式は図の実線のように、傾きが1より大きい直線になる。実質資産の初期値がw0だとすると、w1=β(w0-s)となり、同様にw2、w3…が決まる。

初期値がw*だった場合はw=w*となる45度線との交点(均衡財政)で安定するが、プライマリー黒字でw0>w*の場合(図の右上)は、Wtを一定とするとwtが上がってPが下がり、天井にぶつかって実質資産が拡大する非リカーディアン均衡になる。プライマリー赤字の場合(図の左下)は実質資産が縮小し、インフレで実質債務のデフォルトが起こる。物価(名目資産/実質資産)は上昇し、一定の水準で止まって非リカーディアン均衡(左下)になる。

これは複数均衡で、すべての人々が未来を合理的に予想するw*が(偶然)初期値だったときだけ、真ん中のリカーディアン均衡で安定する。そこに収斂するメカニズムはないので、それ以外の場合は実質資産と物価は発散するが、今の日本のように均衡からはずれているときは、非リカーディアン均衡に近づけば安定する。

追記:シムズのAEA会長講演は、この調整過程をテイラールールで分析し、財政インフレは収束すると論じている。直観的にいうと、代表的家計は政府から借金できないので、将来のある時点で予算制約に直面し、消費を縮小する。中央銀行が物価上昇率と同じ名目金利を設定すると実質所得は同じなので、消費はインフレに中立になり、予算制約で財政赤字はゼロに収束する。合理的予想の仮定をはずすと政府債務は振動するが、インフレが無限大に発散することはなく、物価水準は数倍ぐらいで安定する。

0 Comments:

コメントを投稿

<< Home