#2:33

lenses

《Kuhn calls this a ‘scientific revolution’ and it has been likened to taking off distorting glasses and putting on prescription lenses that correct vision.》 ミッチェルMitchell 2019 詳細目次 https://nam-students.blogspot.com/2019/06/mitchell-2019.html

《…Keynes was a master of argument, but even he did not always win. More recently Deirdre McCloskey made a similar claim in her book The Rhetoric of Economics (1985). Her point is that evidence alone is not decisive; ‘rhetoric’, the art of discourse, is also important.》 (Mitchell 2019 #2:32)

The diagram above shows how the cumulative stock is held in what we term the Non-government Tin Shed which stores fiat currency stocks, bank reserves and government bonds. I invented this Tin Shed analogy to disabuse the public of the notion that somewhere down in Canberra was a storage area where the national government was putting all those surpluses away for later use – which was the main claim of the previous federal regime. There is actually no storage because when a surplus is run, the purchasing power is destroyed forever. However, the non-government sector certainly does have a Tin Shed within the banking system and elsewhere.

I have been travelling a lot today (nearly 6 hours starting early) and so haven’t much time for blog writing. I am working on a paper at present on the use of metaphors in economics and how Modern Monetary Theory (MMT) might usefully frame its offering to overcome some of the obvious prejudices that prevent, what are basic concepts, penetrating the public psyche. Here are some notes on that theme. The blog is just a rough sketch and will be refined over the coming weeks. There is a section at the end that encourages reader feedback – lets see what you think.

…

Don’t Buy It, Anat Shankar-Osorio

…

。。。

以下はレンズの比喩が出てくる別投稿、

MMT is what is, not what might be – Bill Mitchell – Modern Monetary Theory

What MMT provides is a new lens to view the world we live in and the monetary system operations that are important in our daily lives.

This new lens opens up new insights into what is going on in the economy on a daily basis. It’s not something to move to, it already is.

MMT, as a new powerful lens, makes things that are obscured by neo-liberal narratives more transparent.

It means that the series of interlinked myths that are advanced by conservative forces to distract us from understanding causality and consequence in policy-making and non-government sector decision-making are exposed.

So when a Conservative politician or corporate leader claims that the government has run out of money and therefore cannot afford income support for the unemployed any longer at the levels previously enjoyed, MMT alerts us to the fact that this is a lie and that there must be an alternative agenda.

MMT thus empowers a population who learn about it to see things for what they are and to ask questions that they never previously would have thought possible to ask or even relevant.

Previously, when a politician has said the government will run out of money or is maxing out its credit card, an uninformed population will take that statement as granted.

But an understanding of the MMT framework all its lens would mean that the population will now reject the “run out of money” obfuscation and instead demand to know why the government doesn’t want to support a particular policy option.

MMT thus, introduces into the policy debate, the possibility of new policy options and directions that have previously been dismissed out of hand through the use of spurious economic arguments that the politicians and their advisors know will not be properly scrutinised nor understood by the general population who they are trying to manipulate.

MMT is thus, a framework for understanding how the monetary system we live in operates and the capacities and options that are currency-issuing government has to advance our well-being.

It also allows us to understand the likely consequences of deviating from a truly sovereign state, which we define in terms of the currency-issuing status of the government (incorporating exchange-rate arrangements and central bank interest rate setting capacities).

In the latter context, the MMT lens provided us with a clear understanding of why the Eurozone would be a failure with significant negative consequences for the Member States.

Further, MMT is neither left-wing nor right-wing.

Where the confusion lies is in conflating the theoretical and descriptive content of MMT with the value systems that the proponents of MMT overlay on this content.

It might be thought that MMT is left-wing because the values I expound are from the left. But that would be a wrongful inference.

The ideological persuasion of any perspective will manifest in the values that are expounded and the policy prescriptions that are proposed to advance those values.

What MMT has allowed is for the ideological persuasion to become much clearer when a person advances a particular policy proposal.

For example, when a politician, faced with rising unemployment, says that there is no fiscal space for the government to create jobs to deal with the mass unemployment, a person considering that comment through the MMT lens, will immediately realise that the government must have a reason for maintaining higher than necessary unemployment.

「Cinq-Marsの受けた仕打ちはスペイン異端審問になぞらえられるひどいものだった。カンファレンスでは、聴衆たちはCinq-Marsのプレゼンにほとんど耳を貸さず、提示した証拠はぞんざいな扱いを受けた。他の研究者は礼儀正しく耳を傾け、その上でCinq-Marsの能力について疑問を呈した。結果はいつも同じだった…Canadian Museum of Historyの自分のオフィスで、Cinq-Marsは心を閉ざして苛立った。彼のBluefish Caves調査の資金は尽きていき、結局彼のフィールドワークはだんだん失速し、絶えてしまった。」

(神経生物学、考古学、経済学といった)学問分野は、既に構築された’パラダイム’の中で動いている。’パラダイム’は哲学者のThomas Kuhnの1962年の本 The Structure of Scientific Revolutions(邦題:科学革命の構造)の中で、”当座の間、専門家のコミュニティに対して定型問題とその解決法を提供する広範に認知された科学的業績”と定義されている。

One of the things I have noted with regularity is that readers and other second-generation Modern Monetary Theory (MMT) bloggers often fall into the error which we might characterise as the “When we have MMT things will be different” syndrome. Or the “we need to change to MMT principles to make things better” syndrome. Thinking that MMT constitutes a regime change is incorrect and steers one away from the core issues. In this blog, I reflect on that syndrome and some other aspects of the development of ideas, which I hope will provide readers with a clearer picture of what the core (early) MMT developers (Mosler, Bell/Kelton, Wray, Mitchell, Tcherneva, Fullwiler) had in mind when we set out in the early 1990s to construct a better way of doing macroeconomics. The point is that while MMT constitutes a regime change in economic thinking within the academy it does not constitute a regime change in the way the monetary system operates. We need to separate the operational principles exposed by MMT academics from their ideological values to really come to terms with the fact that MMT is what is, not what might be.

I have been reading the 2001 book What Evolution Is by the famous evolutionary biologist Ernst Mayr recently. He took on the establishment in his area of research and has definitely been a major influence on the way we think about biodiversity in modern times.

He was influential in the emphasis on secular explanations for evolution. In one interview in 1999 he was asked:

EDGE: How do you account for the fact that in this country, despite the effect of Darwinism on many people in the scientific community, more and more people are god fearing and believe in the 8 days of creation?

MAYR: You know you cannot give a polite answer to that question.

EDGE: In this venue we appreciate impolite, impolitical, answers.

MAYR: They recently tested a group of schoolgirls? They asked where is Mexico? Do you know that most of the kids had no idea where Mexico is? I’m using this only to illustrate the fact that and pardon me for saying so the average American is amazingly ignorant about just about everything. If he was better informed, how could he reject evolution? If you don’t accept evolution then most of the facts of biology just don’t make sense. I can’t explain how an entire nation can be so ignorant, but there it is.

That insight has bearing on how we think about macroeconomics as well and I will return to that soon.

His account of evolution is interesting and has parallels with the way other ideas develop, including those in economics.

To some extent, Mayr’s work constituted a ‘regime change’ in his discipline after resistance from the established thinkers. in another sense, his discussion of evolution itself has relevance to the ways ideas emerge and move from being unacceptable to broadly accepted.

Evolution, in Mayr’s work, involves novelty, changes to some species. Changes accumulate.

Our understanding of this process through time sometimes takes us down dead-ends or blind alleys as the new ideas are tested against reality.

These ‘mistakes’ in perception are important though, because while they cannot help us understand the reality of interest, they do provide other information that helps us see things in better perspective.

It doesn’t help us understand the way the monetary system operates. The mainstream explanations and characterisations are just plain wrong – and systematically so – one myth links into and reinforces another in a stream of logical nonsense.

But if you then ask why the mainstream adopt the position that they do, which in any reasonable assessment is ‘just plain wrong’ – then exploring that question is insightful because we enter the world of ideology and the role that ideas have in reinforcing existing power elites.

It is clear that the adoption of ‘free market’ conceptions help maintain the elite position in the deployment of real resources and the income flows that are derived.

