これまで、我々は皆、こうした(新自由主義的)コンセプトがあまりに抽象的で、かつメディアが延々とそれらを推奨するがゆえに、完全に欺かれてきた――そのため、中立利子率や自然失業率といった(両者は本質的に関係している)が、完全なるたわごと(total crock of sh.t)であるかどうかを疑うことすらできなかった。

The media is increasingly reporting that the RBA will hike interest rates by the end of 2009. I consider this to be a nonsensical suggestion given that unemployment and underemployment will still be rising and it is unclear whether employment growth will be anything than near zero at that time. From a theoretical perspective, at the root of all the conjecture, whether the journalists actually realise it or not, is a concept called the “neutral rate of interest”, which is just another neo-liberal smokescreen. That is what this blog is about.

In the Melbourne Age today, there was an article entitled Why rates are on the way back up. Another Age economics correspondent Peter Martin, also said on his blog after reporting a bank economist saying the same thing that this makes sense.

So-called “market sentiment” (according to the Age article) is such that most business economists:

… expect the RBA to lift the cash rate to around 4.25 per cent by the end of 2010. That’s 1.25 per cent above where we are today.

The reasoning given by all these economists is taken from a statement made recently by the RBA Governor, Glen Stevens. In response to a question from the Chair of the House of Representatives, Standing Committee on Economics meeting in Sydney on Friday, August 14, 2009, Stevens said (for full transcript)

Well, we are not tightening monetary policy right now. To give a bit of perspective to this discussion about when the time will come for interest rates to lift off the bottom, what we have got in place at the moment is an emergency setting. It is a setting of the cash rate that is the lowest for 40 years put in place in anticipation that the economy would be seriously weak and that there would be very real risks to the downside that stem from a global situation that none of us has lived through before … As the set of risks that you think you face start to shift, at some point you are going to have to make a response to move away from the emergency setting … That in no way signals any less concern for these other economic dimensions. When the time comes it will mainly be that the emergency has passed sufficiently so that we do not hold the emergency setting any longer. Were we to do so, I think that there is ample evidence elsewhere in the world of problems that you ultimately get if you keep the emergency setting in place for too long …

The Age article chimed in on this theme by quoting a business economist who said this:

… the current cash rate at 3 per cent is the lowest in a generation – we haven’t seen anything like this since the late 1960s …

Sure enough, we haven’t seen interest rates this low since the late 1960s but then again we also haven’t been close to full employment since the late 1960s as well. The two are not unrelated.

Anyway, what is behind all this conjecture is a rather insidious notion that mainstream economists continually refer to which is termed the “neutral rate of interest”.

The Age writer says this:

It’s generally considered that a cash rate around 5 per cent is now neutral for the Australian economy – that is, it neither stimulates the economy nor holds it back … A cash rate at 3 per cent then is highly stimulatory. It’s the fiscal equivalent of the central bank flooring the accelerator in a bid to spin the Australian economic tyres out of the global financial crisis mud.

Well unlike mainstream economics who dream these concepts up without any real empirical support, modern monetary theory considers things differently (why would you be surprised by that).

But first some background.

The idea of a neutral rate is relevant because it reflects the belief in the primacy of monetary policy as the preferred counter-stabilisation tool. Accordingly, almost all economists these days (not me!) believe that the central bank can maximise real economic growth by achieving price stability. Consistent with this view is the belief that when the central bank target interest rate is below the “neutral rate of interest”, inflation will break out (eventually) and vice versa.

So the neutral rate is sometimes called the equilibrium interest rate. It has a direct analogue in the labour market in the concept of the natural rate of unemployment – another neo-liberal smokescreen.

Where did this construction come from? We can initially see the idea in the writings of Classical British economist Henry Thornton (1760-1815) but the best known exposition is found in the 1898 book by Swedish monetary theorist Knut Wicksell (1851-1926). Wicksellian thinking is very influential among central bankers.

In his classic book – Interest and Prices (1936 edition published by Macmillan and Co) – Wicksell defined a “natural interest rate” as follows (page 102):

There is a certain rate of interest on loans which is neutral in respect to commodity prices, and tend neither to raise nor to lower them. This is necessarily the same as the rate of interest which would be determined by supply and demand if no use were made of money and all lending were effected in the form of real capital goods. It comes to much the same thing to describe it as the current value of the natural rate of interest on capital (emphasis in original).

So consistent with the view held in those times that the loanable funds market brought savers together with investors, the natural rate of interest is that rate where the real demand for investment funds equals the real supply of savings.

