MMTの金融政策無効論がまとまったものとして、Fullwiler[&Wray]の "Quantitative Easing and Proposals for Reform of Monetary Policy Operations" levyinstitute.org/pubs/wp_645.pdf というWPが分かりやすそう。

Additionally, rising interest rates tend to hurt corporate profitability. It costs more for companies to borrow money, buy inventory, expand facilities and pay salaries, all of which hurt corporate profitability and, accordingly, depress stock valuations. There is one noteworthy exception to this, namely stocks in financial services companies. Bank, brokerage, insurance company and mortgage originator earnings often increase as interest rates move higher, because they can charge more (in the form of interest) for the money they lend to companies and individuals.

History has demonstrated that higher interest rates in the United States, and around the world, will negatively impact the price of commodities.

When interest rates rise, the cost of capital (e.g. in the form of bank loans) to purchase the commodities increases thus driving up the carrying (or holding) cost of these inventories. Since the cost of capital is higher, holding or warehousing large quantities of these commodities is no longer cost efficient. That encourages consumers of raw materials to buy these commodities only on an as-needed basis rather than holding large stockpiles.

It is not an understatement to say that interest rates, or the change in interest rates, impacts virtually every asset class: equities, bonds, currencies and commodities. Although interest rates have risen slightly over the past year, the Federal Reserve is now offering unprecedented transparency, making clear their desire and intention to raise short term interest rates. This article is intended to highlight the correlation between interest rates and these asset classes, focusing on the traditional impact that rising rates will have.

It is important to remember, however, that interest rates are not the ONLY factor for determining how assets will perform, any more than the earnings of a company are the ONLY determinant of a stock’s value, but it certainly is a very important determinant.

RISING INTEREST RATES = DECLINING BOND PRICES

First and foremost, rising interest rates cause the price of outstanding bonds to decline. This is because, as interest rates rise new bonds are offered at these new, higher rates of interest. Since the new bonds offer higher interest rates, the attractiveness of existing bonds at lower rates declines. This inverse relationship between price and yield is fundamental and critical to understanding bonds. New bonds offering higher returns cause the price of older bonds offering lower interest rates to decline.

RISING INTEREST RATES = DECLINING STOCK PRICES

Rising interest rates traditionally result in lower stock prices for two reasons. As interest rates rise, income generating investments become more attractive to investors. Investors will be more likely to purchase assets into income generating investments (like bonds or CDs) and less likely to invest in stocks. In a rising rate environment, we see an inflow of money into income generating investments and an outflow of money from equities. Less demand for equities ultimately results in lower prices being paid for them.

Additionally, rising interest rates tend to hurt corporate profitability. It costs more for companies to borrow money, buy inventory, expand facilities and pay salaries, all of which hurt corporate profitability and, accordingly, depress stock valuations. There is one noteworthy exception to this, namely stocks in financial services companies. Bank, brokerage, insurance company and mortgage originator earnings often increase as interest rates move higher, because they can charge more (in the form of interest) for the money they lend to companies and individuals.

RISING INTEREST RATES = RISING CURRENCY VALUE

Higher, or rising, interest rates traditionally increases the value of a country's currency. Higher interest rates tend to attract foreign investments and investors, increasing the demand for and value of the country’s currency. Alternatively, low or declining interest rates tend to discourage foreign investors and therefore decrease the currency's value.

Certainly, interest rates alone do not determine a currency’s value. Economic stability and the demand for a country's goods and services are also of importance. Favorable economic numbers such as a large Gross Domestic Product (GDP) and level balances of trade (imports vs. exports) are also key figures that analysts and investors consider in assessing a given currency.

When referring to the U.S. dollar there is another important consideration: the U.S. dollar is a reserve currency. This means that many foreign central banks hold substantial amounts of U.S. dollars. This is partly because globally, commodities like gold and oil are traded in U.S. dollars but also because, due to relative economic and political stability, the dollar has historically been considered a global haven of safety in an uncertain world. Due to these considerations, despite historically low interest rates here in the U.S. for the past 10 years, the dollar has shown strength relative to most other global currencies.

History has demonstrated that higher interest rates in the United States, and around the world, will negatively impact the price of commodities.

When interest rates rise, the cost of capital (e.g. in the form of bank loans) to purchase the commodities increases thus driving up the carrying (or holding) cost of these inventories. Since the cost of capital is higher, holding or warehousing large quantities of these commodities is no longer cost efficient. That encourages consumers of raw materials to buy these commodities only on an as-needed basis rather than holding large stockpiles.

Gold is sometimes thought to be an exception to this rule and, certainly, the price of gold responds to a number of different factors. The primary difference between gold and other commodities is that many investors feel gold is a haven of safety and is, therefore, an effective inflation hedge (meaning as inflation or interest rates rise, the value of gold would also rise). History also shows us, though, that a lowering interest rate environment results in rising gold prices, and higher interest rates reduces gold prices.

Since 1975 (when gold futures began trading), there has been an inverse relationship between gold and real interest rates. Gold has generated positive returns during periods of falling real interest rates and negative returns during periods of rising real interest rates. The exception to this is when economic uncertainty is the cause of the inflation. In this case, gold prices will increase despite higher interest rates.

Again, interest rates are not the only factor that impacts the value of other assets like stocks, currency and commodities, but history has shown us that changes in interest rates do impact the prices of all these assets. Whether investing in these assets for long term or trading them actively, it is wise to know how these changes impact the market.