So, while mainstream economics is bunkum, understanding its role is important and helps us understand why ‘better’ ideas struggle to gain ascendancy in the contest of ideas.

There are many examples of such ‘contests’ in the evolution of ideas.

I have previously noted the struggle of American biologist Joseph Altman.

He specialised in neurobiology and discovered adult neurogenesis in the 1960s. He showed that adult brains could create new neurons but the idea was fiercely denied by contemporary thought at the time.

The power elites in his field were challenged by the new ideas.

It wasn’t until the phenomenon was ‘rediscovered’ by another scientist (Elizabeth Gould in 1999) that the proposition became fashionable. Neurogenesis is now one of the most significant areas in neuroscience.

Why were Altman’s discoveries ignored for almost 30 years?

… the dogma of ‘no new neurons’ was universally held and vigorously defended by the most powerful and leading primate developmental anatomist of his time.

Paradigms reject change when establishment hegemony is threatened.

A while ago I followed the story of Jacques Cinq-Mars who was a French-Canadian archaeologist who did fieldwork, searching “the Yukon riverbanks and rock shelters for traces of Ice Age hunters”.

His work in the Bluefish Caves in the North-West of Canada between 1977-87 and his subsequent analysis established that human life in that area existed 24,000 years ago.

The findings challenged the established view at the time – the so-called Clovis-First theory – which had dated the arrival of humans to ‘America’ at 13,000 years.

On May 3, 2013, the editorial in the journal Nature – Young Americans – described what happened when Cinq-Mars released his findings and sparked “one of the most acrimonious — and unfruitful —in all of science”.

Cinq-Mars:

… endured brutal criticism from opponents who did not give them, or their evidence, a fair hearing. Scientists who supported the Clovis-first model countered that reports of pre-Clovis sites were examples of poor scholarship.

Heather Pringle describes the criticism and pressures that Cinq-Mars was put under by the academy as he unveiled the findings of his research:

It was a brutal experience, something that Cinq-Mars once likened to the Spanish Inquisition. At conferences, audiences paid little heed to his presentations, giving short shrift to the evidence. Other researchers listened politely, then questioned his competence. The result was always the same … In his office at the Canadian Museum of History, Cinq-Mars fumed at the wall of closed minds. Funding for his Bluefish work grew scarce: his fieldwork eventually sputtered and died.

And studies now support his earlier claims “that humans reached the Americas well before the Clovis culture”. But the facts were not the issue – it was the challenge to the hegemony in this area of study that mattered.

As Pringle writes: “Today, decades later, the Clovis first model has collapsed”. It was fake knowledge all along but built careers and influence.

Well-paid professors who had made a lucrative career and garnered massive social status as a result of their claims about the first Americans were suddenly staring at a void – they had been peddling fake knowledge.

The impacts of the resistance are still being worked out.

Pringle writes:

Did archaeologists in the mainstream marginalize dissenting voices on this key issue? And if so, what was the impact on North American archaeology? Did the intense criticism of pre-Clovis sites produce a chilling effect, stifling new ideas and hobbling the search for early sites? Tom Dillehay, an archaeologist at Vanderbilt University in Tennessee and the principal investigator at the Chilean site of Monte Verde, thinks the answer is clear. The scientific atmosphere, recalls Dillehay, was “clearly toxic and clearly impeded science.”

Similarly, does an adherence by policy makers to the fake knowledge offered by mainstream macroeconomics force millions of people to endure unemployment and poverty unnecessarily. The answer is clearly yes.

A final example before I move on is closer to home. I refer to the story of Helicobacter Pylori. If you do not know what I am referring to then it is an amazing case of the resistance to new knowledge by those who had entrenched interests in maintaining fake knowledge.

In this case, it also involved the capacity of large pharmaceutical companies to make huge profits by forcing unnecessary drugs onto unsuspecting patients, kept in ignorance by their trusted doctors, who under pressure from the pharmaceutical companies to resist adopting new discoveries.

It involves the research of Dr Barry J. Marshall, who was a young doctor at the Fremantle Hospital in Perth, Western Australia in 1984. He discovered that the bacterium Helicobacter Pylori was associated with the incidence of stomach ulcers. Further research convinced Marshall and his team that the association was causal.

The mainstream of the profession at the time considered ulcers to be caused by “psychological turbulence” (see New Yorker link below).

This New Yorker article (May 3, 2003) – Marshall’s Hunch – provides an interesting insight into the controversy.

It recounts how Marshall first presented his work in 1983:

… at a gathering of infectious disease experts in Brussels. The audience was full of heavyweights … When Marshall finished speaking … The scientists chuckled and murmured and shook their heads, a little embarrassed for a junior colleague whose debut was such a disaster …

One scientist said Marshall’s theory was “the most preposterous thing I’d ever heard … I thought, This guy is a madman”.

The problem for Marshall was that up to that point the pharmaceutical giant Glaxo(SmithKline) were making massive profits selling Zantac to people whose doctors had diagnosed stomach ulcers. The drugs were palliative only – moderated symptoms (pain).

Patients were then on a treadmill where doctors would perform expensive and regular investigative colonoscopy procedures to ‘see’ whether the ulcer was contained and in between times would ingest Zantac and other remedies to control the pain.

They were put on special diets (cutting out things they liked) to stop the ulcer from erupting.

All of which Marshall demonstrated was unnecessary.

Now, Marshall’s findings are standard fare for the medical sector but it took many years before the message got through to GPs who were under the influence of the large drug companies, intent on suppressing the findings and keeping their markets.

All of these stories (and there are many more I could write about) involve regime change. They involve a new set of ideas or explanations coming headlong against the perceived mainstream and then being undermined until it becomes self-evident that the facts support the new idea.

Academic disciplines (such as, neurobiologists, archaeology, economists etc.) work within organised ‘paradigms’, which philosopher Thomas Kuhn identified in his 1962 book – The Structure of Scientific Revolutions – as “universally recognized scientific achievements that, for a time, provide model problems and solutions for a community of practitioners”.

Typically, the body of knowledge that defines the paradigm are “recounted … by science textbooks, elementary and advanced” (Kuhn, 1996: 10).

Kuhn challenged the notion that ‘scientific’ activity is a linear process, whereby scholars add new empirically supported facts to the knowledge base to replace previously accepted notions.

Rather, Kuhn said that dominant viewpoints persist until they are confronted with insurmountable anomalies, whereupon a revolution (paradigm shift) occurs. The new paradigm exposes the old theories as inapplicable, introduces new concepts, asks new questions and provides students with a new way of thinking with a new language and explanatory metaphors.

Once supplanted, the old theories are no longer considered valid knowledge. Kuhn also noted that there is a sort of mob rule among practitioners within a dominant paradigm and they vehemently hold onto their views even in the face of logical or empirical anomaly.

The dominant group becomes trapped in what Irving Janis called Groupthink and initially vilifies those who propose new ways of thinking.

The work of Joseph Altman, Jacques Cinq-Mars, Barry Marshall and countless others across all discplines represented the potential for a paradigm shift and was resisted by the mob until change became ineluctable.

Not all novel ideas face this sort of brick wall. But when the professional bodies become trapped by Groupthink and, typically, there is status and money at stake (particularly, commercial edge) then resistance can be fierce and prolonged.

So we can fairly say that the ideas discussed above resulted in regime change in their particular areas. In some cases, the regime confronted was dominated with real knowledge (such as the dating of the Clovis society) but some assertions relating to that knowledge become exposed.

In other cases, the knowledge is fake all along and the dominance of the discipline is maintained through control of media, professional appointment and promotion, access to research funds, and other smokescreens that are erected to deter outsiders from knowing what the facts are.

Mainstream macroeconomics fits into that latter category. It is fake knowledge and always has been. But the Groupthink discpline among the profession is very tight and coercive. Anyone who has ever challenged its position will know what I mean.

I was giving an invited presentation once at a prestigious conference on my macroeconomic views (I was the token Keynesian they used to have along to say they were providing a balanced roster of speakers! Not!).