Wicksell also differentiated the interest rate in financial markets which is determined by the demand and supply of money and the interest rate that would mediate “real intertemporal transfers” in a world without money. So this meant that “money” had no impact on the “natural interest rate” which reflects only real (not nominal) factors.

He wrote (page 104):

Now if money is loaned at this same rate of interest, it serves as nothing more than a cloak to cover a procedure which, from the purely formal point of view, could have been carried on equally well without it. The conditions of economic equilibrium are fulfilled in precisely the same manner.

All this reasoning is consistent with the idea that classical idea that money is a “veil over the real economy”, that it only affects the price level. The way in which this occurs in Wicksellian thought is that the deviation between the interest rate determined in the financial markets and the natural rate impacts on the price level.

So when the money interest rate is below the natural rate, investment exceeds saving and aggregate demand exceeds aggregate supply. Bank loans create new money to finance the investment gap and inflation results (and vice versa, for money interest rates above the natural rate).

I could write at length outlining why this conception is inapplicable to a modern monetary economy but that isn’t the purpose of this blog.

With the natural rate of interest an unobservable imaginative construct, Wicksell claimed that the link between price level movements and the gap between the two interest rates provided the clue for policy makers.

He wrote (p.189) that:

This does not mean that the banks ought actually to ascertain the natural rate before fixing their own rates of interest. That would, of course, be impracticable, and would also be quite unnecessary. For the current level of commodity prices provides a reliable test of the agreement of diversion of the two rates. The procedure should rather be simply as follows: So long as prices remain unaltered the banks’ rate of interest is to remain unaltered. If prices rise, the rate of interest is to be raised; and if prices fall, the rate of interest is to be lowered; and the rate of interest is henceforth to be maintained at its new level until a further movement of prices calls for a further change in one direction or the other. (emphasis in original).

So you can see the genesis of the natural rate concept that central bankers still hold onto – but now prefer to refer to it as the “neutral rate of interest”.

In this vein, there was an important speech given by former Federal Reserve Chairman Alan Greenspan in 1993 which elevated this concept back into mainstream policy considerations. Central bankers in the 1980s had been beguiled by Milton Friedman’s view that they needed to control the stock of money if they were to maintain price stability. As a consequence monetary targetting was pursued and soon after turned out to be a total failure.

It was obvious that the stock of money could not be controlled by the central bank given it was endogenously determined by the demand for credit. Modern monetary theory never considered money to be exogenously determined – which is the main presumption in mainstream macroeconomics textbooks.

Anyway, to fill the gap, central bankers shifted ground. In his Statement to the Congress, on July 20, 1993 (published in the Federal Reserve Bulletin, September 1993, pages 849-855, Greenspan told the Congress that:

In assessing real rates, the central issue is their relationship to an equilibrium interest rate, specifically the real rate level that, if maintained, would keep the economy at its production potential over time. Rates persisting above that level, history tells us, tend to be associated with … disinflation … and rates below that level tend to be associated with eventual resource bottlenecks and rising inflation, which ultimately engender economic contraction.

This was an important break from the money targeting period and marked the beginnings of inflation targeting whereby central banks would announce or imply a target rate of inflation and then adjust the interest rate up or down to manipulate (so they thought) aggregate demand and hence prices. This aproach explicitly used unemployment as a policy tool to suppress inflation – high unemployment was maintained over this period to suppress aggregate demand as part of the “inflation-first” macroeconomic strategy.

You can see that Greenspan’s “equilibrium interest rate” is just a replay of Wicksell’s “natural interest rate” theory which was dominant in the days before the Great Depression. However, to advocate Wicksell’s theory you have to buy into the whole theoretical box-and-dice – in all its inanity and inconsistency.

Accordingly, you have to consider markets equilibrate through price adjustments and the economy tends to full employment (meaning there cannot be a deficiency of aggregate demand). So if consumption falls (because saving rises), the interest rate (in the loanable funds market) falls (excess supply of loans) and investment rises to fill the gap left by the fall in consumption. This is Say’s Law which is restated as Walras’ Law when multiple markets are introduced.

So the interest rate adjusts to the natural interest rate where the full-employment level of savings equals investment and all is well. There is never a shortage of investment projects but their introduction is impacted upon by the cost of funds. There is never unemployment!

Marx by the way had already disassembled all this nonsense in Capital and I urge you to trace out his argument, for to some extent, what followed (Keynes and Kalecki) was anticipated by Marx.