RESPONDING TO RISING INTEREST RATES

For the Bond Investor: Higher short term rates now make them more attractive than a year ago. That, plus the flat yield curve (long term rates not being substantially higher than short term rates) means that income-oriented investors should invest in short term instruments (Treasury Bills, CDs, short maturity corporate or municipal bonds). Also, the fact that these investments will mature in the short term gives you the opportunity to reinvest the proceeds at the expected higher rates when your bonds mature. Another suggested strategy is to invest in floating rate instruments (like TIPS, floating rate bonds). Given the expected rise in rates, the investor will benefit from this and be rewarded with rising coupons and income on their investments.

For the Borrow: For individuals seeking to borrow money, the rise in rates should be a call to action. Waiting will only cost you. As the past year has shown, the interest rates on mortgages, home equity loans and personal loans have all risen. This is only expected to continue, so in this situation, time is money. Delaying your decisions will only result in more expensive borrowing.

For the Equity Investor: The fact that interest rates were so low here in the U.S. for so long acted as buoyancy for the stock market as investors sought other investments. Accordingly, the rise in rates should act as a hinderance to further stock appreciation.

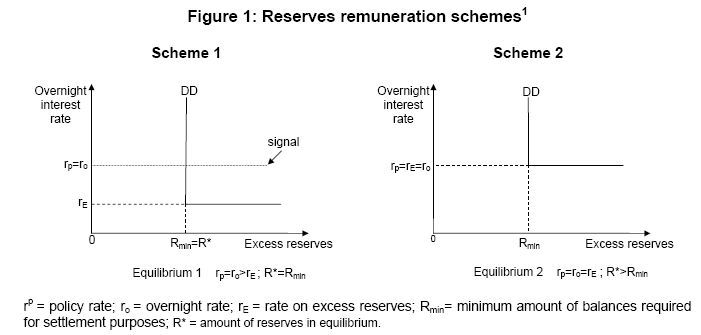

BISのペーパーの16ページから始まるセクション―Are bank reserves special?―は、主流派のコンセプトに毒された読者によって誤解されたミスリーディングな言葉(たとえば、クラウディングアウトのような)をところどころ用いてしまってはいるけれども、それでもなお読む価値のとても高い部分だ。

リチャード・クーは2003年出版の彼の著書 Balance Sheet Recession: Japan’s Struggle with Uncharted Economics and its Global Implications(John Wiley & Sons) (邦題:デフレとバランスシート不況の経済学) でこう述べている:

今日私は仕事でDubboにいる。Dubboはニューサウスウェールズ州の西部で、州の中でも外れた辺鄙なところにある。普通の人々はしばしば通り過ぎてしまうこのオーストラリアの田舎では、美しい景観が楽しめる。私のこの実地見学は、この地域の土着のコミュニティについて私が継続的に行っている研究と関係がある。この研究についてはいつか報告しよう。さて、今日の記事は、私が昨日に準備預金について展開したテーマの続きだ。昨日の記事―Building bank reserves will not expand credit(邦訳)では、準備預金の動態について検討したが、時間が無かったので、いくつかの論点を残してしまっている。一つの論点は、準備預金拡張がインフレーションに与える影響の可能性についてだ。これは、危機に対する金融政策の効果に関する時代遅れな考えについての主流派たちの病的熱狂の核心的部分だ。結論については安心してほしい――金融政策についての唯一の問題は、それが無効であり、より大きい財政政策の努力が必要だというところだ。

BISペーパーの後半で、著者たちは次の疑問を検討している: ”準備預金によるファイナンスは特別にインフレ促進的なのか?” 昨日の記事――Building bank reserves will not expand credit (邦訳) を思い出してほしい。ポール・クルーグマンは、現時点において再び量的緩和が望ましい政策であると提唱した。量的緩和が民間部門に将来的なインフレーションを予想させるからだという。彼はQEを準備預金の拡張と定義づけた。

第二に、Building bank reserves will not expand credit (邦訳) において、我々は準備預金の拡張が銀行融資を増加させないことを示した。準備預金の拡張が銀行融資を増加させるというアイデアは、銀行が融資の前に準備預金を必要とするという誤った理解に基づいている。そんなことは疑いなく絶対にないのだ。この点において、主流派マクロ経済学の教科書は完全に間違っている。

・MMTの金融政策無効論がまとまったものとして、Fullwiler[&Wray]の "Quantitative Easing and Proposals for Reform of Monetary Policy Operations" levyinstitute.org/pubs/wp_645.pdf というWPが分かりやすそう。

2 Comments:

招き猫 (@kyounoowari)

2019/07/28 5:07

ノーベル賞受賞のシムズ

「マイナス金利の深掘りはデフレ的に働く」

本来なら国債の利払いを通じて

政府→民間

への所得移転を逆転させること

0金利の長期化も同様で

政府→民間

への所得移転を無しにすること

ケルトンさんの量的緩和等の金融政策の問題点で言いたいことはこのポイントでしょう

Twitterアプリをダウンロード

以下まとめサイトより

・7月17日の講演の方で、80年代の米で、金利が上がったのに逆に不動産投資が過熱した例を挙げてたはず。

日本でもバブル期に似たような現象が確認されてるわけだよね。

少し前のインタビューでも「日銀はゼロ金利を維持しろ」みたいなこと言ってたはず。

・これは「利上げが自動的にインフレや景気を抑制する」などの、能天気な思考に対してのもので、

短期も長期もそんな単純なわけないじゃんと、反対の効果の一つを強調しているだけで。

・MMTの金融政策無効論がまとまったものとして、Fullwiler[&Wray]の "Quantitative Easing and Proposals

for Reform of Monetary Policy Operations" levyinstitute.org/pubs/wp_645.pdf というWPが分かりやすそう。

・ケルトンが経済はパブロフの犬では有りません、利上げに対して反射的に反応したりしませんよ説明してたな。

コメントを投稿

<< Home