Anyway, after I had given the presentation, the discussant started off by saying (with a whirring noise to start his spiel) “ladies and gentlemen, I think we are being visited by a presence from Mars today!” He said very little after that and just rode on the laughter in the audience. That was meant to be serious professional interchange.

It was nothing more than bullying. There was huge laughter at my expense – but by this stage I was a senior professor and had experienced years of this sort of ignorance. Always water off a duck’s back! I was inured to it.

When I was starting out, my very first referee’s report on a journal submission was one sentence long (they are normally, at least, a few pages long). It said “the author obviously hasn’t read or understood the first chapter in Lipsey”, which was a major mainstream textbook at the time, preaching the sort of rubbish that goes for mainstream macro.

That was it. I had spent hours working on the paper ensuring it was very tight and all I got was that. I took it as a challenge. But many more sensitive younger aspirants would have been destroyed by it – their confidence shot and their motivation damaged.

The economics profession is brutal and you have to have a thick hide to survive if you take it on.

So in this sense, Modern Monetary Theory (MMT) constitutes a regime change. It directly challenges (and exposes) the lies and deceptions of the dominant economic theories and provides a systematic and consistent alternative.

At first we were ignored – for the first 10 years at least of our work (the small group I noted above). Then the progressive side of economics (Post Keynesians) started criticising us – mainly because they attended similar conferences. They were hostile because MMT challenges some of the neo-liberal baggage that Post Keynesians still accept.

But as the message has spread further and the ‘second-generation’ MMTers on social media have become more vocal and numerous, there is now attacks coming from the mainstream economists.

These attacks are becoming widespread and represent the next stage in our development as a set of ideas. The neo-liberal Groupthinkers in the profession are now sensing that their position is weakening as more and more people are starting to eschew the value of the mainstream economics as a result of its massive failure in dealing with the GFC.

That event exposed my profession, which for years had been operating under the radar, so to speak. But its failures were manifest and the mob rule has began to erect all sorts of defences to protect their regime, including mounting public attacks on MMT.

But the regime shift that I have been talking about up to now is not the same thing as the blogosphere claims that ‘things will be better when MMT is adopted’.

That sort of sentiment implies that we can shift to a ‘MMT regime’ if enough politicians are convinced.

The point to understand is that MMT is a system of thought that allows us to understand how a fiat currency monetary system operates and the central role that government can play in a modern monetary economy.

Modern monetary economies use money as the unit of account to pay for goods and services. An important notion is that money is a fiat currency, that is, it is convertible only into itself and not legally convertible by government into gold, for instance, as it was under the gold standard or later versions of the gold standard.

What is mostly ignored in mainstream economic commentary is that in August 1971, the monetary system agreed at the famous Bretton Woods conference in July 1944, which required the central banks of participating nations to maintain their currencies at agreed fixed rates against the US dollar, collapsed.

The system proved unworkable and when President Nixon abandoned the convertibility of the US dollar into gold, most nations moved to a fiat currency system.

Within a fiat currency system, the government has the exclusive legal right to issue the particular fiat currency.

Further, given that this money is the only unit which is acceptable for payment of taxes and other financial demands of the government presents the government with a range of options.

We know that the government is not just a ‘large household’. The latter is the user of the currency and must finance its spending beforehand, ex ante, whereas government, the issuer of the currency, necessarily must spend first (credit private bank accounts) before it can subsequently debit private accounts, should it so desire (raising taxes).

Clearly, a fiat-currency issuing government is always solvent in terms of its own currency of issue.

MMT also teaches us that the purpose of State Money (fiat currency) is to facilitate the movement of real goods and services from the non-government (largely private) sector to the government (public) domain.

Government achieves this transfer by first levying a tax, which creates a notional demand for its currency of issue. To obtain funds needed to pay taxes and net save, non-government agents offer real goods and services for sale in exchange for the needed units of the currency. This includes, of-course, the offer of labour by the unemployed. The obvious conclusion is that unemployment occurs when net government spending is too low to accommodate the need to pay taxes and the desire to net save.

This analysis also sets the limits on government spending. It is clear that government spending has to be sufficient to allow taxes to be paid. In addition, net government spending is required to meet the private desire to save.

If the Government doesn’t spend enough to cover taxes and the non-government sector’s desire to save the manifestation of this deficiency will be unemployment. The basis of this deficiency is at all times inadequate net government spending, given the private spending (saving) decisions in force at any particular time.

Different nations (or blocs of nations) structure and use the capacity possessed by a fiat currency in different ways. The Eurozone Member States voluntarily ceded the capacity to Frankfurt and then imposed harsh rules on themselves with respect to net spending.

Other nations have evolved differently.

But the point is that every day, across every nation, monetary systems are in place that operate along the lines described and explained by MMT.

MMT has a very close relationship to reality, whereas mainstream macroeconomics is largely incapable of dealing with reality.

So to think that a better world is just a matter of moving to MMT is to misunderstand the reality. Monetary systems of all shapes and sizes already operate according to MMT.

So when I read comments like “if we introduced MMT …” or “under MMT policies …” or “when MMT becomes the norm”, which all imply that MMT is a regime that we would move to if society was more enlightened and would open up a new range of policy options that a truly progressive government might pursue I know that this point has been misunderstood.

This is tied in with other comments, specifically about the Job Guarantee, which suggest that MMT is a progressive doctrine or a left-wing approach to economic policy-making and what is holding MMT back from being introduced is the right-wing conspiracy to maintain hegemony.

I understand all these comments are well intended and people are genuinely attracted to some of the policy options that MMT proponents advance. This is notwithstanding, what I consider to be some doctrinal and irrational resistance to proposals such as the Job Guarantee.

But the conception that we might move to an MMT world where enlightened policy will free us from the yoke of capitalist exploitation is plain wrong.

The fact is that we are already living in the MMT world. We interact with each other every day in the MMT world. The monetary system, whether it be in the US, Australia, Japan or any of the Eurozone nations, operates along MMT lines.

So it is not about moving to some new Shangri-La, which we might call the MMT world – we are already in, that world.

What MMT provides is a new lens to view the world we live in and the monetary system operations that are important in our daily lives.

This new lens opens up new insights into what is going on in the economy on a daily basis. It’s not something to move to, it already is.

MMT, as a new powerful lens, makes things that are obscured by neo-liberal narratives more transparent.

It means that the series of interlinked myths that are advanced by conservative forces to distract us from understanding causality and consequence in policy-making and non-government sector decision-making are exposed.

So when a Conservative politician or corporate leader claims that the government has run out of money and therefore cannot afford income support for the unemployed any longer at the levels previously enjoyed, MMT alerts us to the fact that this is a lie and that there must be an alternative agenda.

MMT thus empowers a population who learn about it to see things for what they are and to ask questions that they never previously would have thought possible to ask or even relevant.

Previously, when a politician has said the government will run out of money or is maxing out its credit card, an uninformed population will take that statement as granted.

But an understanding of the MMT framework all its lens would mean that the population will now reject the “run out of money” obfuscation and instead demand to know why the government doesn’t want to support a particular policy option.

MMT thus, introduces into the policy debate, the possibility of new policy options and directions that have previously been dismissed out of hand through the use of spurious economic arguments that the politicians and their advisors know will not be properly scrutinised nor understood by the general population who they are trying to manipulate.

MMT is thus, a framework for understanding how the monetary system we live in operates and the capacities and options that are currency-issuing government has to advance our well-being.

It also allows us to understand the likely consequences of deviating from a truly sovereign state, which we define in terms of the currency-issuing status of the government (incorporating exchange-rate arrangements and central bank interest rate setting capacities).

In the latter context, the MMT lens provided us with a clear understanding of why the Eurozone would be a failure with significant negative consequences for the Member States.

Further, MMT is neither left-wing nor right-wing.

Where the confusion lies is in conflating the theoretical and descriptive content of MMT with the value systems that the proponents of MMT overlay on this content.

It might be thought that MMT is left-wing because the values I expound are from the left. But that would be a wrongful inference.

The ideological persuasion of any perspective will manifest in the values that are expounded and the policy prescriptions that are proposed to advance those values.

What MMT has allowed is for the ideological persuasion to become much clearer when a person advances a particular policy proposal.