Anyway, it was exactly these issues that Keynes tackled in the General Theory. In Chapter 14, Keynes said (page 189) that:

The classical school proper, that is to say; since it is the attempt to build a bridge on the part of the neo-classical school which has led to the worst muddles of all … This leads on to the idea that there is a “natural” or “neutral” … or “equilibrium” rate of interest, namely, that rate of interest which equates investment to classical savings proper without any addition from “forced savings” … But at this point we are in deep water. “The wild duck has dived down to the bottom — as deep as she can get — and bitten fast hold of the weed and tangle and all the rubbish that is down there, and it would need an extraordinarily clever dog to dive after and fish her up again.”

Thus the traditional analysis is faulty because it has failed to isolate correctly the independent variables of the system. Saving and Investment are the determinates of the system, not the determinants. They are the twin results of the system’s determinants … [aggregate demand] … The traditional analysis has been aware that saving depends on income but it has overlooked the fact that income depends on investment, in such fashion that, when investment changes, income must necessarily change in just that degree which is necessary to make the change in saving equal to the change in investment.

In other words, the orthodox position that the interest rate somehow balances investment and saving and that investment requires a prior pool of saving are both incorrect. We learned categorically that investment brings forth its own saving through income adjustments.

What drives all this is effective demand – spending backed by cash (Marx definitely wrote about that in Theories of Surplus Value). The 1930s totally discredited the Wicksellian ideas about the dynamics of the economy and the centrality of interest rate adjustments in stabilising the economy.

But that failed paradigm reappeared in the 1970s and by the 1990s was dominant again. All this talk about neutral interest rates really inherits all that baggage.

How useful is the neutral rate of interest for policy? This is not a stupid question. The characters who continually spout that there is a neutral (natural) rate of interest are unable to categorically measure it.

So they take Wicksell’s route and assert that if prices are rising then the interest rate must be below the neutral rate and vice versa. In other words they just create the concept based on their own theory of how price adjustments occur. We are just told that the connection between interest rate movements and inflation is definite and the theory is sound so therefore without even being able to measure the natural rate we can tell where we are in relation to it.

Meanwhile, all of us are totally hoodwinked because the (neo-liberal) concepts are so abstract and the media continually pushes them – so we never question whether the concept of a neutral rate of interest and a natural rate of unemployment (both intrinsically related) are a total crock of s..t. But I am here to tell you that they are.

Our results reveal a high degree of specification uncertainty, an important one-sided filtering problem, and considerable imprecision due to data uncertainty. Also, the link between trend growth and the equilibrium real rate is shown to be quite weak. Overall, we conclude that statistical estimates of the equilibrium real rate will be difficult to use reliably in practical policy applications.

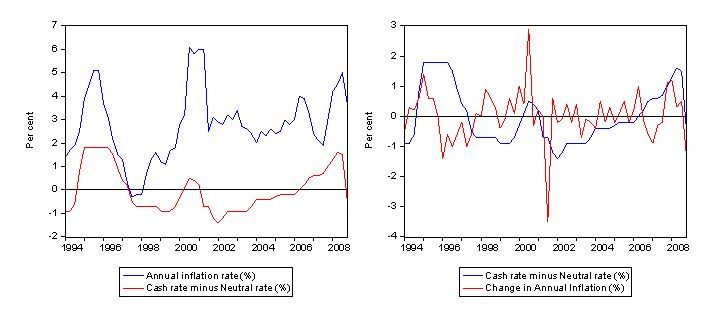

I could go into an elaborate discussion about techniques that have been used to estimate the neutral interest rate. All of them fail and are no better than taking the average of the actual interest rate over some long period. If we consider the period since March 1994 when inflation expectations were all but purged from the system by the 1991 recession and the RBA adopted inflation targeting formally (in 1994) we can construct some graphs to let you see how stupid the neutral rate notion is.

The average short-term interest rate (policy rate) over that period (to December 2008) was 5.67 per cent (not far off the so-called neutral rate).

The first graphs show the deviation of the cash (target) rate from the “neutral” rate of 5.67 per cent (the average since 1994) plotted against the annual inflation rate (left-hand panel) and the change in the annual inflation rate (right-hand panel). The same story would emerge if I used Hodrick-Prescott filters, Kalman filters or Marlboro filters! The first two are commonly employed in the empirical literature as means of estimating the neutral (equilibrium) rate.