For example, when a politician, faced with rising unemployment, says that there is no fiscal space for the government to create jobs to deal with the mass unemployment, a person considering that comment through the MMT lens, will immediately realise that the government must have a reason for maintaining higher than necessary unemployment.

We know there must be a ‘hidden’ agenda because our understanding tells us that the government fiscal space is defined in terms of available real resources that the government can purchase with its currency-issuing capacity. So if there is mass unemployment then we know that there are such available real resources.

So why would the government refuse to purchase them and bring them back into productive use?

The focus then shifts on what that reason is and questions are likely to lead, for example, to an examination of corporate influence that might be leading the government to refuse to use their currency-issuing capacities to maintain full employment.

But when a right-wing politician inspired by MMT expresses a desire to ensure there is a reserve army of unemployed because it will suppress wage demands and enhance profits (which he/she values above worker dignity etc) then they would propose cutting the fiscal deficit because their MMT training tells them that is how they will achieve their goal.

MMT just tells us what the consequences of imposing our values on society via policy choices will be. Those values can take any political or ideological colour.

Conclusion

I hope that discussion helps some readers out there who have been struggling with this sort of issue.

Next week, I will present a blog forecasting the “first 100 days of a Melenchon Presidency for France”. Right-wing economists trading in fake knowledge have already published such an exercise. It is comical. I will try to be more serious.

That is enough for today!

(c) Copyright 2017 William Mitchell. All Rights Reserved.

MMT is just plain good economics – Part 1 – Bill Mitchell – Modern Monetary Theory

Modern Monetary Theory (MMT) is just plain old bad economics

When I read that I wondered what plain new good economics might be.

By inference from the second sentence in the quote above it suggested some body of work that was about ‘money’ holding its value. Perhaps.

But, of course, the core MMT group has never suggested a currency cannot become entirely worthless. Of course it can.

Hyperinflation will do that in a domestic sense if nominal aggregate spending from any source (government or non-government) increasingly outstrips the productive capacity of the economy to respond by producing real goods and services. Inflation accelerating into hyperinflation then becomes the adjustment mechanism to this increasing excess aggregate demand.

Further, an ever-plunging (depreciating) exchange rate towards some infinite asymptote will logically do that in an international context.

Thus, in that sense MMT is fully cognisant that a currency can become, under certain extreme conditions, worthless. But equally, MMT tells us that a government would have to be acting in a ridiculous way for these conditions to persist to the point that the extremes were reached. More about which later.

So, the question remains unanswered. What is plain new good economics?

The other inference is that the advisor has been previously associated with New Keynesian type analysis.

Presumably, the ‘New’ bit means it isn’t plain old, but then that would be a misconception, because New Keynesian economics really reverts back to many of the propositions of pre-Keynesian (neoclassical) economics, which were categorically refuted during the 1930s, by Keynes and others.

In fact, New Keynesian economics is not really macroeconomics at all given that it overcomes aggregation problems and heterogeneous agents by assuming representative agency. A ridiculous fudge for those who want it in simpler language.

Even Marx knew in the middle of the C19th that many of the propositions that remain embedded in the current, dominant New Keynesian approach were flawed to the point of being useless.

Most mainstream macroeconomic theoretical innovations since the 1970s (the New Classical rational expectations revolution … and the New Keynesian theorizing) … have turned out to be self-referential, inward-looking distractions at best. Research tended to be motivated by the internal logic, intellectual sunk capital and esthetic puzzles of established research programmes rather than by a powerful desire to understand how the economy works – let alone how the economy works during times of stress and financial instability. So the economics profession was caught unprepared when the crisis struck … the Dynamic Stochastic General Equilibrium approach which for a while was the staple of central banks’ internal modelling … excludes everything relevant to the pursuit of financial stability.

So that seems to put the dominant mainstream approach to macroeconomics in the plain old bad camp.

Thus, the question remains unanswered. The most obvious conclusion is that the statement “MMT is just plain old bad economics” has no real foundation – it is just a put down to make the writer seem erudite.

In fact, as my MMT colleague Scott Fullwiler has captured in tweet form, there are several novel (that is, new) features that MMT has introduced into the economics literature that significantly improve our understanding of how monetary systems function.

These features are absent in the mainstream approach.

Scott Fullwiler

@stf18

In economics, "govt can always spend & avoid legal default" is NOT radical. But these ARE:

The veracity of the arguments (both the tweet and the more detailed work mapping out the contribution of MMT) remains intact despite increasing attempts to criticise them by mainstream economists.

A logical conclusion is that MMT, in its current form, which clearly draws on many brilliant antecedents, and then adds new components, should be considered at the frontier of macroeconomics, while New Keynesian thinking is the degenerate paradigm (in the Lakatosian sense).

But there is a more important point and the Labour advisor reveals his ignorance when he talks about “MMT prescriptions” in the debate.

He wrote (see Richard Murphy’s blog post for verification):

Well, I disagree – in terms of what a genuinely radical and transformative Labour government would need to do on the economy, its prescriptions are close to catastrophic (for all that it has grasped some correct formal insights ahead of neoclassicism). Any country that isn’t the US trying to apply MMT’s prescriptions would find itself in the same position.

This appeared to be a poorly crafted paragraph. But the point we should focus on is the statement about the application of “MMT prescriptions”.

Exactly, what are those prescriptions?

Here we encounter a misconception that I have dealt with many times.

This short excerpt from a longer lecture I gave in New Zealand last year expresses the point succintly. The full lecture (54 minutes) is available – HERE – and traverses many of the issues that I am writing about now.

I have stated this point often but it still seems to escape the attention of many critics (and second-generation MMTers, for that matter).

MMT is not a regime that you ‘apply’ or ‘switch to’ or ‘introduce’.

Rather, MMT is a lens which allows us to see the true (intrinsic) workings of the fiat monetary system.

It helps us better understand the choices available to a currency-issuing government.

It is not a regime but an accurate perspective on reality.

It lifts the veil imposed by neo-liberal ideology and forces the real questions and choices out in the open.

In that sense, MMT is neither right-wing nor left-wing – liberal or non-liberal – or whatever other description of value-systems that you care to deploy.

I mean by that, that while MMT provides a clear lens for viewing the system, to advance specific policy platforms, one has impose a value system (an ideology) onto that understanding.

For the Labour advisor to talk about “MMT’s prescriptions” reveals he hasn’t fully understood that distinction.

The point is that MMT is what is. Britain’s monetary system is governed and operates under the principles outlined by MMT.

It is not a matter of moving to MMT.

By eschewing the discretionary use of fiscal policy and imposing fiscal rules one is not exercising ‘non-MMT’ policy options.

The MMT lens allows us to tease out and more accurately predict the consequences of such a policy choice.

But there are no ‘non-MMT’ policy options. That is not very well understood.

So when the Labour advisor talks about a state where MMT policy prescriptions are being chosen he is revealing his ignorance of these distinctions.

What he is actually referring to are specific policy proposals that have been advanced.

Which I can only deduce are related to the use of fiscal flexibility given that his supply-side agenda is hardly ‘tame’ – nationalisation, tightly controlled government procurement policies.

Clearly, British Labour have adopted the neoliberal position on fiscal rules and I will discuss this more in Part 2.

I have written extensively about why adopting such rules is poor policy and likely to be counterproductive and unworkable.

Just look what happened in the Eurozone when the GFC hit! The Stability and Growth Pact thresholds were blown out of the water just by the movement in the automatic stabilisers, much less any discretionary stimulus packages that governments might have considered or introduced.

Please see the following blog posts (among others):

But isn’t the Job Guarantee an ‘MMT prescription’?

Now, someone might pop up and claim that because I have argued extensively that the concept of a Job Guarantee is intrinsic to MMT then I am trying to have it both ways.

Isn’t the Job Guarantee an ‘MMT prescription’.

Which compromises the ‘lens’ bit, doesn’t it?

Again a deeper understanding of economic theory is required to understand the nuance here.

The employment buffer stock framework is intrinsic to MMT because it supercedes the various mainstream (including Keynesian) versions of the relationship between unemployment and inflation (the so-called Phillips curve), which historically was seen as the ‘missing equation’ in the standard macroeconomics, linking the product market to the labour market and the real economy (output and employment determination) to the nominal economy (price level determination).

I know that is a mouthful and probably meaningless for non-economists but it is for the record and if you are curious you will explore the idea further.

Then you will: (a) understand the intrinsic nature of the Job Guarantee to MMT, and; (b) you will never again say that the T in MMT is redundant.

Sure enough there are descriptive elements of MMT like any body of thought. So at one level, the sectoral balances framework is just an accounting record. But linking the elements within that record has to be theory in order of us to make sense of it and to use it in a diagnostic and predictive manner.

So, while the Job Guarantee superficially appears to be a policy prescription, which would suggest that MMT is more than just a superior lens through which you can understand how the monetary system actually works and better appreciate the capacities of the currency-issuing government, the reality is that if one establishes that ‘economy’ is about the elimination of inefficiencies, then the choice between the two price stabilising realities:

(a) a NAIRU unemployment buffer stock system; and

(b) a Job Guarantee employment buffer stock system, is a non-choice.

Only (b) is closer to being efficient, given the massive wastage of income and human potential that arises.

So the Job Guarantee is much more than a simple ‘policy prescription’.

It is an essential component of a macroeconomic stability framework, a point that is lost on many, who only construct it as a job creation program.

I discussed that aspect of MMT in the blog posts (cited above (3 part series ‘What is new in MMT’).

That macroeconomic stability device is the MMT answer to the Phillips curve, which no economist would say is not an intrinsic theoretical device in mainstream macroeconomics.

The fact that the Phillips curve, as a theoretical device, is then used to offer policy options (or not), is beside the point.

Theory typically has a praxis attached to it. Otherwise why would we bother.

And even if we take the view that an employment guarantee is a policy prescription rather than something more theoretically intrinsic, does the Labour advisor truly believe that a national government that introduced a Job Guarantee would see its currency dropped by speculators to the point of it becoming worthless?

Why would they do that?

Did they do that at the time of the GFC when fiscal deficits rose many multiples what they might do in the first year of a Job Guarantee?

No.

He might be trying to claim that a Job Guarantee would alter the balance of power between capital and labour and thus represent a paradigmic challenge to the capacity of business to make profit.

This is a favourite of what we might call the neoliberal Left who, in their paranoid belief that global financial markets are all powerful and reduce currency-issuing, sovereign governments to mendicancy status, try to proffer ‘evidence’ that business will close down any government that dares aspire to attain full employment.

Well, historically, Kalecki was proven wrong in this regard. For three decades after his article was published governments successfully sustained true full employment despite the resistance from some quarters of the industrial capitalist community.

Where were the capital strikes? And all the rest of it.

Sure enough, in the 1960s, there was currency instability as the Bretton Woods fixed exchange rate system was finally giving in to its inherent inconsistencies – well summarised by Robert Triffen’s Paradox – where the US had to supply US dollars and thus run large current account deficits, which in turn, led to fears that the dollar would fall in value.

But that currency instability was linked to the exchange rate arrangements not the fact that most nations were running continuous fiscal deficits over this period to support income growth and satisfy the desires of the non-government sector (especially the private domestic sector) to save overall and thus sustain aggregate spending at levels consistent with full employment.

I also considered his claim that the full employment aspirations of a government would always be undermined by capitalist resistance in an article I published in the Journal of Economic Issues in 1998 – W.F. Mitchell (1998) ‘The Buffer Stock Employment Model and the NAIRU: The Path to Full Employment’, Journal of Economic Issues, 32(2), 547-55 – Download.

There is no doubt that there was resistance from capital during the full employment decades following the Second World War.

But the thirst for social democracy was so powerful that governments were able to countervail that resistance. Politically, the idea that a nation could sustain vastly elevated levels of labour underutilisation just didn’t cut it in these periods.

Conservative and Labour governments alike were forced by public sentiment to prioritise full employment.

It was not until the Monetarists emerged and circumstances allowed the ideology associated with those economic ideas to begin its four or so decade domination that public sentiment changed.

But the change came from a massive misinformation campaign assisted in Britain by the Labour politicians that had become infested with neoliberal ideas, if not ideology. They were duped by the Monetarist claims into abandoning social democratic policy positions.

And then Thatcher, Major, Blair and so on followed in the same deceptive manner.

Capital resists impingement on their profits, it abhors the idea of sharing national income with workers, but it has to work through the legislative domain of the nations it operates (produces and/or sells) in.

Moreover, in the contemporary setting, when I explain the concept of a buffer stock of employment to hard core business types, who aren’t posturing for political purposes on the public stage, they are uniformly supportive.

Why?

They see it as a way to reduce hiring costs because the workers have not become dislocated from the labour market in the same way as the long-term unemployed become.

1998年にJournal of Economic Issuesに掲載された記事で、政府の完全雇用志向は常に資本主義者の抵抗によって損なわれてしまうという彼の主張も考慮した。 Mitchell(1998)、「バッファストック雇用モデルとNAIRU:完全雇用への道」、Journal of Economic Issues、32(2)、547-55 - ダウンロード。

Consider this graph, which shows the Australian dollar exchange rate against the US dollar from 1970 to 2018 (using left axis) and the Federal fiscal balance over the same period (using right axis).

For clarity I separated years that the Federal government was in deficit (red bars) and years it was surplus (gray bars). The other point to note is that the fiscal data is for fiscal years, while the exchange rate data is monthly.

To provide concordance I just assumed that the fiscal balance for each fiscal year (July-June) was the same in each month of the corresponding year to allow me to map annual data into monthly space. That is why the fiscal data is very block-like in appearance.

It doesn’t distort the general point however.

Australia is a small, open economy, which also has most of its trade defined by primary commodity exports and advanced manufacturing imports.

It is not like a nation that exports industrial goods, which tend to have more stable prices on international markets. Primary commodity prices fluctuate dramatically, often quickly and in unpredictable ways.

For example, Australia’s terms of trade fell by 13.3 per cent in the five quarters to the June-quarter 1986 (agricultural and mineral prices fell sharply). Australia’s GDP fell by around 10 per cent in the March-quarter 1986 as a result because export volumes were suddenly selling at much lower prices.

So Australia knows a lot about currency instability and shifts from an Australian dollar buying 50 cents US (or equivalent in other currencies) in one period to near parity in the next without any other major change in policy or economic structure being the cause.

The point of the graph is that you will see no particular relationship between our exchange rate movements, which are largely driven by the terms of trade movements in the primary commodity markets, and the fiscal position adopted by government.

You will see that in the period that the Federal government was running ever-increasing surpluses, the exchange rate fell to its lowest levels in the modern (fiat currency) era.

And at times when deficits were rising, the currency was appreciating and other times, when in fiscal deficit, the currency depreciated.

And you can see that for the vast majority of the period shown, the Federal government was in deficit.

I could extend the period if there was comparable data and the story would not alter.

If I used another nation, the story would not alter.

In fact, there has never been a statistically robust relationship found between the fiscal conduct of a currency-issuing government and the movements in exchange rates.

So why do the Left immediately rehearse their paranoia that a currency will be rendered worthless via exchange rate sell-offs by the speculators, when it is proposed that a nation runs a fiscal deficit and uses that net spending to support non-government saving desires, sustain full employment and build productive infrastructure?

Conclusion

On Monday, I will consider how currencies become worthless (or not).

That is enough for today!

(c) Copyright 2018 William Mitchell. All Rights Reserved.