Interest-rate deviations above the zero line mean the the current cash (policy) rate is above the neutral rate and that should be deflationary and values below the zero line mean the current cash rate is below the neutral rate and this should be inflationary. It is unclear what the theory is about – whether it is pointing to the first-derivative of the price level (inflation) or the second derivative (change in inflation – or how fast inflation changes). So the graph provides information about both.

You can see that no relationship depicted is consistent with anything Wicksell foresaw.

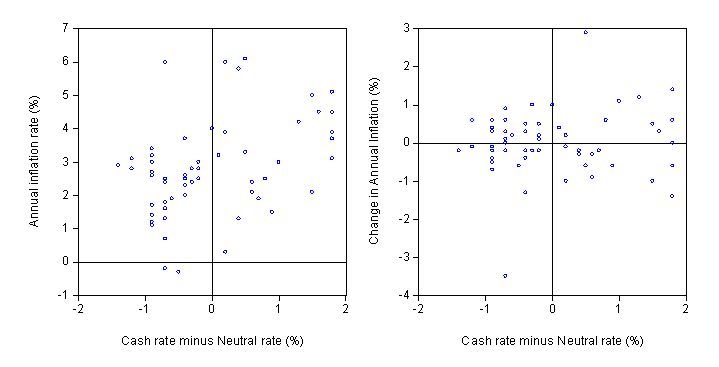

The second graph provides a scatter depiction of the relations. The left-panel is between the cash rate deviation and inflation and the right-panel is between the cash rate deviation and the change in inflation. We should see a concentration of observations in the top left and bottom right quadrants. We do not. That is no surprise to a modern monetary theorist for reasons I elaborate on next. But it is another example of faulty theory being used to provide authority for bad monetary policy.

Why the “natural” interest rate is zero

Modern monetary theorists consider monetary policy to be a poor tool for counter-stabilisation. It is indirect, blunt and relies on uncertain distributional behaviour. It works with a lag if at all and imposes penalties on regions and cohorts that may not be contributing to the price pressures (for example, when Sydney property prices were booming all of regional Australia which was not was forced to bear the higher interest rates). There is also no strong empirical research to tell us about the impact on debtors and creditors and their spending patterns. It is assumed implicitly that borrowers have higher consumption propensities than lenders but that hasn’t been definitively determined.

For a modern monetary theorist, fiscal policy is powerful because it is direct and can create or destroy net financial assets in the non-government sector with certainty. It also does not rely on any distributional assumptions being made.

Further, the natural economic state for a modern monetary theorist is full employment which means less than 2 per cent unemployment, zero hidden unemployment and zero underemployment. Deviations from full employment reflect failed fiscal policy settings – not a large enough budget deficit (other things equal).

The size of deficit has to be judged in terms of the desire of the non-government sector to save in the currency of issue. So if the deficit is inadequate and unemployment arises we know the net spending has not fully covered the spending gap.

We also know that budget deficits add to bank reserves and create system-wide reserve surpluses. The excess reserves then stimulate competition in the interbank market between banks who are seeking better returns than the support rate offered by the central bank. Up until recently this support rate in countries such as Japan and the USA was zero. In Australia it has been 25 basis points below the cash rate although there is no theoretical reason for that setting.

It makes much better sense not to offer a support rate at all. In that situation, net public spending will drive the overnight interest rate to zero because the interbank competition cannot eliminate the system-wide surplus (all their transactions net to zero – no net financial assets are destroyed).

So in pursuit of the “natural” policy goal of full employment, fiscal policy will have the side effect of driving short-term interest rates to zero. It is in that sense that modern monetary theorists conclude that a zero rate is natural. This article by Warren Mosler and Mathew Forstater is useful in this regard.

If the central bank wants a positive short-term interest rate for whatever reason (we do advocate against that) – then it has to either offer a return on excess reserves or drain them via bond sales.

Our preferred position is a natural rate of zero and no bond sales. Then allow fiscal policy to make all the adjustments. It is much cleaner that way.

And all those bright sparks in the central bank could be redirected (retrained) to studying cancer cures or engage in something else that is useful.

これらすべてを駆り立てているのは、効果的な需要、つまり現金で支出された支出です(Marxは間違いなくそれについてTheory of Surplus Valueで書いています)。1930年代は、経済のダイナミクスと経済を安定させる上での金利調整の中心性についてのWicksellianの考えを完全に信用していませんでした。

0 Comments:

コメントを投稿

<< Home