《…Keynes was a master of argument, but even he did not always win. More recently Deirdre McCloskey made a similar claim in her book The Rhetoric of Economics (1985). Her point is that evidence alone is not decisive; ‘rhetoric’, the art of discourse, is also important.》 (Mitchell 2019 #2:32)

1980年代とそれ以降、主流派による過去への再解釈が勢いづいた。 Weber(1997: 71)は”新しい経済学”の勃興を以下のように特徴づけている: 『…生産におけるグローバリゼーション、金融の変化、雇用の性質、政策、新しい市場、そして情報技術が…景気循環の抑制を齎すようになった。』 [Reference: Weber, S. (1997) ‘The End of the Business Cycle?’, Foreign Affairs, 76(4), 65–82]

2002年、ハーバード大学の経済学者James StockとMark Watsonはこうした所感を捉え、アメリカの経済は、”過去20年を越える景気循環の安定、及びGDP成長率のボラティリテの全般的低下を反映した””静止状態”になったと論じた(Stock and Watson, 2002)。彼らはこうした傾向を”大いなる安定”と名付けた(2002: 162)。[Reference: Stock, J.H. and Watson, M.W. (2002) ‘Has the Business Cycle Changed and Why?, in Gertler, M. and Rogoff, K. (eds.), NBER Macroeconomics Annual 2002, Volume 17, MIT Press, 159-218]

進歩的な文献(例えば、The Common Values Handbook)(訳注:The Common Cause Handbookの間違い? とりあえずそれらしきもの発見できず)では、”我々の態度や行動”に影響を与える”我々の基本規範”となる価値観を明示しようとしている。広範な研究によって、”一貫して生ずる人間的価値観が大量に特定された”。(Common Values Handbook, 2012:8)

I have been travelling a lot today (nearly 6 hours starting early) and so haven’t much time for blog writing. I am working on a paper at present on the use of metaphors in economics and how Modern Monetary Theory (MMT) might usefully frame its offering to overcome some of the obvious prejudices that prevent, what are basic concepts, penetrating the public psyche. Here are some notes on that theme. The blog is just a rough sketch and will be refined over the coming weeks. There is a section at the end that encourages reader feedback – lets see what you think.

Framing

Macroeconomics is an area of study that is fraught with controversy. Macroeconomics is seen as being of significant national importance but the concepts that are involved in understanding macroeconomic functions are difficult to understand well.

For example, what is an aggregate price level? How do we understand a budget deficit or a budget surplus? And are all budget deficits the same?

Macroeconomic concepts are discussed in the media on a daily basis, such as, the real GDP growth rate, the inflation rate, the unemployment rate, the budget deficit, and the interest rate.

Finance segments on national news broadcasts, introduced over the last three decades or so, increasingly expose the public (and journalists) to macroeconomic terminology, without a commensurate increase in the degree of education associated with the terminology or concepts.

Further, the advent of social media has made it possible for anyone to become a macroeconomic commentator: the so-called blogosphere is replete with self-styled macroeconomic experts who make claims about the state of the federal budget, often relying on “common sense” logic to make their cases.

The problem is that common sense is a dangerous guide to reality and not all opinion should be given equal privilege in public discourse. Our propensity to generalise from personal experience, as if the experience constitutes general knowledge, dominates the public debate – and the area of macroeconomics is a major arena for this sort of false reasoning.

The surge in public interest in matters macroeconomic has been channelled by the dominant neo-classical paradigm in economics. As a consequence, the public understanding becomes straitjacketed by orthodox concepts and conclusions that, in themselves, are erroneous, but also lead to policy outcomes that undermine prosperity and subvert public purpose.

The abandonment of full employment in the 1980s and the willingness to tolerate mass unemployment is a manifestation of this syndrome.

The dominant macroeconomics paradigm, which prior to the global financial crisis had pronounced that the business cycle was largely dead and that we had entered a period of “great moderation”, categorically failed to foresee the consequences of the labour market and financial deregulation that it had promoted.

We would argue that its lack of empirical content and its demonstrated failure to predict novel facts (the GFC) renders the mainstream macroeconomics a pseudo-scientific, degenerative research program following the classification scheme proposed by Imre Lakatos in 1970.

However, any sense that the crisis would lead to a major examination of the role of mainstream economics and action to change the curricula taught and research agendas pursued were short-lived. Mainstream economists exercised their anti-government free-market biases and effectively reconstructed what was a private debt crisis into a sovereign debt crisis. The dynamics that created the crisis (deregulation, reduced financial oversight) continue to be advocated by the mainstream as solutions.

The public debate is dominated by claims that fiscal austerity is the only viable path to recovery and leading multilateral agencies such as the IMF and the OECD have produced glowing forecasts, which denied that major fiscal retrenchments would damage growth.

This view was unchallenged by media commentators. Subsequently, the IMF has been forced to admit its calculations were in error (IMF apology article) although this admission, stunning for what it represents, has had little impact on the dominant discourse.

Modern Monetary Theory (MMT) is a coherent, internally consistent and well-developed macroeconomics framework, which is ground in the operational reality of the capitalist monetary economy.

Its track record in explaining major events over the last two decades (including the global financial crisis and its aftermath) suggests that it is a progressive research program (in the Lakatosian sense) capable of predicting novel facts, which are confirmed by subsequent events.

In this regard, MMT is a superior basis for macroeconomic reasoning relative to the dominant neo-classical approach.

But the problem is dealing with the way the dominant macroeconomics paradigm frames its argument. Why does the emerging MMT approach, which though superior in the ways noted above, fail to resonate with the wider public.

Framing refers to the way an argument is mounted or pursued in the public debate. Cognitive linguists have shown that the way we understand complex issues is via metaphors and neo-classical macroeconomics has been extremely successful in its use of common metaphors to advance their ideological interests (the work of George Lakoff is prominent).

It is apparent that we end up believing things and supporting policies that actually undermine our own best interests because of the way the arguments are presented to us. In other words, we accept falsehoods as truth and ideology triumphs over evidence.

Recent psychological studies have highlighted the extent to which pre-existing biases influence the way in which individuals interpret factual information, including straightforward statistical data.

This presents a problem for the communication by researchers to the public of research outcomes that bear on public policy design, particularly where findings may be counter-intuitive, or may challenge a dominant or controversial discourse, as in the case of economic austerity or climate change.

The aim of the paper we are working on at present – with some notes presented below – is that we consider the evolution of MMT as a viable consistent alternative but recognise that the language deployed by progressives and conservatives in communication about key macroeconomic concepts undermines the successful communication of insights arising from MMT.

We aim to provide a conceptual basis for understanding how language matters (the contribution of my co-author who knows about these things) and examine some of the key metaphors used to reinforce what the flawed message of orthodox economics and examine key ideas of modern monetary theory and propose effective ways of expressing those key ideas.

Fellow MMT colleague Randy Wray and others have explored the metaphors that underpin the language that is commonly used to describe macroeconomic operations and outcomes.

There has, however, been limited work in the linking of metaphorical language to values and the way language reinforces or undermines a particular value or set of values. That is our aim.

The economy is Us

People created the economy. There is nothing natural about it. Concepts such as the “natural rate of unemployment”, which imply that the economy is a natural system, which should be left to its own equilibrating forces to reach its natural state, like any living system.

But when we use terms like natural we have to ask – natural in relation to what? The mainstream define the problem away rather than address the ideological benchmark that the term “natural” disguises.

The reality is that human interaction and choices, initially simple and localised, and later, significantly more complex and spatially distributed (globalised), creates what we call the economy. We are in charge here.

At some point, we realised that we needed an agent to do things that we could not do ourselves – either easily or at all. We formed governments. We also came to understand that our creation – the economy – would only serve our common purposes if it was subject to oversight and control by our agent.

We had operated under the mistaken view that this agency role was unnecessary because our spontaneous interactions would sort things out in our favour. It didn’t happen and when the consequences of this failure became so obvious – during the Great Depression – we accepted the agency role as being fundamental to ensuring that the capitalist monetary system behaved itself.

We learned then that capitalism which had developed into a broad system of wage labour was subject to basic tensions between labour and capital. We also learned that the so-called “market” signals (prices that brought demand and supply together) would not deliver employment outcomes that satisfied the desires of labour for work.

We learned that this system could easily equilibrate (a state where there was no further dynamic for change) in a state of mass unemployment. The Great Depression taught us that our agent (the government) could ensure that the system did not get stuck in this state because it had the spending capacity to ensure that total spending in the economy generated enough output that would fully employ all those who wanted work.

The simple understanding of that period was that the economy was a construct we could control in order to create desirable collective outcomes such as improved living standards – better housing for all, improved public education and health standards etc. All outcomes that required real resources to be brokered by the public sector in cooperation with the private firms and workers.

While there was a strong conservative element that resisted the Post-World War 2 consensus, the government mediated the class conflict to ensure the system did deliver social as well as private returns. We understood that if employment fell it was because there wasn’t sufficient demand and because the economy was us, we knew what to do about it – spend more. The question was how would this be accomplished.

Economists certainly understood that private spending could become stuck – while the unemployed certainly had a demand for goods and services, they only sent a notional signal to the firms of that desire. The private market only works on effective demand and supply signals – that is, demand intentions backed by cash and the unemployed didn’t have any cash because they had lost their job and employment provides income which funds spending.

While the way the macroeconomists spoke of such things was reserved for the academy (full of jargon etc), the concepts were also broadly understood by the public and we knew that a government budget deficit was required to ensure that total spending was sufficient (for full employment) when the rest of us (the non-government sector) were not recycling all our current income back into the spending stream (that is, saving).

The period of neo-liberal smugness

In the 1980s and beyond, the mainstream revision of the past gathered pace.

Weber (1997: 71) wrote that the rise of the “New Economics”, characterised by the:

… globalization of production, changes in finance, the nature of employment, government policy, emerging markets, and information technology, had contributed] … to the dampening of the business cycle.

[Reference: Weber, S. (1997) ‘The End of the Business Cycle?’, Foreign Affairs, 76(4), 65–82]

The “facets” which had smoothed out growth and supply shocks would now be:

… less important in a more flexible and adaptive economy that adjusts to shocks more easily and with less propensity for sparking a new cycle (Weber, 1997: 71).

Weber also implicated the decline in union strength, more flexible labour markets, and the rapid growth of the financial sector as contributing to the end of the business cycle.

He said that the “enormous growth” in derivatives trading was beneficial because “(t)hese new financial products spread and diversify risk” and that the new class of funds managers were “better at using these new tools to stabilize financial flows and protect themselves against shocks” (1997: 74). The financial sector was seen as lubricating “increasingly efficient” global capital markets and had created an array of “shock absorbers that cushion economic fluctuations” (1997: 75).

He also said (1997: 80) that the “current consensus on inflation among central bankers” will “also constrain states’ fiscal policies” and that the “inherently cyclical nature of government spending will decline as business cycles dampen”.

Weber (1997: 75) concluded that “doomsday” arguments “that complex markets might act in synergy and come crashing down together is simply not supported by a compelling theoretical logic or empirical evidence.” Such views were increasingly common among mainstream economists as the new century approached.

In 2002, Harvard economists James Stock and Mark Watson captured this sentiment and noted that the US economy was “quiescence” which reflected “a trend over the past two decades towards moderation of the business cycle and, more generally, reduced volatility in the growth rate of GDP” (Stock and Watson, 2002). They termed this trend the “great moderation” (2002: 162).

[Reference: Stock, J.H. and Watson, M.W. (2002) ‘Has the Business Cycle Changed and Why?, in Gertler, M. and Rogoff, K. (eds.), NBER Macroeconomics Annual 2002, Volume 17, MIT Press, 159-218]

On February 20, 2004 the current US Federal Reserve Board Governor Ben S. Bernanke presented a paper in Washington entitled “The Great Moderation” (Bernanke, 2004), which summarised the views held by the vast majority of economists that the business cycle was dead!

[Reference: Bernanke, B.S. (2004) ‘The Great Moderation’, paper presented to the the Eastern Economic Association, Washington, DC, February 20, 2004, available at: http://www.federalreserve.gov/BOARDDOCS/SPEECHES/2004/20040220/default.htm]

The celebratory, smug confidence of the mainstream economists is best summarised by Robert Lucas Jnr. in his presidential address to the American Economics Association (2003: 1):

Macroeconomics was born as a distinct field in the 1940’s, as a part of the intellectual response to the Great Depression. The term then referred to the body of knowledge and expertise that we hoped would prevent the recurrence of that economic disaster. My thesis in this lecture is that macroeconomics in this original sense has succeeded: Its central problem of depression prevention has been solved, for all practical purposes, and has in fact been solved for many decades. There remain important gains in welfare from better fiscal policies, but I argue that these are gains from providing people with better incentives to work and to save, not from better fine-tuning of spending flows. Taking U.S. performance over the past 50 years as a benchmark, the potential for welfare gains from better long-run, supply-side policies exceeds by far the potential from further improvements in short-run demand management.

The message was simple. The mainstream economists had triumphed over the interventionists who had over-regulated the economy, undermined the incentive from private enterprise, allowed trade unions to become too powerful, and bred generations of indolent and unmotivated individuals who only aspired to live on welfare support payments.

This triumph manifested at the policy level by the primacy of monetary policy in counter-stabilisation, where the primary policy target became inflation stability. Fiscal policy was rendered a passive subordinate and governments abandoned their responsibilities to maintain full employment.

The sentiments expressed by Lucas coincided with the major shift in policy direction towards so-called microeconomic reform, which resulted in extensive financial and labour market reform. The pre-conditions for what was to become the global financial crisis were set in place during this period.

Real wages growth started to lag behind productivity growth as a result of attacks on unions and the rising precariousness of work (increased casualisation and rising underemployment), which undermined the capacity of workers to pursue adequate recompense.

The loss of capacity to maintain consumption growth was overcome by the burgeoning financial sector, which grew rapidly on the back of a massive increase in private sector debt, increasingly provided to more and more marginal borrowers then packaged up into complex derivatives and on-sold to the next sucker.

The official narrative was that of Lucas – the business cycle was largely dead.

This view of the world was buttressed with a vehement political campaign which sought to dispose of the binding concepts such as collective will etc in favour of promoting the view of the economy as a natural system delivering outcomes to individuals in accordance to their contributions.

They promoted the economy as a self-regulating system.

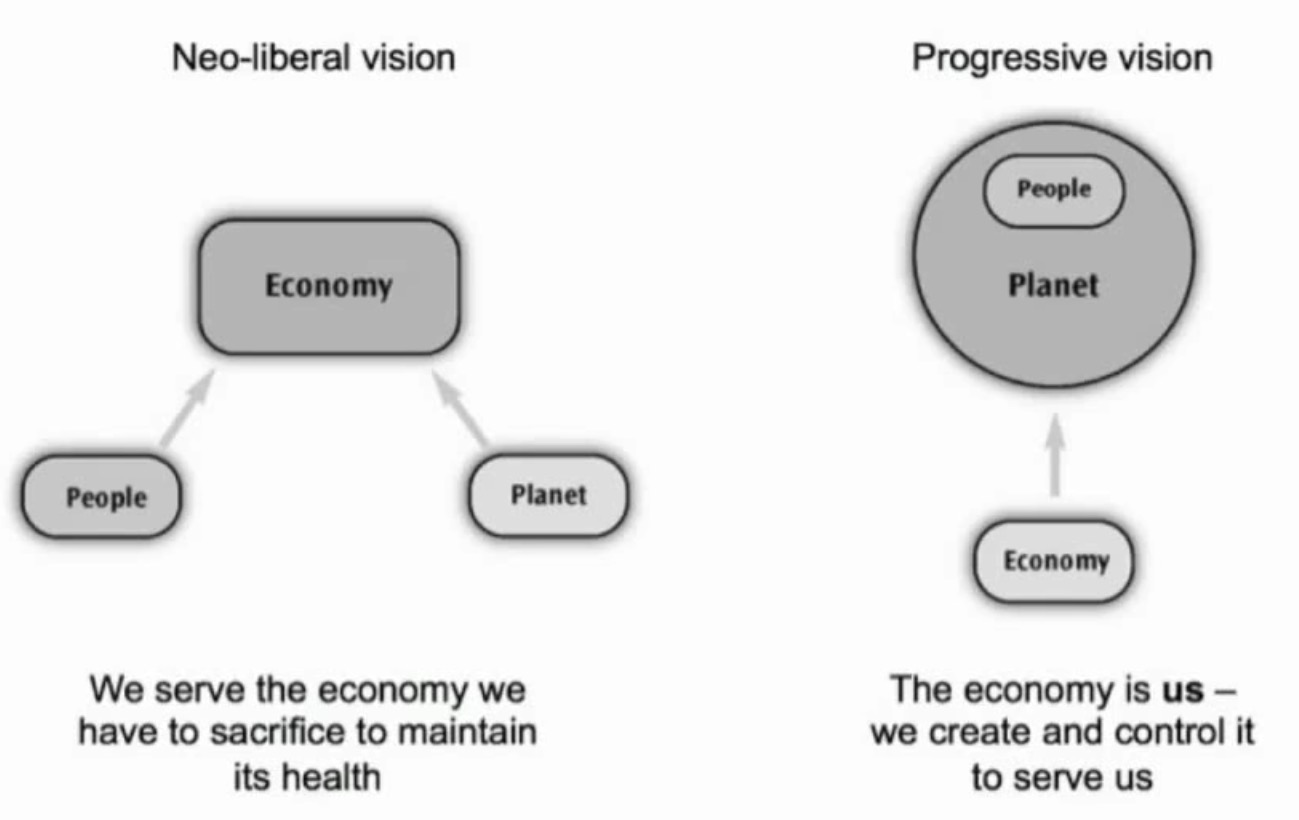

In her book, Don’t Buy It, Anat Shankar-Osorio juxtaposes two models of the economy. The first depicted in the following graphic which she considers represents the conservative view (although there are progressives that would be lumped into this category).

Accordingly, the driving image is that “people and nature exist primarily to serve the economy” (Location 439). The economy is removed from us and is a moral arbiter, which recognises our endeavour and rewards us accordingly. Those who do not work hard and sacrifice for the “economy” are deprived of such rewards.

But if the “government” intervenes in the competitive process and provides an avenue where the undeserving (lazy, etc) still receive rewards then the system malfunctions and becomes “sick” (a metaphor that the economy is a living thing) and the solution is to restore its natural processes (aka getting rid of government intervention such as minimum wages, job protection, income support etc).

So “self-governing and natural” are the messages we receive, which leads to the obvious conclusion that “government ‘intrusion’ does more harm than good, and we just have to accept current economic hardship” (Location 386).

Our success then is somehow independent of the success of the economy. The hallmarks of a successful country are whether real GDP growth is strong irrespective of whether “this comes at the expense of air quality, leisure time, life expectancy, or happiness … all of these are secondary”.

If poverty rates are rising, the construction is that the person is just not doing enough for the economy rather than the economy failing, in its current operations, to do enough for us. We are to blame for our own failures. They arise because we don’t contribute enough. How can we expect to be rewarded for a sub-standard contribution to the success of the economy?

Progressives get sucked into this narrative and offer up “fairer” alternatives within, for example, the austerity debate. Take the current debates in the advanced nations.

None of the major (progressive) political parties are challenging the austerity dogma. You will often read a progressive commentator writing something like … “we know the deficit is a problem and public debt has to be reduced, but we think this should be done more gradually”.

At that point, both sides of the debate are effectively singing off the same hymn sheet and the public discretion gets lost in the fog. The basic propositions are root-and-branch wrong but the solutions seem obvious and the different value-systems (conservative and progressive) are left to argue about matters of degree.

Towards an alternative

In the early 1990s, as the neo-liberal credit binge was beginning, the early proponents of what is now broadly known as Modern Monetary Theory (MMT) – this was a small group (Mosler, Mitchell, Wray, Forstater, Fullwiler, Tcherneva then Bell/Kelton) – drew on earlier heterodox theory (functional finance etc) and added particular operational insights about the monetary system – to develop an alternative narrative about the way the monetary capitalist system operated.

They used this narrative to expose what they saw was an unsustainable dynamic fostered by the mainstream belief that self regulating markets would deliver maximum wealth to all.

Even in those early stages of the private debt build-up it was clear that a major crisis was approaching, given the ill-considered financial practices that were emerging.

Other progressive economists, however, were not so engaged. They were mostly intent on focusing on issues such as gender, sexuality, method and, as such, provided a fragmented, and easily dismissed critique of the mainstream economics narrative.

There was also hostility with progressive ranks to the growing literature being produced by the proponents of MMT.

The Great Moderation was brought to a stark halt by the global financial crisis, which began in early August 2007 when the French bank BNP Paribus stopped withdrawals from three investment funds in response to the growing concern about the viability of the sub-prime loan portfolios. Later in the same month, there was a run on the British bank Northrock.

As the wealth that had been built up during the Great Moderation started to prove illusory, with housing and share prices falling sharply, the crisis escalated. In September 2008, Lehmans collapsed.

At that point, the myth of self-regulating markets was exposed and the entire edifice of mainstream economic theory lost creditability – none of the dominant Neo-Keynesian models taught in universities or used by academics in scholarly articles was equipped to predict the crisis or offer viable solutions to the crisis.

Finally, it was clear to all that the emperor had no clothes.

The initial response to the crisis of the mainstream economists was silence although there were notable exceptions.

On October 23, 2008 as the crisis was escalating, the former US Federal Reserve Chairman appeared before the US House Committee on Oversight and Government Reform, which was investigating the “The Financial Crisis and the Role of Federal Regulators”.

The Chairman of the Committee, Henry Waxman asked Greenspan whether his free market ideology that pushed him to make regrettable decisions. He replied (US House of Representatives, 2008, page 36-37):

Mr. GREENSPAN. Well, remember, though, whether or not ideology is, is a conceptual- framework with the way people deal with reality. Everyone has one. You have to. To exist, you need an ideology.

The question is, whether it exists is accurate or not. What I am saying to you is, yes, I found a f1aw, I don’t know how significant or permanent it is, but I have been very distressed by that fact …

Chairman WAXMAN. You found a flaw?

Mr. GREENSPAN. I found a flaw in the model that I perceived is the critical functioning structure that defines how the world works, so to speak.

Chairman WAXMAN. In other words, you found that your view of the world, your ideology, was not right, it was not working.

Mr. GREENSPAN. Precisely. That’s precisely the reason I was shocked, because I had been going for 40 years or more with very considerable evidence that it was working exceptionally well.

However, any sense that the crisis would lead to a major examination of the role of mainstream economics and action to change the curricula taught and research agendas pursued were short-lived.

The mainstream profession began to reconstruct what was a private debt crisis into a sovereign debt crisis, which suited their anti-government, free market biases.

The dynamics that had created the crisis (deregulation, reduced oversight) were advocated as solutions. The public debate was flooded with claims about that fiscal austerity was the only viable path to take and leading multilateral agencies such as the IMF and the OECD produced glowing forecasts, which denied that major fiscal retrenchments would damage growth.

Subsequently, the IMF has been forced to admit its calculations were in error (IMF apology ARTICLE).

So while the MMT narrative has had a high predictive value its capacity in influencing the public debate has been close to zero.

Shenker-Osorio (2012) provides this alternative conception of the economy, which is consistent with the view that it is our construct and not something separate from us.

She writes (Location 1037):

This image depicts the notion that we, in close connection with and reliance upon our natural environment, are what really matters. The economy should be working on our behalf. Judgments about whether a suggested policy is positive or not should be considered in light of how that policy will promote our well-being, now how much it will increase the size of the economy.

Or we might add – how much it adds to the budget deficit or public debt.

Her suggestions sits squarely with the principles of functional finance – that we see the economy as a “constructed object” – and policy interventions should be appraised only in terms of how functional they in relation to our broad goals.

We thus need to elaborate more fully what the goals that we seek to achieve are. A particular budget deficit, for example, is a meaningless goal.

The budget balance will be whatever it is – in relation to our goals and the functional relationship that net public spending has in relation to those goals.

The government is not a moral enforcer and the economy is not a morality play.

Metaphors and Values

There is a progressive literature (for example, the Common Values Handbook) which attempt to articulate the values considered to be “our guiding principles” which influence “the attitudes we hold and how we act”. Extensive research has “identified a number of consistently-occurring human values” (Common Values Handbook, 2012: 8).

This research that is drawn upon largely centres around the work of Schwartz and his value circumplex. He identified 10 basic and universal human values which frame the way we think.

Our view – which will be elaborated in the paper – is that this discussion is somewhat of a side-show. The values are so general that any idea can be consistent with them.

We prefer to concentrate on developing some broad principles and working on a language to support them.

Broad principles and terminology